For many Americans, a car is not just a convenience but a necessity, an essential tool for commuting, errands, and family life. Yet, the cost of acquiring and maintaining a vehicle represents one of the most significant recurring expenses in a household budget, often second only to housing. Understanding “what is the average American car payment” is more than just a statistical curiosity; it’s a critical piece of information for financial planning, budgeting, and making informed decisions about one of life’s most substantial purchases.

In an economic landscape characterized by fluctuating interest rates, evolving vehicle technologies, and shifting consumer preferences, the average car payment is a dynamic figure. This article delves into the current averages, explores the myriad factors that influence these payments, and offers insights into how consumers can navigate the complexities of auto financing to secure a vehicle responsibly and affordably. By examining loan types, terms, and the broader financial implications, we aim to equip readers with the knowledge needed to make astute financial choices in the car market.

Unpacking the Current Average Car Payment Landscape

The automotive market continually shifts, influenced by supply chain dynamics, technological advancements, and economic conditions. Consequently, the average car payment is not a static number but rather a reflection of these ongoing changes. Understanding the latest figures provides a crucial benchmark for consumers considering a new vehicle purchase.

The Latest Figures: New vs. Used Cars

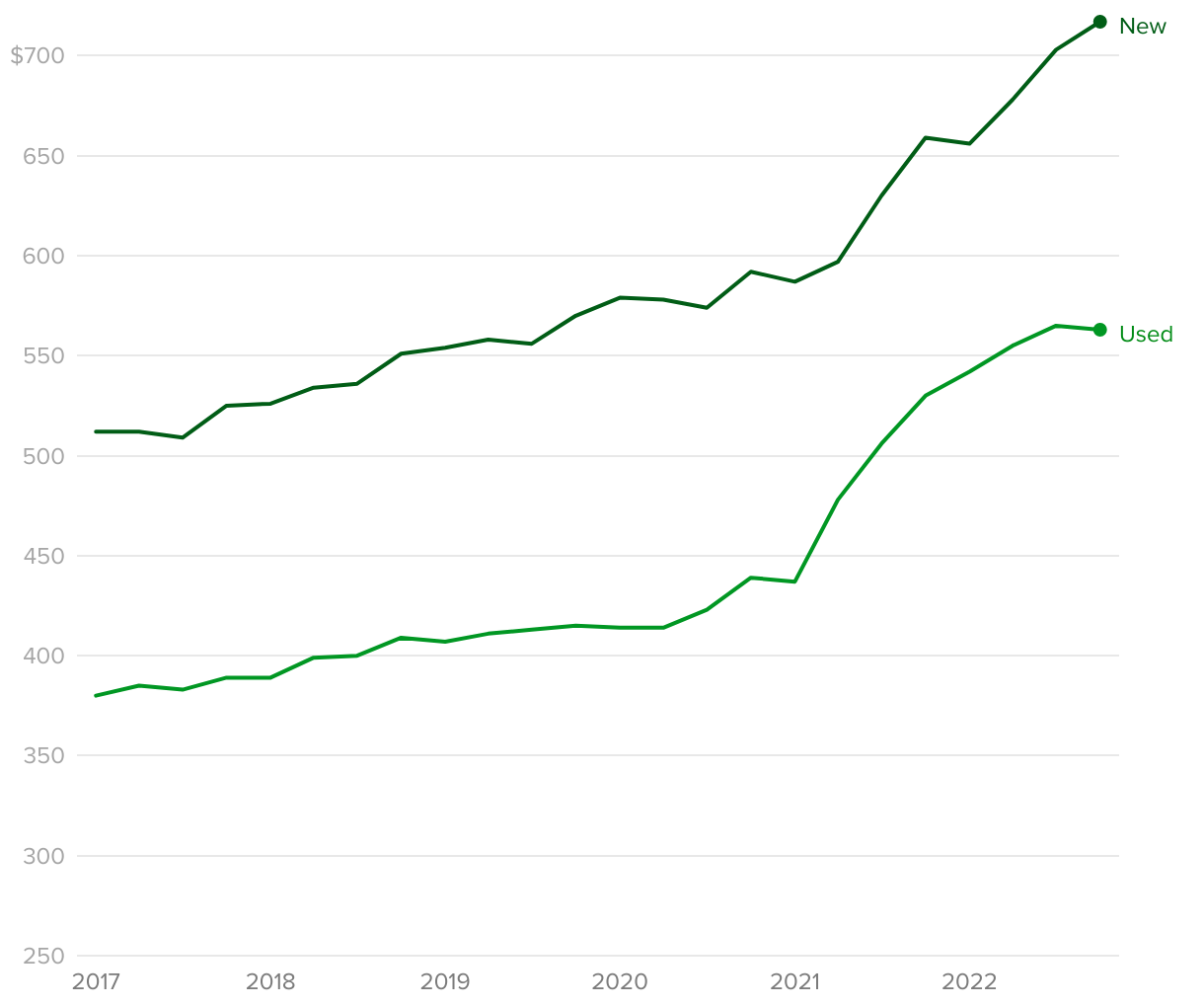

Recent data consistently reveals a significant disparity between average payments for new and used vehicles. As of late 2023 and early 2024, the average new car loan payment has frequently hovered around $700 to $750 per month. This figure represents a considerable increase over previous years, driven by higher vehicle prices, advanced features, and, at times, elevated interest rates. For used cars, while generally more affordable, payments have also seen an upward trend, often averaging in the range of $500 to $550 per month. This gap underscores the financial benefits of considering a pre-owned vehicle, particularly for budget-conscious buyers.

Understanding Loan Terms and Amounts

Beyond the monthly payment, the average loan term and the amount financed are critical components of the financing landscape. The typical auto loan term in the U.S. has stretched considerably, with many consumers opting for longer durations to make higher vehicle prices more manageable. Average loan terms for new cars often extend to 68-72 months (5.5 to 6 years), and sometimes even longer, up to 84 months (7 years). Used car loan terms, while often shorter, can still reach 60-65 months. While longer terms result in lower monthly payments, they also mean more interest paid over the life of the loan, ultimately increasing the total cost of ownership. The average amount financed for new vehicles has frequently surpassed $40,000, with used car financing often exceeding $25,000, reflecting the overall increase in vehicle prices across the board.

Key Factors Influencing Your Car Payment

While national averages provide a useful starting point, an individual’s actual car payment can vary wildly. This variability is primarily due to a confluence of personal financial circumstances, vehicle characteristics, and market conditions. Understanding these influential factors is crucial for anyone looking to optimize their auto financing.

Vehicle Price and Type

The most obvious determinant of a car payment is the vehicle’s sticker price. More expensive models—luxury cars, large SUVs, and high-end trucks—naturally command higher payments. Conversely, economy sedans or compact SUVs will typically result in lower monthly costs. The choice between a new and used vehicle also plays a pivotal role. New cars come with the immediate depreciation hit and often higher initial costs, while used cars, having already depreciated significantly, can offer a more budget-friendly entry point, despite potentially higher interest rates for older models.

Credit Score and Interest Rates

A consumer’s creditworthiness is a paramount factor. A strong credit score (typically FICO scores of 700+) signals to lenders a low risk of default, enabling access to the most favorable interest rates (Annual Percentage Rate or APR). Conversely, individuals with lower credit scores often face significantly higher APRs, which can drastically increase the total cost of the loan and, consequently, the monthly payment, even for the same vehicle and loan amount. Market interest rates, influenced by central bank policies and economic conditions, also dictate the baseline for auto loan rates, impacting everyone regardless of credit score.

Loan Term Length and Down Payment

The length of the loan term directly impacts the monthly payment. Spreading the cost over a longer period (e.g., 72 or 84 months) reduces the individual monthly outlay, making a vehicle seem more affordable. However, this strategy invariably leads to paying more interest over the loan’s lifetime. Conversely, shorter terms (e.g., 36 or 48 months) result in higher monthly payments but less total interest paid. A substantial down payment—the upfront cash paid at the time of purchase—is another powerful lever. A larger down payment reduces the principal amount financed, thereby lowering both the monthly payment and the total interest accrued, offering immediate and long-term financial benefits.

Trade-in Value and Fees

The value of a trade-in vehicle acts similarly to a down payment, reducing the total amount that needs to be financed. A strong trade-in can significantly lower your monthly payment. Additionally, various fees can subtly inflate the total cost of your loan. These include sales tax, registration fees, title fees, documentation fees from the dealership, and sometimes extended warranty costs or gap insurance premiums. While some of these are unavoidable, understanding and scrutinizing them can prevent unexpected increases in your overall financing obligation.

Navigating Car Financing Options

With the average car payment being a significant financial commitment, it’s essential for consumers to understand the various financing avenues available. Each option comes with its own set of advantages and disadvantages, impacting monthly payments, total costs, and long-term ownership prospects.

Auto Loans: Traditional vs. Refinancing

The traditional auto loan is the most common method for financing a vehicle purchase. This involves borrowing a specific amount from a lender (bank, credit union, or dealership finance department) to buy the car, then repaying it with interest over a set term. While convenient, the initial loan terms may not always be the most optimal. This is where refinancing comes into play. If your credit score has improved since your initial purchase, interest rates have dropped, or you simply want to adjust your monthly payment (either lower by extending the term or save interest by shortening it), refinancing can be a powerful tool. It involves taking out a new loan, often with better terms, to pay off your existing car loan, potentially saving you a substantial amount over the loan’s duration.

Car Leases: Pros and Cons

Leasing offers an alternative to outright ownership, providing access to a new car for a fixed period (typically 2-4 years) with a set monthly payment. Lease payments are generally lower than loan payments for a comparable new car because you are only paying for the depreciation of the vehicle during your lease term, not its full purchase price. This can be attractive for those who prefer driving a new car every few years with lower upfront costs and often include warranty coverage throughout the lease. However, leasing comes with mileage restrictions, potential penalties for excessive wear and tear, and no equity building. At the end of the lease, you either return the car, buy it out at a pre-determined residual value, or lease another vehicle.

The Role of Insurance and Maintenance Costs

While not directly part of the car payment, car insurance and maintenance costs are critical components of the total cost of car ownership and must be factored into your financial planning. Insurance premiums can vary dramatically based on the vehicle type, your driving record, location, and coverage choices. A higher-value car or a sports model will typically incur higher insurance costs. Similarly, maintenance, repairs, and fuel expenses are ongoing outlays. While new cars often come with factory warranties covering initial repairs, older vehicles might require more frequent and costly maintenance. Overlooking these “hidden” costs when budgeting for a car can lead to unexpected financial strain, making the monthly car payment seem less manageable in the broader context.

Strategies for Managing and Reducing Your Car Payment

Given the significant impact a car payment can have on one’s financial health, proactively managing and, if possible, reducing this expense is a smart financial move. There are several actionable strategies that consumers can employ before, during, and after the car buying process.

Budgeting and Affordability Assessment

The first and most crucial step is to determine what you can genuinely afford, not just what a lender approves you for. A common guideline is the “20/4/10 rule”: aim for a 20% down payment, finance the car for no more than four years, and ensure that your total car expenses (payment, insurance, fuel, maintenance) do not exceed 10% of your gross monthly income. This holistic approach ensures you don’t become “car-poor.” Thoroughly calculate your total cost of ownership by researching average insurance premiums, fuel efficiency, and maintenance costs for your desired vehicle, rather than focusing solely on the monthly loan payment.

Improving Your Financial Position

Before even stepping into a dealership, take steps to strengthen your financial standing. Prioritize improving your credit score by paying bills on time, reducing existing debt, and monitoring your credit report for errors. A higher credit score will unlock lower interest rates, directly translating to a lower monthly payment and less interest paid over time. Simultaneously, commit to saving for a larger down payment. The more you put down upfront, the less you need to borrow, which significantly reduces your monthly payment and overall interest costs. Even an extra few thousand dollars in a down payment can make a noticeable difference.

Smart Car Buying Choices

Be a savvy shopper. Consider purchasing a used or certified pre-owned (CPO) vehicle, which often offers excellent value as the steepest depreciation has already occurred. CPO vehicles also come with manufacturer-backed warranties, providing peace of mind similar to a new car. When you’re ready to buy, shop around for the best financing rates from multiple lenders—banks, credit unions, and online lenders—before engaging with dealership financing. This pre-approval gives you leverage during negotiations. Crucially, negotiate the total purchase price of the vehicle first, before discussing monthly payments. Focusing on the monthly payment can lead to extended loan terms or hidden fees that inflate the overall cost.

Broader Financial Implications of Car Payments

A car payment is more than just a line item on a budget; its size and duration can have profound ripple effects across an individual’s entire financial landscape, influencing everything from debt levels to long-term savings and future financial freedom.

Impact on Personal Debt and Savings Goals

A substantial or poorly managed car payment can significantly strain a household’s finances. It consumes a portion of disposable income that could otherwise be allocated to other critical financial goals, such as saving for a down payment on a home, funding retirement accounts, contributing to an emergency fund, or paying down higher-interest debts like credit cards. A high car payment also adds to your overall debt-to-income ratio, which lenders consider when evaluating applications for mortgages or other significant loans, potentially hindering your ability to secure future financing at favorable terms. The opportunity cost of funds tied up in an expensive vehicle can be immense, diverting resources from wealth-building activities.

Future Planning and Financial Freedom

For many, financial freedom is a long-term objective, characterized by reduced debt, robust savings, and flexibility in financial decision-making. The choices made regarding car payments directly influence this trajectory. Opting for an affordable vehicle with a manageable loan can accelerate progress towards financial goals, freeing up cash flow for investments, savings, or even pursuing entrepreneurial ventures. Conversely, committing to an overly expensive car with an extended loan term can create a persistent financial burden, delaying key milestones like early retirement, financial independence, or even simply having the flexibility to change careers or take time off without financial stress. Aligning car purchases with long-term financial health means viewing the vehicle as a tool that supports your life goals, not an impediment to them.

Conclusion

Understanding “what is the average American car payment” offers a valuable snapshot of current market trends, but it is ultimately a starting point for individual financial planning. As we’ve explored, numerous factors—from vehicle choice and credit score to loan terms and down payments—collectively determine the final monthly obligation. Beyond the payment itself, the broader costs of ownership, including insurance and maintenance, demand careful consideration.

Making informed decisions about auto financing goes beyond simply securing a vehicle; it’s about making a choice that aligns with your personal financial goals, preserves your budget, and contributes positively to your long-term financial well-being. By researching diligently, improving your financial position, and employing smart buying strategies, you can navigate the complexities of car payments and ensure your vehicle ownership experience enhances, rather than detracts from, your pursuit of financial stability and freedom.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.