Homeownership stands as a cornerstone of the American dream for many, representing not just a place to live, but often the most significant financial asset an individual or family will acquire. Yet, the journey to owning a home is rarely achieved without assistance. This is where “home lending” comes into play – a complex, multi-faceted financial mechanism that makes the dream of homeownership a tangible reality for millions. Far more than just borrowing money, home lending is an intricate system involving various financial institutions, regulatory bodies, and a robust process designed to facilitate the purchase of residential property.

At its core, home lending refers to the process by which individuals or entities borrow funds from a financial institution (the lender) to purchase a home, using the property itself as collateral for the loan. This arrangement, commonly known as a mortgage, binds the borrower to regular payments over an extended period, typically 15 or 30 years, until the loan principal and accumulated interest are fully repaid. Understanding the nuances of home lending is crucial for anyone contemplating a property purchase, as it directly impacts financial stability, long-term wealth building, and overall quality of life. This guide will demystify home lending, exploring its fundamentals, the diverse types of loans available, the application process, key influencing factors, and critical post-approval considerations.

Understanding the Fundamentals of Home Lending

To fully grasp the landscape of home lending, it’s essential to first establish a solid understanding of its fundamental components and the roles played by various participants. This foundational knowledge will serve as a compass as we navigate the more complex aspects of securing a home loan.

Defining Home Lending and Mortgages

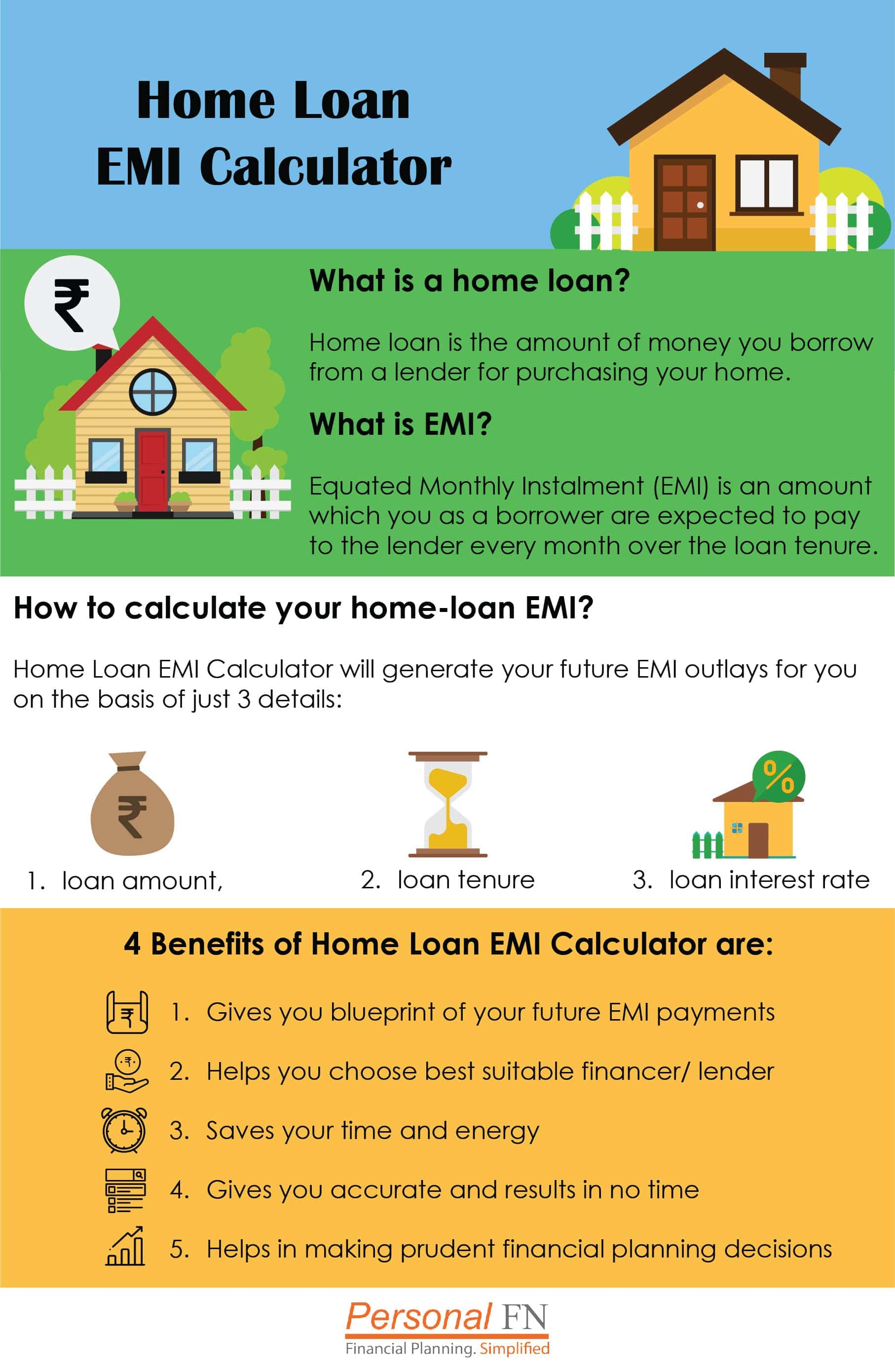

At the heart of home lending is the mortgage. A mortgage is a legal agreement by which a bank or other creditor lends money at interest in exchange for taking title to the debtor’s property, with the condition that the conveyance of title becomes void upon the payment of the debt. In simpler terms, it’s a loan specifically for buying real estate, where the house itself serves as security. Should the borrower default on payments, the lender has the legal right to seize the property through a process called foreclosure to recover their investment. This security is what makes large loans like mortgages feasible for lenders.

The Role of Lenders and Borrowers

The home lending ecosystem primarily consists of two key players: the borrower and the lender.

Borrowers are individuals or entities seeking funds to purchase a home. They commit to repaying the loan according to agreed-upon terms, including principal and interest. Their financial health, creditworthiness, and ability to repay are rigorously assessed during the application process.

Lenders are financial institutions that provide the capital for home loans. These can include commercial banks, credit unions, mortgage companies, and even some government agencies. Lenders assess risk, determine interest rates, manage the loan application and underwriting process, and service the loan (collect payments) throughout its term. Their primary goal is to provide loans that are both profitable and low-risk.

Why Home Lending is Crucial for Homeownership

For the vast majority of people, buying a home outright with cash is not financially viable due to the substantial cost of real estate. Home lending bridges this gap, providing the necessary capital to turn property ownership aspirations into reality. It democratizes access to housing, allowing individuals to spread the cost of a significant asset over many years, making it an affordable endeavor. Moreover, mortgages contribute to economic stability by facilitating real estate transactions, stimulating construction, and creating employment opportunities within the financial and housing sectors. Without robust home lending mechanisms, the concept of widespread homeownership would be largely unattainable.

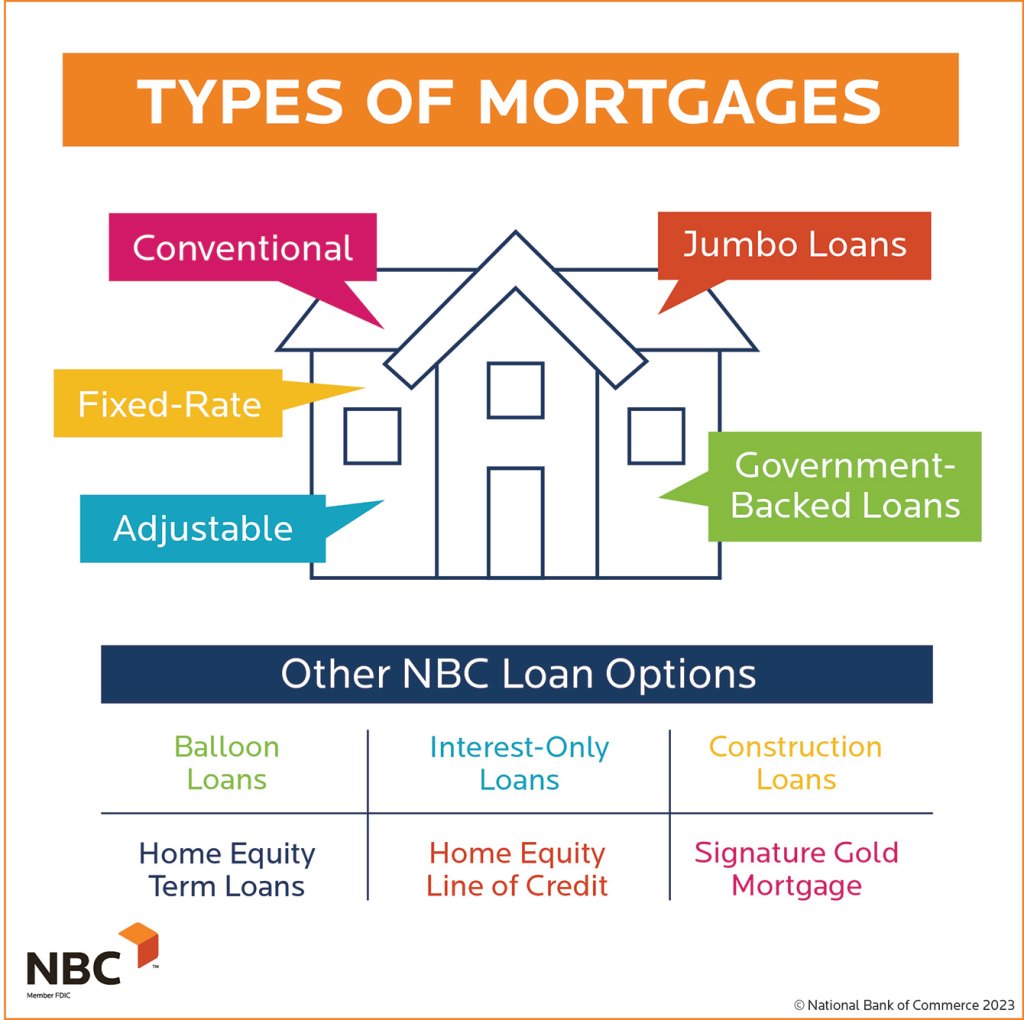

Types of Home Loans: Navigating Your Options

The world of home lending is not a one-size-fits-all scenario. A diverse array of loan products exists, each designed to cater to different financial situations, risk tolerances, and borrower profiles. Understanding these options is critical to choosing the loan that best suits your needs.

Conventional Loans

Conventional loans are the most common type of mortgage and are not insured or guaranteed by the federal government. They adhere to lending guidelines set by government-sponsored enterprises (GSEs) like Fannie Mae and Freddie Mac. To qualify for a conventional loan, borrowers typically need a good credit score (usually 620 or higher) and a solid debt-to-income ratio. If the down payment is less than 20% of the home’s purchase price, borrowers are usually required to pay Private Mortgage Insurance (PMI), which protects the lender in case of default. Conventional loans offer flexibility in terms and are often preferred by borrowers with strong financial credentials.

Government-Insured Loans (FHA, VA, USDA)

These loans are backed by various U.S. government agencies, making them more accessible to a broader range of borrowers, particularly those with less-than-perfect credit or lower down payments.

- FHA Loans: Insured by the Federal Housing Administration, FHA loans are popular among first-time homebuyers and those with lower credit scores (sometimes as low as 580 with a 3.5% down payment). While offering easier qualification, FHA loans require both upfront and annual mortgage insurance premiums, regardless of the down payment amount.

- VA Loans: Guaranteed by the Department of Veterans Affairs, VA loans are exclusive to eligible service members, veterans, and surviving spouses. A significant benefit is the ability to purchase a home with no down payment and no private mortgage insurance. Interest rates are often competitive, reflecting the government guarantee.

- USDA Loans: Backed by the U.S. Department of Agriculture, these loans are designed for low-to-moderate-income individuals purchasing homes in designated rural areas. They also offer no down payment options, making them highly attractive for qualifying buyers in eligible regions.

Adjustable-Rate Mortgages (ARMs) vs. Fixed-Rate Mortgages (FRMs)

One of the most fundamental distinctions in home lending is between fixed and adjustable interest rates.

- Fixed-Rate Mortgages (FRMs): With an FRM, the interest rate remains constant for the entire duration of the loan. This provides predictable monthly payments, making budgeting easier and protecting borrowers from potential interest rate increases. Common terms are 15, 20, or 30 years.

- Adjustable-Rate Mortgages (ARMs): ARMs feature an interest rate that is fixed for an initial period (e.g., 3, 5, 7, or 10 years) and then adjusts periodically based on a chosen market index. While ARMs often start with lower interest rates than FRMs, they introduce the risk of higher payments if rates rise after the fixed period. They can be appealing to borrowers who plan to sell or refinance before the adjustable period begins or those comfortable with interest rate volatility.

Jumbo Loans and Other Niche Products

For borrowers seeking to purchase homes that exceed the conforming loan limits set by Fannie Mae and Freddie Mac (which vary by region), a jumbo loan is necessary. These are non-conforming loans that often require higher credit scores, larger down payments, and more stringent underwriting criteria due to the increased risk associated with their size.

Beyond these, there are other specialized products like interest-only mortgages, construction loans, and physician loans, each catering to specific financial needs or professions. Researching these niche options can uncover tailored solutions for unique circumstances.

The Home Loan Application Process: A Step-by-Step Guide

Securing a home loan is a multi-stage process that requires meticulous preparation, thorough documentation, and patience. Understanding each step can help demystify the journey and minimize stress.

Pre-Approval: Setting Expectations

The first crucial step is obtaining a mortgage pre-approval. This involves providing a lender with your financial information (income, assets, debts), which they review to give you an estimate of how much you can borrow and at what interest rate. A pre-approval letter is not a guarantee of a loan but a strong indication of your borrowing capacity. It empowers you by setting a realistic budget for your home search and strengthens your offer to sellers, signaling that you are a serious and qualified buyer.

Gathering Necessary Documentation

Once you’re ready to apply for a specific loan, the documentation phase intensifies. Lenders will require a comprehensive set of documents to verify your financial standing. This typically includes:

- Proof of Income: Pay stubs, W-2 forms, tax returns (for the past two years), and bank statements. Self-employed individuals will need more extensive business financial records.

- Asset Verification: Bank statements, investment account statements, and documentation for any other assets.

- Debt Information: Credit card statements, student loan statements, auto loan statements, and any other outstanding debt obligations.

- Identification: Government-issued ID.

- Property Information: (Once an offer is accepted) Sales contract, property appraisal, and title insurance information.

This stage requires organization and promptness to keep the process moving forward efficiently.

Underwriting: The Lender’s Due Diligence

Underwriting is the most critical phase where the lender assesses the risk of lending to you. An underwriter meticulously reviews all submitted documents to verify your income, assets, credit history, and debt-to-income ratio. They also evaluate the property itself, typically through an appraisal, to ensure its value supports the loan amount. The underwriter’s job is to ensure that you meet all loan program guidelines and that the loan represents an acceptable risk for the lender. This stage can take several days to a few weeks, often involving requests for additional information or clarification.

Loan Approval and Closing

If the underwriting process is successful, you will receive a “clear to close” notification. This means your loan has been approved, and the lender is ready to finalize the transaction. The final step is the closing, where all parties (buyer, seller, lender, real estate agents, and closing agent/attorney) sign the necessary legal documents. During closing, you’ll review and sign the promissory note (your promise to repay the loan) and the mortgage or deed of trust (giving the lender a lien on the property). You’ll also pay closing costs, which are various fees associated with the transaction. Once all documents are signed and funds are disbursed, you officially become the homeowner.

Key Factors Influencing Your Home Loan

The terms and availability of your home loan are not arbitrary; they are the direct result of several financial and personal factors. Understanding these elements can empower you to improve your position before applying for a mortgage.

Credit Score and History

Your credit score is arguably the most influential factor. It’s a numerical representation of your creditworthiness, based on your payment history, amounts owed, length of credit history, new credit, and credit mix. Lenders use it to gauge your reliability in repaying debts. A higher credit score (e.g., 740+) typically qualifies you for lower interest rates and better loan terms, as you are perceived as a lower risk. Conversely, a lower score may result in higher rates or even loan denial. A strong credit history demonstrates responsible financial behavior over time.

Debt-to-Income (DTI) Ratio

Your DTI ratio is another critical metric. It compares your total monthly debt payments to your gross monthly income. Lenders use DTI to determine your ability to manage monthly payments and repay the loan. Generally, a lower DTI ratio (typically below 43-45%) is preferred, indicating you have sufficient disposable income to cover new mortgage payments without becoming overextended. It’s calculated in two ways: the “front-end” ratio (housing expenses only) and the “back-end” ratio (all monthly debts including housing).

Down Payment Amount

The amount of money you pay upfront for a home, known as the down payment, significantly impacts your loan. A larger down payment reduces the amount you need to borrow, which often translates to lower monthly payments and less interest paid over the life of the loan. It also signals to lenders that you have a significant financial stake in the property, reducing their risk. A down payment of 20% or more on a conventional loan often eliminates the need for Private Mortgage Insurance (PMI), saving you money.

Interest Rates and APR

The interest rate is the cost of borrowing money, expressed as a percentage of the loan amount. It directly determines how much extra you pay each month on top of the principal repayment. The Annual Percentage Rate (APR) is a broader measure of the total cost of the loan, including the interest rate plus certain fees and other charges (like origination fees, discount points, and some closing costs). When comparing loan offers, looking at the APR provides a more comprehensive picture of the true cost than just the interest rate alone. Market conditions, economic indicators, and the Federal Reserve’s policies greatly influence prevailing interest rates.

Loan Term and Repayment Structure

The loan term is the length of time you have to repay the loan, most commonly 15 or 30 years for fixed-rate mortgages.

- Shorter terms (e.g., 15 years): Generally come with lower interest rates and allow you to build equity faster and pay off the home sooner, but result in higher monthly payments.

- Longer terms (e.g., 30 years): Offer lower monthly payments, providing more financial flexibility, but typically accrue more interest over the life of the loan and take longer to build equity.

The repayment structure dictates how principal and interest are amortized over the loan term. Understanding this structure helps borrowers make informed decisions about their long-term financial commitments.

Managing Your Home Loan: Post-Approval Considerations

Obtaining your home loan is a major milestone, but it’s not the end of your financial journey. Effective management of your mortgage in the years following approval is crucial for long-term financial health and maximizing your investment.

Understanding Your Monthly Payments

Your monthly mortgage payment typically consists of four main components, often referred to as PITI:

- Principal: The portion of your payment that goes directly towards reducing the loan balance.

- Interest: The cost of borrowing the money, paid to the lender.

- Taxes: Property taxes, usually collected by the lender and held in an escrow account, then paid to the local government on your behalf.

- Insurance: Homeowner’s insurance premiums, also often held in escrow and paid by the lender. Additionally, if you have PMI or FHA/VA mortgage insurance, those premiums will also be part of your monthly payment.

Understanding how these components change over time (e.g., less interest and more principal paid as the loan matures) is key to financial planning.

Refinancing Options

Refinancing involves replacing your existing mortgage with a new one. Homeowners typically consider refinancing for several reasons:

- Lowering Interest Rates: If market interest rates have dropped significantly since you obtained your original loan, refinancing can secure a lower rate, reducing your monthly payments and total interest paid.

- Reducing Loan Term: Refinancing from a 30-year to a 15-year term can save substantial interest over time, though it increases monthly payments.

- Cash-Out Refinance: This allows homeowners to tap into their home equity by taking out a new, larger loan and receiving the difference in cash. This cash can be used for home improvements, debt consolidation, or other large expenses.

- Changing Loan Type: Switching from an ARM to a fixed-rate mortgage for stability, or vice versa if market conditions are favorable.

Refinancing involves new closing costs, so it’s important to analyze whether the long-term savings outweigh the upfront expenses.

Escrow Accounts and Property Taxes/Insurance

Most mortgages include an escrow account, managed by your lender. This account collects a portion of your monthly payment to cover property taxes and homeowner’s insurance premiums. The lender then pays these bills on your behalf when they are due. While convenient, it means you don’t directly control these funds. Lenders are required to conduct annual escrow analyses to ensure enough funds are collected. If property taxes or insurance premiums increase, your monthly mortgage payment will adjust accordingly. Understanding your escrow statements and annual adjustments is vital.

Strategies for Early Repayment

While the standard loan term is 15 or 30 years, many homeowners aim to pay off their mortgage sooner to save on interest and achieve financial freedom. Several strategies can facilitate early repayment:

- Making Extra Principal Payments: Even small, consistent extra payments directly to the principal can significantly shorten your loan term and reduce total interest.

- Bi-Weekly Payments: Instead of one monthly payment, making half a payment every two weeks results in 13 full monthly payments per year, effectively making an extra payment annually.

- Round Up Payments: Rounding your monthly payment up to the nearest hundred or another comfortable figure adds extra principal each month.

- Applying Windfalls: Using bonuses, tax refunds, or other unexpected income to make a lump-sum payment towards the principal.

Before implementing any early repayment strategy, ensure your lender doesn’t charge prepayment penalties and understand how to properly designate extra funds as principal-only payments.

Conclusion

Home lending is an indispensable component of the housing market, transforming the aspirational goal of homeownership into an achievable reality for millions. From understanding the fundamental distinction between a fixed-rate and an adjustable-rate mortgage to meticulously navigating the underwriting process and making informed decisions about loan management, every step requires careful consideration. A mortgage is not merely a debt; it is a powerful financial tool that, when understood and managed wisely, can be a cornerstone of personal wealth and long-term financial security. By thoroughly researching your options, diligently preparing for the application, and proactively managing your loan, you can unlock the full potential of homeownership and secure a stable financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.