US Bank, a prominent institution in the American financial landscape, offers a comprehensive suite of banking services to millions of individuals, small businesses, and corporations. Understanding its geographical and operational footprint is crucial for anyone engaging with the bank, from a personal finance perspective to a business finance strategy. Beyond a simple address, “where is US Bank located?” delves into its strategic market presence, the accessibility of its financial tools, and its role in fostering economic activity across diverse regions. This exploration transcends mere brick-and-mortar locations, encompassing the vast digital infrastructure that defines modern banking and shapes the financial choices available to consumers and businesses alike.

A Comprehensive Footprint: Physical and Digital Reach

The concept of a bank’s “location” has evolved significantly. While physical branches and ATMs remain vital, the digital realm now constitutes a massive and increasingly critical aspect of a financial institution’s presence. US Bank strategically leverages both to provide widespread accessibility and convenience, directly impacting personal and business financial management.

The Extensive Branch Network: Serving Communities

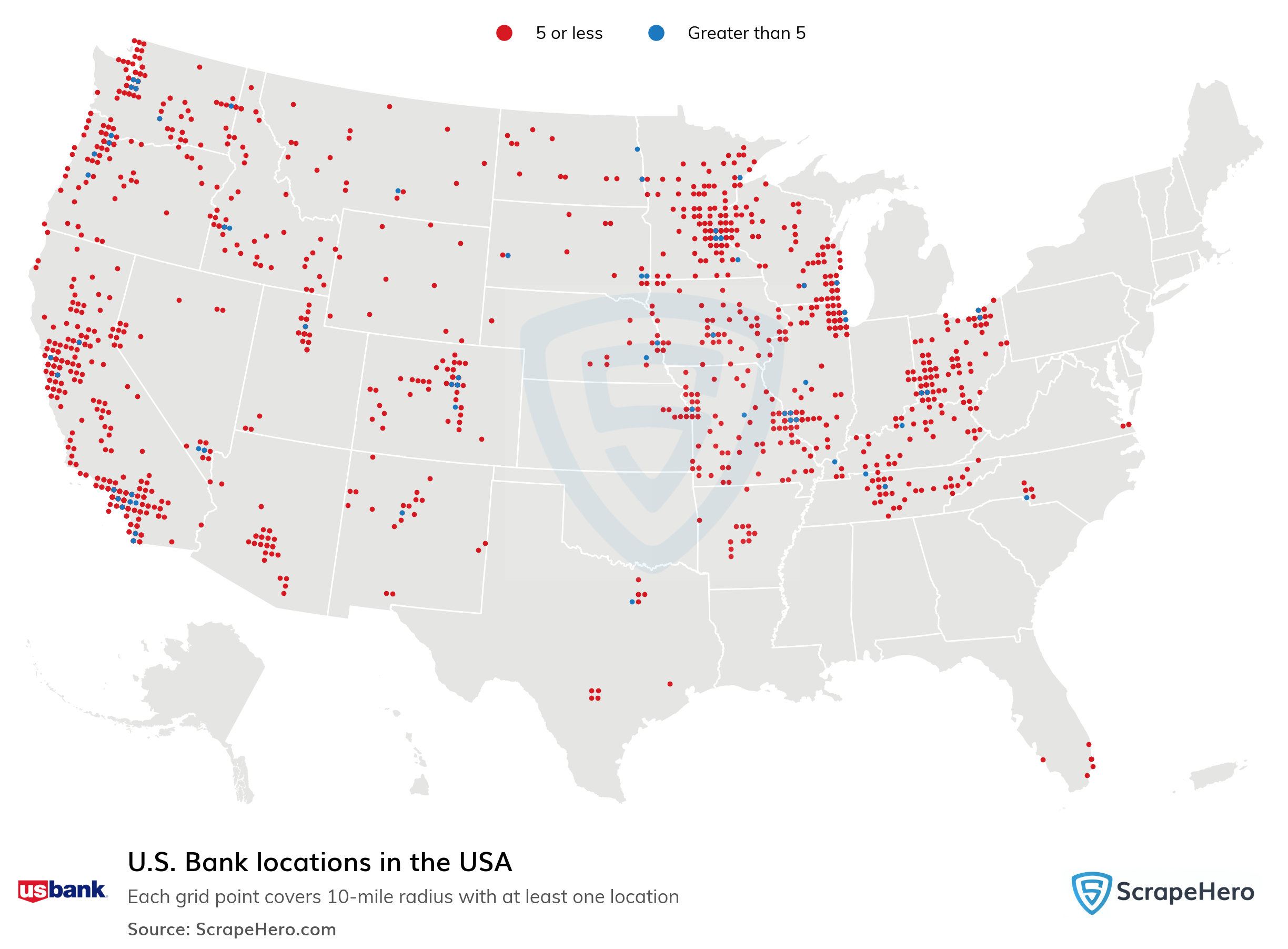

US Bank boasts a substantial physical presence, primarily concentrated in the Midwestern and Western United States, though its reach extends into many other regions. This extensive branch network is not merely a collection of buildings; it represents critical touchpoints for community engagement, offering personalized services that are often essential for complex financial transactions or for individuals who prefer face-to-face interaction. For personal finance, proximity to a branch can be crucial for opening accounts, applying for loans, resolving disputes, or accessing specialized advisory services. From a business finance perspective, a local branch presence can facilitate cash management, provide access to commercial lending officers, and foster relationships vital for local business growth. Each branch acts as a micro-economic hub, providing employment and contributing to the local financial ecosystem. The strategic placement of these branches often reflects demographic studies, economic growth patterns, and the bank’s commitment to serving specific markets, making it a critical aspect of their business strategy and financial accessibility.

ATM Access: Convenience at Your Fingertips

Complementing its branch network, US Bank provides widespread access to ATMs, ensuring that customers can manage their cash needs efficiently, regardless of their immediate proximity to a physical branch. This includes both proprietary US Bank ATMs and participation in surcharge-free networks, significantly expanding the convenience factor for routine transactions like withdrawals, deposits, and balance inquiries. For personal finance, the ubiquity of ATMs means less time spent searching for cash and more seamless management of daily expenses. For small businesses, particularly those with cash-intensive operations, easily accessible ATMs facilitate timely deposits and cash management, which is vital for operational liquidity. The ability to deposit checks or cash at an ATM extends banking hours virtually round the clock, offering unparalleled flexibility. This extensive ATM network underscores a core principle of modern financial services: to make banking as convenient and omnipresent as possible, thereby integrating financial tools more smoothly into the daily lives of customers.

The Digital Frontier: Online and Mobile Banking

Perhaps the most expansive “location” for US Bank today is its robust digital platform. Online banking through their website and the US Bank mobile app provides a virtual branch that is open 24/7, accessible from anywhere with an internet connection. This digital presence has revolutionized how individuals and businesses manage their finances. For personal finance, it offers the ability to check balances, pay bills, transfer funds, deposit checks via mobile capture, manage investments, and even apply for loans or credit cards without ever stepping into a physical location. For businesses, the digital platform provides sophisticated tools for treasury management, payroll services, business bill pay, fraud monitoring, and reporting, which are critical for operational efficiency and financial oversight. The geographical limitations of physical banking are completely removed in the digital space, allowing US Bank to serve customers nationwide and even internationally through online transactions. This digital location is continuously updated with new features, security enhancements, and user experience improvements, reflecting the bank’s investment in technology as a primary means of service delivery and market expansion.

Strategic Presence: Understanding US Bank’s Geographic Focus

The physical and digital locations of US Bank are not arbitrary; they are the result of deliberate strategic decisions aimed at maximizing market penetration, operational efficiency, and customer satisfaction. Understanding this strategic presence reveals much about the bank’s business model and its impact on the broader financial services industry.

Core Markets and Regional Strength

US Bank’s historical growth has led to a strong concentration in specific geographic regions, particularly the Midwest (where it originated) and the West Coast. This strategic focus allows the bank to build deep relationships within these communities, develop expertise in regional economic drivers, and tailor products and services to local needs. For businesses operating within these core markets, US Bank often represents a go-to financial partner with a strong understanding of the local economic landscape. For individuals, this regional strength can translate into more community-oriented banking, with staff who are familiar with local challenges and opportunities. While technology allows for broader reach, the concentrated physical footprint in these core markets signifies a commitment to traditional relationship banking, blending high-tech capabilities with high-touch service. This regional strength contributes significantly to the bank’s stability and market share within these areas, underpinning its financial performance and reputation.

The Headquarters: A Hub of Financial Operations

At the heart of US Bank’s extensive network lies its corporate headquarters in Minneapolis, Minnesota. This central location serves as the nerve center for all global operations, strategy development, risk management, and major financial decision-making. While customers rarely interact directly with the headquarters, its location is symbolic of the bank’s roots and its commitment to the region. From a business finance perspective, the headquarters houses the executive leadership, specialized financial departments, and technological infrastructure that drive the entire organization. Decisions made here influence interest rates, product offerings, investment strategies, and compliance frameworks that affect every customer and every branch. It’s the strategic command center that ensures the synchronized operation of thousands of branches and millions of digital interactions, making its location a crucial, albeit behind-the-scenes, element of “where US Bank is located.”

Expansion and Consolidation: Evolving Financial Landscapes

The banking industry is dynamic, characterized by periods of expansion and consolidation. US Bank’s footprint has evolved through organic growth, as well as strategic acquisitions and divestitures. These activities significantly alter where the bank is located, not just geographically but also in terms of market share and service offerings. Acquisitions, for instance, instantly expand the bank’s presence into new regions or deepen its existing presence, bringing new customers and branches under the US Bank umbrella. This can be beneficial for customers by offering more convenient locations and expanded services. Conversely, strategic divestitures or branch closures might occur in areas where the bank decides to optimize its resources. These changes reflect ongoing adjustments to market conditions, regulatory environments, and competitive pressures, all of which ultimately define the evolving “location” of US Bank’s services and its strategic financial positioning.

Navigating US Bank’s Locations: Tools and Resources

For customers, whether individuals managing personal budgets or businesses overseeing complex financial operations, knowing how to efficiently locate and interact with US Bank’s various presences is paramount. The bank provides several tools to simplify this process, ensuring accessibility to its financial services.

Leveraging the Branch Locator and Mobile App

The most direct way to find US Bank’s physical locations is through its official website’s branch and ATM locator tool or within the US Bank mobile app. These tools allow users to search for the nearest branch or ATM based on their current location or a specific address, often providing details such as hours of operation, available services (e.g., drive-thru, notary, safe deposit boxes), and contact information. For personal finance, this means quickly finding a nearby ATM for cash or a branch for a specific banking need. For business finance, the locator can help identify branches with specialized business banking services or those convenient for employees making deposits. The integration of these locators within digital platforms exemplifies how technology enhances access to physical services, bridging the gap between virtual and tangible banking experiences.

Understanding International Access and Services

While US Bank’s physical branch network is primarily concentrated within the United States, its digital presence and strategic partnerships offer certain international capabilities. Customers can manage their US-based accounts from anywhere in the world via online and mobile banking. Furthermore, US Bank credit and debit cards are widely accepted globally, and the bank offers international wire transfer services. While it doesn’t have a vast international branch network like some global banks, its robust digital infrastructure ensures that account holders can conduct essential financial activities and access their funds while abroad. This is particularly relevant for individuals traveling or living overseas and for businesses engaged in international trade, highlighting how “location” for financial services extends far beyond national borders through digital connectivity.

When Physical Location Still Matters: Specialized Services

Despite the rise of digital banking, there are still instances where a physical location remains indispensable. Specialized services like opening a trust, getting a mortgage, discussing complex investment strategies, or obtaining specific types of business loans often benefit from face-to-face consultations with financial experts. These interactions require a level of personal engagement and document handling that digital platforms, while advanced, may not fully replicate. Furthermore, situations requiring notary services, access to safe deposit boxes, or large cash transactions necessitate a physical branch. For these critical financial needs, understanding US Bank’s branch locations and their specific service offerings is essential, emphasizing that physical presence, though evolving, continues to play a vital role in a comprehensive financial services strategy.

The Financial Impact of Widespread Accessibility

The extensive physical and digital footprint of US Bank has profound implications for financial inclusion, convenience, and economic growth. Its strategically positioned locations contribute significantly to both individual and collective financial well-being.

Enhancing Customer Convenience and Financial Inclusion

A widespread presence, both physically and digitally, dramatically enhances customer convenience. For individuals, this means easier access to their funds, banking services, and financial advice, leading to better personal financial management. The ability to bank from anywhere, anytime, reduces barriers to financial participation, particularly for those in remote areas or with busy schedules. This accessibility is a cornerstone of financial inclusion, ensuring that a broader segment of the population can access essential banking services, build credit, save for the future, and achieve financial stability. By extending its reach, US Bank plays a vital role in democratizing access to financial tools, which is crucial for reducing economic disparities and empowering individuals.

Business Banking: Supporting Local and National Enterprises

For businesses, US Bank’s extensive network provides critical infrastructure for growth and stability. Local branches offer personalized support for small businesses, from setting up merchant services to securing working capital loans. The national reach, facilitated by both physical locations and digital platforms, supports larger corporations with complex banking needs across multiple states or even internationally. This enables seamless cash management, access to diverse financing options, and robust treasury services, all essential for operational efficiency and strategic expansion. By providing financial resources and expert advice, US Bank’s presence effectively acts as a catalyst for local economies and contributes to national economic development, demonstrating how a bank’s “location” translates directly into tangible economic impact.

Crisis Preparedness and Operational Resilience

The distribution of US Bank’s operational centers, data centers, and customer service hubs across various geographic locations also contributes to its operational resilience and crisis preparedness. In the event of a localized disaster or system outage, a geographically diverse infrastructure helps ensure business continuity and uninterrupted service delivery. This redundancy is critical for safeguarding customer assets and maintaining trust, particularly in a world prone to unforeseen events. For both personal and business finance, knowing that a financial institution has robust contingency plans built into its operational structure provides an invaluable layer of security and peace of mind. The strategic scattering of its “locations” in this context is not about customer convenience but about systemic stability and the continuous flow of financial services.

The Future of Banking Location: Blending Physical and Virtual

The landscape of banking locations is continuously evolving, driven by technological advancements, changing consumer preferences, and competitive pressures. US Bank, like other major financial institutions, is navigating this transformation by blending its traditional physical presence with innovative digital solutions.

Digital-First, Branch-Optional: Evolving Customer Preferences

A growing segment of the population, particularly younger generations, adopts a “digital-first” approach to banking. They prefer to conduct most, if not all, of their financial activities through online and mobile platforms, viewing physical branches as optional or necessary only for very specific needs. This shift in preference is prompting banks to invest heavily in their digital infrastructure, ensuring that the “virtual location” is robust, secure, and user-friendly. While physical branches may see reduced foot traffic, their role is evolving from transactional hubs to advisory centers, focusing on more complex financial planning and problem-solving. This future vision of “where US Bank is located” emphasizes flexibility, allowing customers to choose their preferred channel for interacting with their financial institution.

Hybrid Models: The Best of Both Worlds

The future of US Bank’s location strategy is likely to embrace a hybrid model that intelligently combines the strengths of both physical and digital channels. This means offering a seamless experience where customers can start a transaction online and finish it in a branch, or vice versa. Branches might become smaller, more technologically advanced, and focused on advisory services, while self-service kiosks and smart ATMs handle routine transactions. The goal is to provide convenience without sacrificing the human element when it’s most needed. This blended approach ensures that US Bank remains accessible to all customer segments, from those who are fully digital to those who value personal interaction, thereby maximizing financial inclusion and customer satisfaction across the board.

Security and Accessibility in a Distributed Network

As banking locations become more distributed and integrated across physical and digital spaces, maintaining robust security and ensuring universal accessibility become paramount. US Bank must continuously invest in cybersecurity measures to protect digital transactions and customer data, regardless of the access point. Similarly, accessibility features for individuals with disabilities must be integrated into both physical branch designs and digital platform interfaces, ensuring that everyone can access and utilize financial services effectively. The definition of “where US Bank is located” is therefore expanding to include not just physical addresses and IP networks, but also the secure, inclusive, and reliable channels through which financial services are delivered, making it a truly omnipresent and resilient financial partner.

In conclusion, “where US Bank is located” is a multi-faceted question with answers spanning a vast physical network, a pervasive digital presence, and a strategic operational core. This complex interplay of locations is designed to provide comprehensive financial services, enhance customer convenience, support economic activity, and ensure the resilience of its operations in an ever-changing financial world.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.