Embarking on the journey of retirement planning can feel like navigating a complex maze. Among the most fundamental and effective tools at your disposal is the Individual Retirement Account (IRA). Often lauded as a cornerstone of personal finance, an IRA offers a tax-advantaged way to save for your golden years, empowering you to build wealth steadily over time. However, the initial question for many is often, “Where do I even begin?”

This article will demystify the process, guiding you through the essential considerations, various types of IRAs, and the diverse platforms available to help you kickstart your retirement savings. Whether you’re a seasoned investor or taking your first step into the world of personal finance, understanding where to start an IRA is a crucial step towards securing your financial future. We’ll delve into the nuances that empower you to make an informed decision, ensuring your retirement savings grow efficiently and effectively.

Understanding the Foundation: What is an IRA and Why You Need One

Before diving into the “where,” it’s vital to grasp the “what” and “why” behind an IRA. An Individual Retirement Account is not an investment itself, but rather a special type of account that holds investments, offering significant tax benefits designed to encourage long-term savings for retirement. Unlike employer-sponsored plans like a 401(k), an IRA is opened by an individual, providing greater control and flexibility.

The Core Concept of an IRA

At its heart, an IRA is a savings vehicle with tax advantages. It allows your money to grow over time, often shielded from immediate taxes, until you reach retirement age. The specific tax benefits depend on the type of IRA you choose, but the underlying principle is consistent: incentivizing long-term savings through government-backed tax breaks. These accounts can hold a wide range of investments, including stocks, bonds, mutual funds, exchange-traded funds (ETFs), and certificates of deposit (CDs), giving you the freedom to tailor your portfolio to your risk tolerance and financial goals. The power of compounding, where your earnings generate further earnings, is amplified within an IRA due to its tax-advantaged status, making it an incredibly potent tool for wealth accumulation.

The Indisputable Benefits of IRAs

The “why” of opening an IRA is compelling, anchored by several key advantages:

- Tax Advantages: This is the primary draw. Depending on the IRA type, contributions might be tax-deductible in the current year (Traditional IRA), or withdrawals in retirement might be entirely tax-free (Roth IRA). This allows more of your money to work for you, rather than being siphoned off by taxes each year. The ability for investments to grow tax-deferred or tax-free significantly boosts your potential returns over decades.

- Compounding Growth: IRAs harness the power of compound interest, a phenomenon where your investment returns themselves earn returns. With the tax benefits, this compounding effect is supercharged, enabling substantial growth over your working life. A small, consistent contribution made early in your career can grow into a significant sum by retirement due to this exponential growth.

- Control and Flexibility: Unlike some employer plans, an IRA gives you complete control over your investment choices. You can select specific stocks, bonds, or funds that align with your personal investment philosophy. This self-directed nature empowers you to actively manage your retirement savings, making adjustments as your financial situation or market conditions evolve.

- Accessibility (with caveats): While primarily for retirement, certain circumstances allow for penalty-free withdrawals before age 59½, such as for a first-time home purchase or qualified higher education expenses. This offers a degree of flexibility not always found in other retirement vehicles, though it’s generally wise to avoid early withdrawals to preserve the long-term growth potential.

Navigating the Landscape: Choosing the Right Type of IRA

The IRA umbrella covers several distinct types, each designed to cater to different financial situations and goals. Understanding these differences is critical to selecting the option that best serves your long-term interests. The two most common and widely utilized are the Traditional IRA and the Roth IRA, but specialized options exist for specific needs.

Traditional IRA: The Immediate Tax Break

A Traditional IRA allows you to contribute pre-tax dollars, meaning your contributions may be tax-deductible in the year they are made. This can lower your taxable income in the present, leading to an immediate tax savings. Your investments then grow tax-deferred, meaning you don’t pay taxes on capital gains or dividends year-to-year. However, withdrawals in retirement are taxed as ordinary income.

- Who it’s for: Ideal for individuals who expect to be in a lower tax bracket in retirement than they are now. It’s also a good choice for those who want an immediate tax deduction and meet the income requirements for deductibility (which are dependent on whether you or your spouse are covered by a retirement plan at work). There are no income limitations to contribute to a Traditional IRA, but income limits do affect the deductibility of contributions if you’re covered by a workplace retirement plan.

Roth IRA: The Future Tax Break

With a Roth IRA, you contribute after-tax dollars. This means your contributions are not tax-deductible in the current year. The magic of the Roth IRA lies in its withdrawals: once you reach age 59½ and have held the account for at least five years, all qualified withdrawals—both contributions and earnings—are completely tax-free.

- Who it’s for: Best suited for those who anticipate being in a higher tax bracket in retirement than they are currently, or those who simply prefer to pay taxes now and enjoy tax-free income later. Roth IRAs also offer more flexibility, as contributions can be withdrawn tax- and penalty-free at any time. However, there are income limitations to contribute directly to a Roth IRA, making it inaccessible for very high earners (though a “backdoor Roth” strategy can sometimes bypass this).

Employer-Sponsored IRAs: SEP and SIMPLE

While less common for the average individual looking to “start an IRA,” it’s worth noting these variations:

- SEP IRA (Simplified Employee Pension): Primarily for self-employed individuals and small business owners, a SEP IRA allows employers to contribute to their employees’ (and their own) retirement accounts. Contribution limits are significantly higher than Traditional or Roth IRAs.

- SIMPLE IRA (Savings Incentive Match Plan for Employees): Another option for small businesses (typically with 100 or fewer employees), a SIMPLE IRA requires employer contributions, either as a matching contribution or a fixed percentage of salary.

Deciding Between Traditional and Roth

The choice between Traditional and Roth largely hinges on your current income, expected future income, and tax bracket.

- If you’re in a high tax bracket now and expect to be in a lower one in retirement, a Traditional IRA’s immediate tax deduction might be more appealing.

- If you’re in a lower tax bracket now or expect your income (and thus your tax bracket) to increase significantly in the future, a Roth IRA’s tax-free withdrawals in retirement could be immensely valuable.

- Consider your eligibility based on income limits. If you earn too much to contribute directly to a Roth, a Traditional IRA might be your only direct option, or you might explore a backdoor Roth conversion.

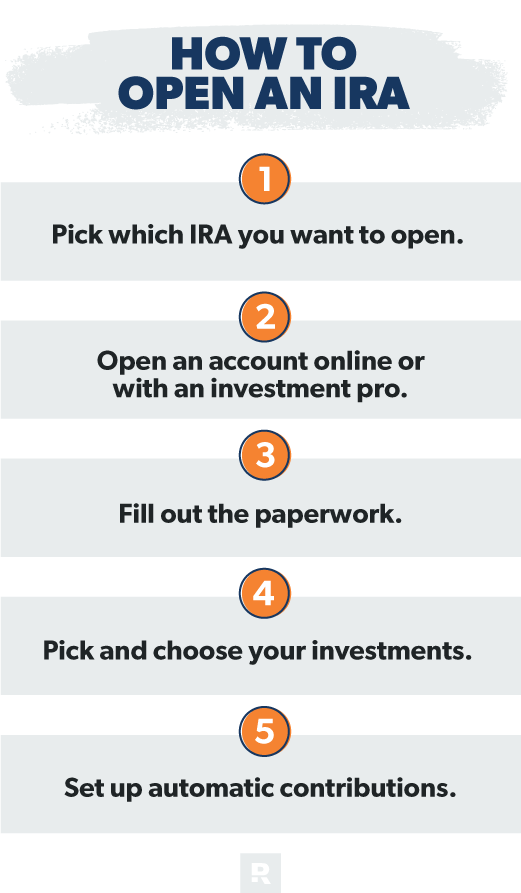

Pinpointing Your Provider: Where to Open Your IRA Account

Once you’ve decided on the type of IRA that aligns with your financial strategy, the next crucial step is selecting the right financial institution to host your account. The marketplace offers a variety of providers, each with its own strengths and ideal customer profile. Your choice will largely depend on your preferred level of involvement, investment knowledge, and cost sensitivity.

Online Brokerages: The DIY Investor’s Hub

Online brokerages are arguably the most popular choice for opening an IRA, particularly for individuals who prefer to manage their own investments. These platforms provide a vast array of investment options and powerful tools for self-directed investors.

- Features: They typically offer access to a wide spectrum of investment products, including individual stocks, bonds, mutual funds, ETFs, and options. Many boast low or zero commission fees for stock and ETF trades, extensive research materials, educational resources, and sophisticated trading platforms.

- Who it’s for: Experienced investors, those who enjoy researching and selecting their own investments, or individuals comfortable with a do-it-yourself approach.

- Examples: Fidelity, Vanguard, Charles Schwab, E*TRADE, TD Ameritrade (now Schwab). These firms are known for their robust platforms, competitive fees, and strong customer support. Vanguard, for instance, is famous for its low-cost index funds and ETFs.

Robo-Advisors: Automated Investing Made Simple

Robo-advisors represent a newer, tech-driven approach to investing. They use algorithms to build and manage diversified portfolios based on your risk tolerance, financial goals, and timeline.

- Features: They offer automated portfolio management, including rebalancing and tax-loss harvesting, often with low minimum investment requirements and lower fees than traditional human advisors. They typically invest in low-cost ETFs.

- Who it’s for: Beginners, busy professionals, or investors who prefer a hands-off approach and appreciate automation. They’re excellent for those who want expert-designed portfolios without the high cost of a personal financial advisor.

- Examples: Betterment, Wealthfront, M1 Finance. These platforms make investing accessible and straightforward, ideal for setting it and forgetting it.

Traditional Banks and Credit Unions: Familiarity and Limited Options

You might be tempted to open an IRA at your existing bank or credit union for convenience. While familiar, this option often comes with limitations for retirement investing.

- Features: Often provide a limited range of investment options, primarily focused on CDs or savings accounts, which may not offer the growth potential needed for long-term retirement savings. Fees can sometimes be higher for brokerage services if they offer them.

- Who it’s for: Individuals who prioritize simplicity and keeping all their accounts under one roof, or those who are extremely risk-averse and prefer ultra-safe (though low-growth) investments like CDs.

- Examples: Chase, Bank of America, Wells Fargo. While they offer IRAs, their investment selection for long-term growth is typically less diverse than dedicated brokerages or robo-advisors.

Financial Advisors: Personalized Guidance for Complex Needs

For individuals with complex financial situations, substantial assets, or those seeking comprehensive financial planning beyond just an IRA, a dedicated financial advisor can be invaluable.

- Features: Personalized investment strategies, holistic financial planning (including estate planning, tax planning, insurance), and ongoing guidance. This often comes with higher fees (e.g., a percentage of assets under management or hourly rates).

- Who it’s for: High-net-worth individuals, those with intricate financial situations, or anyone who desires a high level of personalized service and expert guidance.

Making the Smart Choice: Factors to Consider When Selecting a Provider

Choosing where to open your IRA is a decision that can significantly impact your long-term returns and overall investing experience. Beyond simply picking a name you recognize, several key factors warrant careful consideration to ensure you select the best fit for your unique needs.

Fees and Commissions: Minimizing Your Costs

Fees, even small ones, can erode your returns over decades. Prioritizing low costs is paramount.

- Trading Fees/Commissions: Many online brokerages now offer commission-free trading for stocks and ETFs. Ensure you understand any fees for mutual funds or other specific investments.

- Expense Ratios: This is a crucial fee for mutual funds and ETFs, representing the annual percentage of your investment that goes to fund management. Opt for funds with low expense ratios (e.g., under 0.20%). Vanguard and Fidelity are known for their low-cost index funds and ETFs.

- Account Maintenance Fees: Some providers charge annual fees for IRAs, especially if your balance falls below a certain threshold. Look for providers that offer no-fee IRAs.

- Advisory Fees: If you opt for a robo-advisor or human financial advisor, understand their advisory fee structure (e.g., a percentage of assets under management).

Investment Options: Matching Your Strategy

The range and quality of investment products offered by a provider are critical, as they dictate how you can build and diversify your retirement portfolio.

- Variety of Assets: Does the platform offer stocks, bonds, ETFs, mutual funds, and other instruments you’re interested in?

- Access to Specific Funds: If you have a preference for particular fund families (e.g., Vanguard, iShares), ensure the provider offers them, ideally without transaction fees.

- Research Tools and Education: Look for platforms that provide robust research tools, analytical charts, and educational materials to help you make informed investment decisions.

- Managed Portfolios: If you prefer a hands-off approach, evaluate the quality and cost of pre-built or robo-managed portfolios.

User Experience and Customer Support: Ease of Management

A user-friendly platform and reliable customer service can make a significant difference in your investing journey, especially for new investors.

- Online Platform and Mobile App: Is the website intuitive and easy to navigate? Does the mobile app provide all the functionality you need on the go?

- Customer Service: How can you reach customer support (phone, chat, email)? Are they responsive and knowledgeable? This becomes crucial if you encounter issues or have questions.

- Educational Resources: Does the provider offer webinars, articles, or tutorials to help you understand investing better?

Minimum Balance Requirements: Getting Started Easily

Some providers require a minimum amount to open an account or to invest in certain funds.

- Initial Deposit: Many online brokerages and robo-advisors now have no minimums or very low minimums (e.g., $0 or $100) to open an IRA.

- Investment Minimums: Be aware that some mutual funds may have higher minimum investment requirements, even if the account itself has a low or no minimum.

The Final Steps: Opening and Funding Your IRA

Once you’ve identified the ideal provider and IRA type, the process of opening and funding your account is relatively straightforward. The key is to gather the necessary information beforehand and understand the contribution limits to maximize your retirement savings.

Gathering Your Information

Before you start the online application, have the following documents and information readily accessible:

- Personal Identification: Your Social Security Number (SSN) or Taxpayer Identification Number (TIN), and potentially a driver’s license or state ID.

- Contact Information: Your current address, phone number, and email.

- Employment Information: Your employer’s name and address (if applicable), especially if you’re also covered by a workplace retirement plan, as this can affect IRA deductibility.

- Bank Account Details: Your bank account number and routing number for electronic fund transfers to fund your IRA.

The Application Process

Most IRA applications can be completed online in a matter of minutes.

- Select Account Type: Clearly specify that you want to open an IRA and then choose between a Traditional, Roth, SEP, or SIMPLE IRA.

- Provide Personal Details: Fill in all required personal information accurately.

- Designate Beneficiaries: This is a crucial step. You’ll name primary and contingent beneficiaries who will inherit the assets in your IRA upon your passing, bypassing the probate process.

- Agree to Terms: Review the terms and conditions carefully before electronically signing.

Funding Your IRA

After your account is approved, the next step is to get money into it.

- Contribution Methods: The most common ways to fund your IRA are:

- Electronic Funds Transfer (EFT): Linking your bank account for direct transfers.

- Check Deposit: Mailing a check to the provider.

- Rollover: If you’re moving funds from an old 401(k) or another retirement account, you can initiate a direct rollover (recommended for tax purposes) or an indirect rollover.

- Contribution Limits: Be mindful of the annual IRA contribution limits set by the IRS. For 2023, the limit is $6,500 (or $7,500 if you’re age 50 or older). For 2024, it increases to $7,000 (or $8,000 for age 50 and over). These limits apply across all your Traditional and Roth IRAs combined.

Choosing Your Investments

Once funds are in your IRA, the final step is to invest them.

- Asset Allocation: Decide on a mix of different asset classes (e.g., stocks, bonds) based on your risk tolerance and time horizon. Younger investors typically lean more towards stocks for higher growth potential, while those closer to retirement might favor bonds for stability.

- Diversification: Spread your investments across various companies, industries, and geographies to reduce risk.

- Long-Term Perspective: Remember that IRAs are long-term vehicles. Avoid making emotional decisions based on short-term market fluctuations. Stick to your investment plan and periodically rebalance your portfolio as needed.

Starting an IRA is a powerful step towards building financial security and achieving your retirement dreams. By understanding the types of IRAs available, carefully selecting a provider that aligns with your needs, and consistently contributing, you put yourself on a trajectory for a comfortable and financially independent future. The sooner you start, the more time your money has to grow, thanks to the magic of compounding and tax advantages. Don’t delay—your future self will thank you.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.