In the dynamic landscape of personal finance, mobile payment applications like Cash App have become indispensable tools for managing money. For many users, understanding the nuances of how these platforms facilitate the movement of funds is crucial. When we talk about “withdrawal” on Cash App, we’re delving into a fundamental aspect of personal finance: accessing your digital funds in a tangible or readily spendable form. It’s more than just a transaction; it’s the bridge between your Cash App balance and your everyday financial needs, whether that’s paying bills, making purchases, or simply having cash in hand.

This article will meticulously explore what withdrawal truly signifies within the Cash App ecosystem, breaking down the financial implications, available methods, associated costs, and strategic considerations for managing your money effectively. Our focus will remain exclusively on the “Money” category, examining how these features impact your personal finance decisions, budgeting, and overall financial well-being.

Understanding the Essence of Withdrawal on Cash App

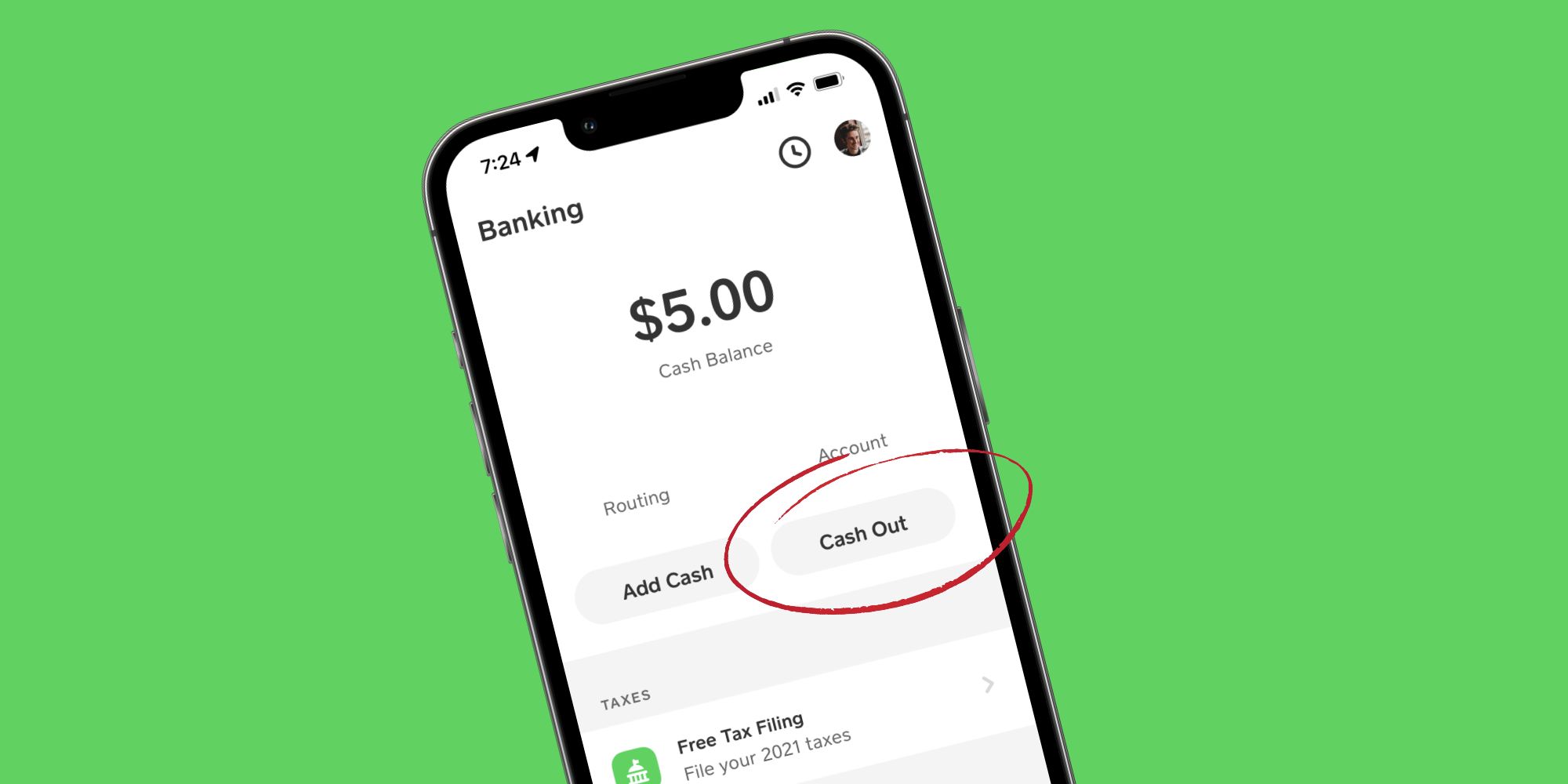

At its core, a withdrawal on Cash App refers to the process of transferring funds from your Cash App balance to an external account or converting it into physical cash. It’s the action of taking money out of your Cash App account, making it accessible for use outside the app’s immediate payment functionalities. This capability is vital for users who receive payments, transfer money, or simply store funds within their Cash App and eventually need to utilize those funds in traditional financial systems or for immediate cash needs.

The Core Concept of Withdrawing Funds

The concept of withdrawal is a cornerstone of banking and financial services, extended and streamlined by fintech platforms. On Cash App, your balance represents funds digitally held by the platform. When you initiate a withdrawal, you are essentially instructing Cash App to move a specified amount from this digital balance to a destination of your choice. This could be your linked bank account, a physical ATM, or even for direct deposits to a conventional checking or savings account. The significance lies in empowering users to control their money, ensuring liquidity and accessibility when and where it’s needed most. Without effective withdrawal options, Cash App would merely be a holding platform, severely limiting its utility as a comprehensive financial tool.

Why Withdraw Funds from Cash App?

Users withdraw funds from Cash App for a myriad of financial reasons, each rooted in personal finance management. One primary reason is to consolidate funds into a central bank account, making it easier to manage overall finances, pay bills, or save. For individuals who receive income or payments via Cash App, withdrawing allows them to transfer these earnings to their primary bank, where they might have recurring payments set up or wish to build their savings.

Another crucial reason is the need for physical cash. While digital payments are increasingly prevalent, there are still many instances where cash is king—think small businesses, gratuities, or simply managing daily spending with physical money. The ability to withdraw cash directly from an ATM using the Cash Card addresses this specific financial need. Furthermore, some users withdraw funds to move money between different financial institutions, perhaps to take advantage of better interest rates, pay down specific debts, or fund investments held elsewhere. Each withdrawal decision is ultimately a personal financial strategy designed to align with individual spending habits, budgeting goals, and broader financial planning.

Navigating Your Withdrawal Options

Cash App offers several flexible withdrawal methods, each designed to cater to different user needs regarding speed, convenience, and cost. Understanding these options is paramount for making financially savvy choices that align with your personal cash flow requirements.

Standard vs. Instant Withdrawals: Speed and Cost

The most common distinction in Cash App withdrawals lies between “Standard” and “Instant” transfers to a linked bank account.

-

Standard Withdrawal: This option typically takes 1-3 business days for the funds to arrive in your linked bank account. Critically, Cash App does not charge a fee for standard withdrawals. From a personal finance perspective, this is the most cost-effective method for moving funds when time is not an immediate constraint. It’s ideal for routine transfers, managing income received on Cash App, or consolidating funds for future bill payments where the deadline is not imminent. Prioritizing standard transfers helps you retain more of your money by avoiding unnecessary fees, a key principle of sound financial management.

-

Instant Withdrawal: As the name suggests, this method provides immediate access to your funds, typically depositing them into your linked debit card account within minutes. However, this speed comes at a cost: Cash App charges a 0.5% to 1.75% fee for instant transfers, with a minimum fee of $0.25. While this fee might seem small, it adds up over time and can eat into your available funds. Instant withdrawals are financially justified primarily for urgent situations, such as unexpected expenses, emergency cash needs, or time-sensitive bill payments that cannot wait for a standard transfer. It’s crucial to weigh the convenience against the cost and only opt for instant transfers when the immediate need outweighs the financial penalty.

ATM Withdrawals with the Cash Card

For those requiring physical cash, the Cash Card offers a convenient solution. The Cash Card is a free, customizable debit card linked directly to your Cash App balance. Once activated, you can use it to make purchases anywhere Visa is accepted and, more importantly, withdraw cash from ATMs.

- Financial Utility: The Cash Card essentially transforms your digital Cash App balance into a readily spendable and withdrawable asset. This is incredibly useful for budgeting, as you can allocate specific funds to your Cash App for daily spending and ATM withdrawals, effectively separating it from your primary bank account.

- Fees and Reimbursements: While Cash App generally charges a $2 fee for ATM withdrawals if you don’t have direct deposits set up, it offers a significant financial benefit: users who receive at least $300 in direct deposits to their Cash App account each month qualify for instant ATM fee reimbursements (both the $2 Cash App fee and the ATM operator’s fee). This feature can lead to substantial savings for regular ATM users, making the Cash Card a highly competitive option for cash access, especially for those who route their payroll or other income through Cash App. This directly impacts personal finance by reducing transaction costs.

Direct Deposits to Your Linked Bank Account

While technically a withdrawal mechanism, the most direct way to move funds from Cash App to your traditional banking system is via linking your bank account. Cash App allows you to link a bank account using your account and routing numbers. This enables you to send your Cash App balance directly to your bank account using either the standard or instant withdrawal options described above. This integration is vital for personal financial management, as it allows seamless transfer of funds received on Cash App into your main financial hub, where you might manage savings, investments, or recurring bill payments. It ensures that funds don’t remain isolated within the Cash App ecosystem but are fluidly integrated into your broader financial strategy.

Fees, Limits, and Financial Considerations

Understanding the financial constraints and costs associated with withdrawals is paramount for responsible money management on Cash App. Ignoring these details can lead to unexpected expenses or limitations that hinder your access to funds.

Deconstructing Withdrawal Fees

As previously touched upon, withdrawal fees are a critical financial consideration.

- Instant Withdrawal Fee: This is the most common fee users encounter. Ranging from 0.5% to 1.75%, this percentage can add up, especially for larger sums. For instance, withdrawing $500 instantly could cost you between $2.50 and $8.75. While seemingly minor, consistent instant withdrawals can erode your savings or available funds over time. Astute financial planning involves minimizing these fees by opting for standard transfers whenever possible.

- ATM Withdrawal Fee: The $2 Cash App fee for ATM withdrawals (if direct deposit requirements aren’t met) combined with potential third-party ATM operator fees means each cash withdrawal can incur a notable cost. Strategically, setting up direct deposits to Cash App can eliminate these fees, making the Cash Card a more financially attractive option for cash access. This highlights how leveraging specific features can significantly improve your personal finance efficiency.

Understanding Daily and Weekly Limits

Cash App implements withdrawal limits for security and regulatory compliance. These limits dictate how much money you can withdraw within specific timeframes.

- ATM Withdrawal Limits: Typically, Cash App users can withdraw up to $300 per transaction, $1,000 per day, and $1,000 per week from ATMs. These limits are subject to change and may vary based on your account verification status.

- Bank Transfer Limits: While Cash App doesn’t always explicitly state maximum bank transfer limits, fully verified accounts generally have higher limits, often allowing transfers of up to $25,000 per week.

These limits are crucial for financial planning, especially for individuals managing larger sums or those who rely on Cash App for significant income. It’s important to understand your current limits by checking your app’s settings and to plan your withdrawals accordingly to avoid hitting a cap when you urgently need funds. For business finance or those with high transaction volumes, these limits necessitate careful budgeting and potentially using other financial tools in conjunction with Cash App.

Best Practices for Cost-Effective Withdrawals

To maximize your money and minimize costs, consider these best practices:

- Prioritize Standard Transfers: Whenever you don’t need immediate access to funds, always opt for the free standard transfer to your linked bank account. This is the simplest way to avoid instant withdrawal fees.

- Leverage Direct Deposit for ATM Fee Reimbursements: If you frequently need cash, consider routing at least $300 of your monthly income (e.g., salary, government benefits, or even regular transfers from another account) to your Cash App balance. This activates the ATM fee reimbursement feature, saving you money on every withdrawal.

- Plan Large Withdrawals: If you need to withdraw a substantial amount, plan ahead to utilize standard transfers. For sums exceeding daily ATM limits, multiple withdrawals over several days or a direct bank transfer might be necessary.

- Monitor Your Balance: Keep a close eye on your Cash App balance and anticipate your spending needs. This proactive approach helps you decide the most appropriate and cost-effective withdrawal method in advance.

Ensuring Secure and Smooth Withdrawals

Security is paramount in personal finance, and Cash App provides various measures to protect your funds during withdrawals. Understanding these features and adopting best practices can prevent financial losses and ensure a seamless experience.

Verifying Your Identity for Enhanced Security

Cash App strongly encourages and often requires identity verification for higher transaction limits and enhanced security. This usually involves providing your full legal name, date of birth, and the last four digits of your Social Security Number (SSN).

- Financial Safeguard: Verification helps prevent fraud and unauthorized access to your funds. By confirming your identity, Cash App can better protect your account from malicious actors attempting to withdraw your money.

- Increased Flexibility: A verified account often unlocks higher withdrawal limits, giving you greater financial flexibility and reducing the chances of hitting caps when you need to access larger sums. This aligns with responsible financial management by allowing you to move your money as needed, while still maintaining security.

Troubleshooting Common Withdrawal Issues

Even with careful planning, withdrawal issues can arise. Common problems include failed transfers, delays, or incorrect amounts.

- Failed Transfers: This can happen due to incorrect bank details, insufficient funds, or exceeding withdrawal limits. Always double-check your linked bank account information before initiating a transfer.

- Delayed Funds: While instant transfers are usually quick, technical glitches can occur. For standard transfers, remember business days exclude weekends and holidays. If a standard transfer takes longer than 3 business days, contact Cash App support.

- Account Verification: Many issues stem from unverified accounts encountering strict limits. Ensure your identity is fully verified within the app.

- Contact Support: If you encounter persistent problems, the first step is always to contact Cash App support through the app. They can provide specific insights into your transaction status and help resolve technical issues, which is crucial for protecting your financial assets.

Protecting Your Funds: Security Tips

Beyond identity verification, a few proactive steps can safeguard your money:

- Enable Security Locks: Always use a PIN, Touch ID, or Face ID to secure your Cash App account. This prevents unauthorized access even if your phone is lost or stolen.

- Beware of Scams: Be vigilant against phishing attempts, fake customer support, or schemes promising unrealistic returns. Cash App will never ask for your PIN or sign-in code outside the app. Protecting your login credentials is a fundamental aspect of digital financial security.

- Monitor Activity: Regularly review your transaction history for any suspicious activity. Report unauthorized transactions immediately to Cash App support. Prompt action is key to recovering funds in case of fraud.

- Strong, Unique Passwords: Use a strong, unique password for your email associated with Cash App and never reuse passwords.

Optimizing Your Cash App Withdrawal Strategy

Integrating Cash App effectively into your overall personal finance strategy requires a thoughtful approach to withdrawals, ensuring you maximize convenience while minimizing costs and risks.

When to Use Each Withdrawal Method

- Standard Withdrawal (Free, 1-3 business days): Best for routine transfers, consolidating funds, or receiving income when there’s no immediate urgency. This should be your default choice to preserve your money.

- Instant Withdrawal (0.5% – 1.75% fee, instant): Reserve this for genuine emergencies, immediate bill payments, or time-sensitive transactions where the cost is justified by the urgency. Factor the fee into your immediate budget.

- Cash Card ATM Withdrawal (Potential $2 fee + ATM operator fee, immediate cash): Ideal for when you need physical cash. Maximize its value by setting up direct deposits to get ATM fee reimbursements, effectively making cash access free.

- Cash Card for Purchases (Free, instant): While not a withdrawal in the traditional sense, using your Cash Card directly for purchases avoids the need to withdraw cash or transfer to another bank, potentially saving you fees and streamlining spending from your Cash App balance.

Integrating Cash App into Your Personal Finance

Cash App is more than just a money transfer tool; it can be a significant component of your personal financial ecosystem. By strategically managing your withdrawals, you can optimize its role:

- Budgeting Tool: Use Cash App to receive a portion of your income and manage specific spending categories. Withdraw funds to your primary bank for larger expenses or savings, maintaining a clear separation for budgeting purposes.

- Emergency Fund Access: Keep a small emergency fund within Cash App for instant access, accepting the instant transfer fee as the cost of immediate liquidity.

- Streamlined Payments: Receive payments from side hustles or freelance work directly into Cash App, then strategically withdraw to your main account or use the Cash Card for expenses.

- Financial Flexibility: Leverage Cash App to move money quickly between accounts or access cash, providing flexibility in managing your liquidity across different financial needs.

In conclusion, “withdrawal” on Cash App is a multifaceted financial action that offers users various ways to access their money. By understanding the different methods, their associated costs, and security considerations, users can make informed choices that align with their personal finance goals, ensuring efficient, cost-effective, and secure management of their digital funds. Integrating Cash App thoughtfully into your financial strategy can empower you with greater control and flexibility over your money.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.