In an increasingly interconnected world, the ability to transfer funds seamlessly and securely has become a cornerstone of both personal and business finance. From splitting dinner bills with friends to sending remittances to family abroad, and from paying contractors to managing household expenses, the methods we use to move money have evolved dramatically. What was once a slow, paper-based process is now often instant, digital, and accessible from the palm of your hand. This evolution, driven by technological advancements and consumer demand for efficiency, has introduced a plethora of options, each with its own benefits, drawbacks, and specific use cases. Understanding these various methods is not merely a matter of convenience; it’s a critical component of effective personal financial management, ensuring your money goes where it needs to, when it needs to, without unnecessary costs or risks.

This guide delves into the diverse landscape of fund transfer mechanisms, offering a professional and insightful overview for anyone looking to navigate the complexities of sending money. We will explore everything from traditional banking solutions to modern digital payment platforms, dissecting their operational nuances, security implications, and financial considerations. By the end, you’ll be equipped with the knowledge to make informed decisions, choosing the most suitable, cost-effective, and secure method for every scenario.

The Evolving Landscape of Personal Fund Transfers

The journey of money transfer has undergone a profound transformation, mirroring the broader shifts in technology and global connectivity. For centuries, the act of sending money was a physical endeavor, involving cash, precious metals, or handwritten checks. The advent of telegraphs and later, electronic banking, began to digitize the process, but it was the internet and mobile technology that truly revolutionized how individuals and businesses exchange funds.

From Cash to Digital: A Brief History

Historically, sending money over distance was fraught with risk and inconvenience. Early methods relied on couriers or the postal service, which were slow, expensive, and vulnerable to loss or theft. The introduction of money orders in the mid-19th century offered a slightly more secure alternative, allowing individuals to send funds through post offices or authorized agents. Bank transfers, initially reserved for large commercial transactions, gradually became accessible to the public, offering a more robust and secure channel, albeit often accompanied by significant delays and fees.

The late 20th and early 21st centuries ushered in the digital age of finance. The widespread adoption of credit and debit cards laid the groundwork for electronic payments. However, it was the rise of online banking and, critically, peer-to-peer (P2P) payment platforms in the early 2000s that democratized money transfers. Services like PayPal demonstrated the immense potential of digital platforms to facilitate quick, convenient, and relatively inexpensive transfers, bypassing some of the traditional banking hurdles. Today, with smartphones in nearly every pocket, mobile payment apps have become indispensable tools, allowing instant transfers with just a few taps.

Why Understanding Payment Methods Matters

In this rich ecosystem of payment options, choosing the right method is paramount for several reasons directly related to personal finance. Firstly, cost efficiency varies wildly. Some services levy flat fees, others charge a percentage of the transaction, and international transfers often involve unfavorable exchange rates or hidden markups. Understanding these costs can save significant amounts over time. Secondly, speed and convenience are critical. While some situations demand instant transfers, others allow for slower, potentially cheaper alternatives. Thirdly, security and reliability are non-negotiable. Each method carries different levels of risk concerning fraud, data breaches, and transaction disputes. Lastly, accessibility and recipient preferences play a role. Not everyone has access to the same digital tools, and some recipients may prefer traditional methods, especially in less digitally mature regions. A comprehensive understanding empowers you to balance these factors, optimizing your financial transactions.

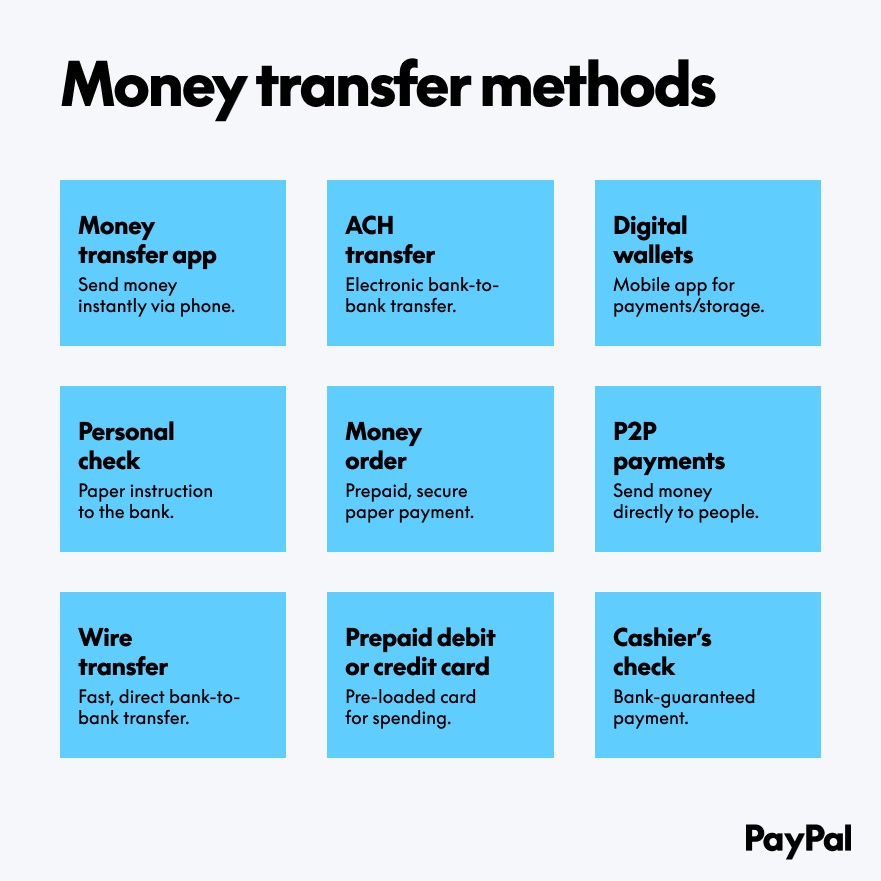

Domestic Payment Solutions: Convenience and Choice

Within national borders, the options for sending money are abundant, ranging from established banking services to innovative digital apps. The choice often hinges on the urgency, amount, and relationship with the recipient.

Bank-Centric Methods: Wires, ACH, and Checks

Traditional banks remain a cornerstone for many domestic money transfers, offering reliable, albeit sometimes slower, services.

- Bank Wire Transfers: These are direct, electronic transfers of funds from one bank account to another. Wires are generally very fast, often completing within hours, and are considered highly secure. They are irreversible once sent, making them suitable for large, time-sensitive transactions like real estate closings or down payments. However, wires typically come with higher fees, ranging from $20 to $50 per transaction, and require precise recipient bank details.

- Automated Clearing House (ACH) Transfers: ACH transfers are electronic payments processed through a centralized system that batches transactions. They are commonly used for direct deposits of paychecks, automatic bill payments, and inter-bank transfers. ACH transfers are much cheaper, often free for standard transfers, but they are significantly slower than wires, typically taking 1-3 business days to clear. They are ideal for recurring payments or non-urgent transfers where cost-effectiveness is a priority.

- Paper Checks: Despite the rise of digital payments, checks still hold a place, especially for less frequent, non-urgent payments or when a physical record is preferred. They are inexpensive to issue but can take several days to clear once deposited. The primary drawbacks include the potential for fraud (bounced checks, forged signatures) and the manual effort involved in writing, mailing, and depositing them. For most modern transactions, digital alternatives have largely superseded checks due to their convenience and speed.

Peer-to-Peer (P2P) Payment Apps: The Modern Standard

P2P payment apps have revolutionized how individuals send money to each other domestically, making it as simple as sending a text message. These apps link directly to your bank account, debit card, or credit card, facilitating near-instant transfers.

- Zelle: Integrated directly into many banking apps, Zelle allows users to send money directly from their bank account to another person’s account, usually within minutes. It’s often free for users, making it a highly attractive option for quick domestic transfers. However, Zelle transactions are irreversible, and it’s generally recommended for sending money to people you know and trust. Transaction limits are typically set by individual banks.

- Venmo: Popular for its social features and ease of use, Venmo facilitates transfers between friends for things like splitting bills, rent, or groceries. While standard transfers from a Venmo balance or linked bank account are free, instant transfers to a debit card incur a small fee (e.g., 1.75%, minimum $0.25). Users can also fund payments with credit cards, but this usually comes with a 3% fee. Venmo is primarily for domestic, personal use.

- Cash App: Similar to Venmo, Cash App allows users to send and receive money, often instantly and without fees for standard transfers from a linked bank account or debit card. It also offers features like direct deposit, a debit card, and even allows users to buy and sell Bitcoin and stocks. Credit card payments incur a 3% fee, and instant transfers to a bank account typically cost a small percentage. Cash App is widely used for peer-to-peer payments and small business transactions.

- PayPal: As one of the pioneers in digital payments, PayPal offers a robust platform for sending and receiving money both domestically and internationally. Sending money to friends and family within the U.S. from a linked bank account or PayPal balance is free. Using a debit or credit card for personal payments usually incurs a fee. PayPal is versatile, supporting personal payments, online purchases, and business transactions, often with buyer and seller protection.

When to Use Each Method: A Decision Framework

The best method depends on your specific needs:

- For large, urgent, high-value transfers (e.g., house down payment): Bank Wire Transfer (despite the cost).

- For regular, scheduled, low-cost transfers (e.g., paying rent, direct deposit): ACH Transfer.

- For quick, free transfers to trusted individuals (e.g., splitting a bill): Zelle or Venmo (if both parties use it).

- For personal payments with some flexibility and potentially social features: Venmo or Cash App.

- For versatile personal or business payments, including online purchases: PayPal.

- When a physical record is paramount or the recipient prefers it: Paper Check (with caution).

Navigating International Money Transfers

Sending money across borders introduces additional layers of complexity, including exchange rates, varying regulations, and a wider array of specialized services. The goal remains the same: to get money from point A to point B efficiently, securely, and cost-effectively.

Specialized Remittance Services: Global Reach, Local Impact

For international transfers, specialized remittance services often offer better exchange rates and lower fees compared to traditional banks.

- Wise (formerly TransferWise): Known for its transparent pricing and “real” mid-market exchange rates, Wise is a favorite for international transfers. It uses a peer-to-peer matching system or local transfers to minimize fees. Wise supports transfers to over 80 countries, offering various delivery speeds and payment options (bank transfer, debit/credit card). It’s generally one of the most cost-effective options for bank-to-bank international transfers.

- Xoom (a PayPal service): Xoom specializes in international money transfers, allowing users to send money for cash pickup, bank deposit, or even home delivery in many countries. It’s often fast, with some transfers completing in minutes. Fees and exchange rates can vary significantly by country and payment method, but it leverages PayPal’s extensive network for convenience.

- Western Union and MoneyGram: These are legacy services known for their vast global networks, enabling cash pick-up in remote locations where banking infrastructure might be limited. They offer various sending options (online, app, agent location) and delivery methods. While incredibly widespread, their exchange rates and fees can sometimes be less favorable than purely digital platforms, especially for larger amounts. They are often preferred when the recipient doesn’t have a bank account or needs cash quickly in person.

Bank International Wires: The Traditional Global Pathway

Traditional banks offer international wire transfers through networks like SWIFT (Society for Worldwide Interbank Financial Telecommunication). These are highly secure and reliable for large sums, but they typically involve:

- Higher Fees: Often ranging from $30-$50 per transfer, and sometimes more if intermediary banks are involved.

- Less Favorable Exchange Rates: Banks may add a significant markup to the interbank exchange rate, reducing the amount the recipient receives.

- Longer Processing Times: While often marketed as “fast,” international wires can take 1-5 business days to clear, especially if multiple correspondent banks are involved.

- Detailed Information Required: You’ll need the recipient’s full bank details, including SWIFT/BIC codes and sometimes an IBAN.

Cryptocurrency for Cross-Border Payments: An Emerging Alternative

Cryptocurrencies like Bitcoin and Ethereum, or stablecoins pegged to fiat currencies (e.g., USDC, USDT), present an intriguing, albeit volatile, alternative for international transfers.

- Potential Benefits: Extremely fast transaction times (minutes, not days), potentially lower fees (especially for large sums), and bypasses traditional banking intermediaries, which can be advantageous in regions with strict capital controls.

- Challenges: High price volatility (though stablecoins mitigate this), complexity of use for the uninitiated, regulatory uncertainty, and the need for both sender and receiver to have cryptocurrency wallets and understand how to convert to/from local currency. While promising for certain use cases and tech-savvy users, it’s not yet a mainstream solution for most.

Securing Your Financial Transactions

Regardless of the method chosen, security must be a top priority. Financial fraud and scams are pervasive, making vigilance and adherence to best practices essential for protecting your money and personal information.

Protecting Against Fraud and Scams

Scammers constantly evolve their tactics, but common themes involve preying on urgency, emotion, or lack of information.

- Verify the Recipient: Always double-check the recipient’s name, email, phone number, and account details. A small typo can send your money to the wrong person, and most digital transfers are irreversible. If in doubt, contact the person directly through a known, alternative channel (not the one requesting the money).

- Beware of Urgent Requests: Scammers often create a sense of urgency, impersonating family members in distress, government agencies, or tech support to pressure you into sending money quickly. Always pause, verify, and question such requests.

- “Too Good to Be True” Offers: Be extremely skeptical of unsolicited offers that promise large returns for a small upfront payment, or lottery winnings that require you to send money to claim them.

- Public Wi-Fi Risks: Avoid conducting financial transactions over unsecured public Wi-Fi networks, as they can be vulnerable to eavesdropping.

Data Security and Privacy

Your personal and financial data is valuable. Protecting it is crucial to prevent identity theft and unauthorized access to your accounts.

- Strong, Unique Passwords: Use complex passwords that are different for each financial account. Consider a reputable password manager.

- Two-Factor Authentication (2FA): Enable 2FA on all financial apps and services. This adds an extra layer of security, typically requiring a code from your phone in addition to your password.

- Monitor Account Activity: Regularly review your bank statements and transaction history for any unfamiliar activity. Report suspicious transactions immediately.

- Understand Privacy Policies: Be aware of how the platforms you use collect, store, and share your data.

Transaction Limits and Regulatory Compliance

Financial institutions and payment services impose transaction limits for various reasons, including security, fraud prevention, and regulatory compliance.

- Daily/Weekly Limits: Most P2P apps and banks have limits on how much you can send in a single transaction or over a specific period. Be aware of these if you plan to send large sums.

- KYC (Know Your Customer) and AML (Anti-Money Laundering) Regulations: To combat financial crime, services often require users to verify their identity (e.g., with a driver’s license or passport). This might be necessary to unlock higher transaction limits or use international transfer services. Compliance with these regulations is crucial for the integrity of the financial system.

Making Informed Choices: Cost, Speed, and Reliability

Ultimately, the best way to send money is the one that best meets your specific needs while being cost-effective, secure, and reliable. This requires a careful consideration of several factors.

Deconstructing Transfer Fees: Hidden vs. Overt

Fees can significantly impact the final amount a recipient receives.

- Flat Fees vs. Percentage Fees: Some services charge a fixed amount per transaction, while others take a percentage of the transferred sum. For small amounts, a percentage fee might be less; for large amounts, a flat fee might be more economical.

- Exchange Rate Markups: For international transfers, the exchange rate offered by a service can be more important than the explicit fee. Many providers embed a profit margin into their exchange rate, effectively charging a hidden fee. Always compare the offered exchange rate against the mid-market rate (what you see on Google or Reuters) to understand the true cost.

- Third-Party Fees: Be aware that intermediary banks in international wires can levy their own charges, further reducing the received amount.

The Urgency Factor: Instant vs. Standard Transfers

Speed comes at a price.

- Instant Transfers: Methods like Zelle, instant P2P app transfers, or wire transfers are fast, but may incur higher fees or come with strict limits. Use them when time is of the essence.

- Standard Transfers: ACH transfers or regular P2P transfers linked to a bank account are slower but often free or significantly cheaper. Choose these when you have a few days to spare.

Reliability and Support: What to Look For

A reliable service offers peace of mind.

- Customer Service: Evaluate the availability and responsiveness of customer support. What happens if a transaction goes wrong? Is there a clear dispute resolution process?

- Trackability: Can you track the status of your transfer? Many services provide real-time updates, which is invaluable, especially for international transfers.

- Reputation and Reviews: Check reviews and ratings from other users to gauge a service’s overall reliability and user experience.

Empowering Financial Mobility

The landscape of money transfers is dynamic, offering an unprecedented array of choices for individuals and businesses alike. From the instant gratification of P2P apps to the robust security of bank wires, and the global reach of specialized remittance services, there’s a solution for nearly every need. By understanding the underlying mechanics, dissecting the associated costs, prioritizing security, and aligning your choice with the urgency and nature of your transaction, you can harness these tools to manage your finances with greater efficiency and confidence.

The ability to send people money is more than just a convenience; it’s a critical component of modern financial literacy and a key enabler of economic activity. As technology continues to evolve, so too will the methods we employ to move money. Staying informed, exercising due diligence, and adapting to new innovations will ensure that your financial mobility remains seamless, secure, and always in your control.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.