The question, “How much is the mortgage rate today?” is perhaps one of the most critical queries for prospective homeowners, existing homeowners considering refinancing, and anyone keeping an eye on the broader economic health. Mortgage rates are not static; they are dynamic, influenced by a complex interplay of economic indicators, central bank policies, and global financial market movements. Understanding these underlying forces is paramount to making informed financial decisions that can impact your budget for decades.

For most people, a home represents their largest financial asset and their largest liability. The interest rate on a mortgage can mean the difference of hundreds, if not thousands, of dollars in monthly payments and tens of thousands over the loan’s lifetime. In a world where every percentage point matters, deciphering the current rate environment is not just about a single number; it’s about comprehending the mechanisms that shape it and leveraging that knowledge to secure the best possible terms for your financial well-being. This article will delve into the intricacies of mortgage rates, exploring the factors that drive them, the various loan types available, strategies for securing optimal rates, and how to effectively monitor the market today.

Understanding Mortgage Rates: More Than Just a Number

Before diving into the “how much” of today’s rates, it’s essential to grasp what a mortgage rate truly represents and why its fluctuations are so significant for personal finance.

What Exactly is a Mortgage Rate?

At its core, a mortgage rate is the cost you pay to borrow money for a home loan, expressed as a percentage of the loan amount. This percentage determines the interest portion of your monthly mortgage payment. It’s essentially the lender’s profit margin and compensation for the risk they take in lending you a large sum of money over an extended period. The lower the rate, the less you pay in interest over the life of the loan, resulting in lower monthly payments and greater financial flexibility.

Why Mortgage Rates Matter to Your Financial Future

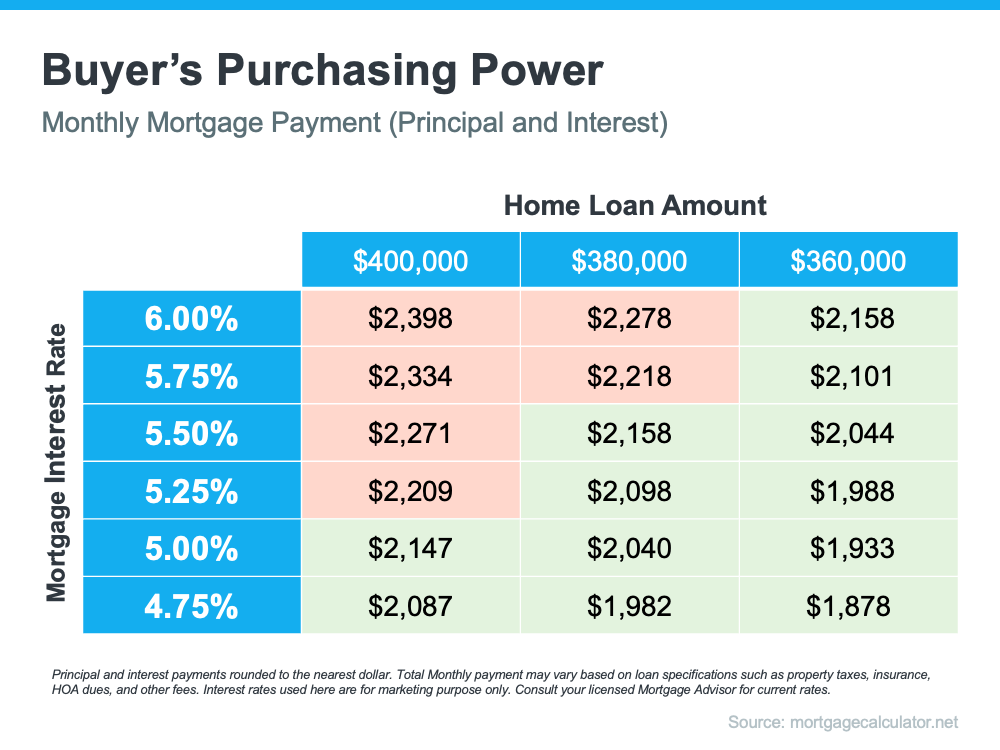

The impact of mortgage rates extends far beyond the immediate monthly payment. Over a 15-year or 30-year loan term, even a seemingly small difference of half a percentage point can accumulate into substantial savings or additional costs. For instance, on a $300,000 mortgage, a 0.5% difference in interest rate could mean tens of thousands of dollars saved or spent over the loan’s duration. This directly affects your overall wealth accumulation, your ability to save for retirement, or even your capacity to handle unexpected financial challenges. Furthermore, lower rates can increase your purchasing power, allowing you to afford a more expensive home within the same budget, or conversely, reducing the financial strain of your current home.

The Difference Between APR and Interest Rate

When shopping for a mortgage, you’ll encounter two key figures: the interest rate and the Annual Percentage Rate (APR). The interest rate is simply the cost of borrowing the principal amount. The APR, however, is a broader measure of the total cost of the loan, including the interest rate plus other charges such as origination fees, discount points, mortgage insurance, and other closing costs. While the interest rate tells you how much interest you’ll pay on the loan balance, the APR gives you a more comprehensive picture of the true annual cost of your loan. Comparing APRs across different lenders can be a more accurate way to assess which loan offers the best overall value.

Key Factors Driving Mortgage Rate Fluctuations

Mortgage rates are highly sensitive to a variety of economic and financial forces. Understanding these drivers is crucial for predicting potential shifts and making timely decisions.

The Federal Reserve’s Influence and Monetary Policy

The Federal Reserve, the U.S. central bank, does not directly set mortgage rates. However, its monetary policy decisions have a profound indirect impact. When the Fed raises or lowers the federal funds rate – the target rate for overnight borrowing between banks – it influences other interest rates throughout the economy. Higher federal funds rates typically lead to higher rates on various loans, including mortgages, as the cost of borrowing for lenders themselves increases. The Fed’s statements and actions regarding inflation, employment, and economic growth are closely watched by financial markets, directly affecting bond yields and, subsequently, mortgage rates.

Economic Indicators: Inflation, Employment, and GDP

Several key economic indicators provide insights into the health of the economy and influence the direction of mortgage rates:

- Inflation: High inflation erodes the purchasing power of money over time, making future loan repayments less valuable to lenders. To compensate for this, lenders typically demand higher interest rates during inflationary periods. Conversely, low inflation can allow rates to remain stable or even fall.

- Employment: A strong job market generally indicates a healthy economy, which can lead to increased consumer spending and potential inflationary pressures, pushing rates higher. A weak job market, on the other hand, might signal economic slowdowns, potentially leading to lower rates.

- Gross Domestic Product (GDP): GDP growth reflects the overall economic output. Robust GDP growth often accompanies economic expansion and can lead to higher interest rates as demand for money increases. Slow or negative GDP growth might prompt the Fed to lower rates to stimulate the economy.

The Bond Market’s Role: Specifically, 10-Year Treasury Yields

While the Fed influences short-term rates, long-term mortgage rates, especially for 30-year fixed loans, are more directly tied to the yield on the 10-year U.S. Treasury note. Mortgage-backed securities (MBS), which form the basis of most mortgages, compete with Treasury bonds for investor attention. When 10-year Treasury yields rise, MBS yields typically follow suit, pushing mortgage rates higher. Factors like investor sentiment, global economic events, and government debt levels all play a role in shaping these bond yields.

Lender-Specific Considerations: Your Credit Score and Down Payment

Beyond macroeconomics, individual borrower characteristics significantly impact the rate you receive.

- Credit Score: Lenders use your credit score (e.g., FICO score) as a primary indicator of your creditworthiness and repayment risk. Borrowers with excellent credit scores (typically 740+) are perceived as lower risk and qualify for the most favorable rates. A lower credit score suggests higher risk, leading to higher interest rates to compensate the lender.

- Down Payment: A larger down payment reduces the loan-to-value (LTV) ratio, meaning the borrower has more equity in the home from the outset. This reduces the lender’s risk and can lead to a better interest rate. A smaller down payment (e.g., less than 20%) often requires private mortgage insurance (PMI) and can result in a slightly higher rate.

Types of Mortgage Loans and Their Rate Structures

The type of mortgage you choose will fundamentally dictate how your interest rate behaves over time, influencing your long-term financial planning.

Fixed-Rate Mortgages: Stability in a Changing Market

The fixed-rate mortgage is the most common type, offering a consistent interest rate for the entire life of the loan (typically 15 or 30 years). This predictability means your principal and interest payments remain the same each month, regardless of market fluctuations. For homeowners seeking budgeting stability and protection against rising rates, fixed-rate mortgages are an attractive option. The downside is that you won’t benefit if market rates fall without refinancing, which incurs additional costs.

Adjustable-Rate Mortgages (ARMs): Balancing Initial Savings with Future Risk

Adjustable-Rate Mortgages (ARMs) offer an initial fixed-rate period (e.g., 3, 5, 7, or 10 years), after which the rate adjusts periodically based on a predetermined index (like LIBOR or SOFR) plus a margin. ARMs typically start with a lower interest rate than comparable fixed-rate mortgages, making them appealing for those who plan to sell or refinance before the fixed-rate period ends, or who anticipate higher future income. However, the risk lies in potential rate increases after the initial period, which can lead to significantly higher monthly payments. Most ARMs have caps on how much the rate can adjust per period and over the life of the loan, but substantial increases are still possible.

FHA, VA, and USDA Loans: Government-Backed Options

For specific borrower profiles, government-backed loans offer distinct advantages in terms of eligibility and rates:

- FHA Loans: Insured by the Federal Housing Administration, these loans are popular for first-time homebuyers or those with lower credit scores and smaller down payments (as low as 3.5%). While rates can be competitive, FHA loans require mortgage insurance premiums (MIP) for the life of the loan or until specific conditions are met, adding to the overall cost.

- VA Loans: Guaranteed by the Department of Veterans Affairs, these loans are available to eligible service members, veterans, and surviving spouses. VA loans offer significant benefits, including no down payment requirement and no private mortgage insurance. They often come with some of the most competitive interest rates on the market, recognizing the service of military personnel.

- USDA Loans: Backed by the U.S. Department of Agriculture, these loans are designed for low-to-moderate income borrowers purchasing homes in eligible rural areas. They also offer no down payment options and competitive rates but come with income limits and property location restrictions.

Strategies for Securing the Most Favorable Mortgage Rate

Even when rates are generally high, there are proactive steps you can take to position yourself for the best possible terms.

Improving Your Credit Profile: A Foundation for Better Rates

Your credit score is arguably the most impactful factor under your direct control. To improve it:

- Pay bills on time, every time: Payment history is the most significant factor in your credit score.

- Reduce outstanding debt: High credit utilization (the amount of credit you’re using compared to your available credit) can negatively impact your score.

- Avoid opening new credit accounts: This can temporarily lower your score.

- Check your credit report regularly: Dispute any errors that could be dragging down your score.

Aim for a credit score of 740 or higher to access the lowest rates.

The Power of a Substantial Down Payment

Lenders view a larger down payment as a sign of financial stability and reduced risk. Aiming for a 20% down payment or more can not only eliminate the need for private mortgage insurance (PMI) but also qualify you for a lower interest rate. Even if 20% isn’t feasible, saving as much as you can for a down payment will generally result in a better rate than a minimal down payment.

Shopping Around and Comparing Lender Offers

This is perhaps the most straightforward yet often overlooked strategy. Do not settle for the first offer you receive. Contact multiple lenders—banks, credit unions, and mortgage brokers—and compare their rates, fees, and APRs. A small difference in interest rate from one lender to another can save you thousands over the life of the loan. Use loan estimates to compare offers apples-to-apples, paying close attention to all closing costs.

Understanding Mortgage Points and Buy-Down Options

Mortgage points, also known as discount points, are fees paid to the lender at closing in exchange for a lower interest rate. One point typically costs 1% of the loan amount. For example, on a $300,000 loan, one point would be $3,000. Deciding whether to pay points depends on how long you plan to stay in the home. If you plan to stay long enough for the savings from the lower monthly payment to outweigh the initial cost of the points, it can be a financially sound decision.

What to Expect Today: Accessing Real-Time Rate Information and Future Outlook

While I cannot provide real-time, personalized mortgage rates, I can guide you on where to find the most current data and how to interpret market trends.

Where to Find Current Mortgage Rate Data

Several reputable online resources provide up-to-date mortgage rate information. Websites like Bankrate, Zillow, LendingTree, and NerdWallet regularly poll lenders and publish average daily rates for various loan types (30-year fixed, 15-year fixed, 5/1 ARM, etc.). Financial news outlets like Bloomberg, The Wall Street Journal, and CNBC also report on rate trends. Remember that these are often national averages, and your specific rate will depend on your financial profile and the lender you choose.

Interpreting Market Trends for Informed Decisions

When observing rate trends, pay attention to the overall direction. Are rates generally rising, falling, or holding steady? Look for expert analyses on what factors are currently dominating the market (e.g., inflation concerns, Fed announcements, global economic stability). Understand that daily fluctuations are normal, but sustained trends over weeks or months are more indicative of the market’s direction. If you see rates consistently declining, it might be a good time to lock in. If they’re rising, acting sooner rather than later could be advantageous.

Long-Term Outlook: Preparing for Future Rate Shifts

The mortgage rate environment is constantly evolving. While no one has a crystal ball, staying informed about economic forecasts, Fed projections, and global financial news can help you anticipate future shifts. For instance, if economists predict continued inflation, it’s reasonable to expect upward pressure on rates. Conversely, a projected economic slowdown might lead to lower rates. For homeowners, this foresight can inform decisions about refinancing, home equity lines of credit (HELOCs), or future property investments. Always consult with a qualified financial advisor or mortgage professional to tailor these general insights to your unique financial situation.

In conclusion, “how much is the mortgage rate today” is a question with a multi-faceted answer. It’s a dynamic figure influenced by macroeconomics and individual financial health. By understanding these complexities, diligently preparing your finances, and actively shopping for the best terms, you can confidently navigate the current mortgage landscape and secure a loan that aligns perfectly with your financial goals.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.