In the evolving landscape of digital finance, peer-to-peer payment applications like Cash App have become indispensable tools for managing everyday transactions. Offering convenience for sending, receiving, and even investing money, Cash App has revolutionized how many individuals interact with their finances. However, beneath the surface of its user-friendly interface lies a structured system of financial limits designed to ensure security, comply with regulations, and manage risk. Understanding these thresholds is crucial for any user, whether you’re splitting a dinner bill or managing more substantial financial flows. This article delves deep into the question of “how much money can you have on Cash App,” exploring its various limits, the reasons behind them, and how you can optimize your experience for both daily use and larger financial needs.

Navigating Cash App’s Core Limits: Sending and Receiving

Cash App, like all financial tools, operates with specific limits on how much money you can send and receive. These limits are not arbitrary; they are meticulously set to balance user convenience with robust security and compliance protocols. The primary distinction in these limits hinges on whether your account is “unverified” or “verified.”

Unverified Account Restrictions

When you first sign up for Cash App, your account is typically unverified. This initial status comes with relatively restrictive limits, reflecting the platform’s inability to fully confirm your identity. For instance, a common unverified sending limit might be around $250 within any 7-day period, and a receiving limit could be approximately $1,000 over a 30-day period. These low thresholds are in place to deter fraudulent activities and protect both the user and the platform from potential misuse. While these limits might suffice for sporadic, small transactions, they quickly become an impediment for users who rely on Cash App for more regular or larger financial exchanges. This initial phase serves as a trial, allowing users to experience the app while encouraging them to take the necessary steps to unlock its full potential.

The Benefits of Verification: Expanded Horizons

The true power of Cash App, especially for those who wish to use it as a primary financial tool, lies in verifying your account. Verification significantly expands your transaction capabilities, removing many of the constraints associated with an unverified status. Once verified, the sending limit typically jumps to $7,500 per week, and the receiving limit becomes effectively unlimited. This dramatic increase transforms Cash App from a casual payment tool into a powerful personal finance instrument capable of handling a much broader range of transactions, from paying rent to managing business-related payments. Beyond increased limits, verification also unlocks access to other features, such as the ability to order a Cash Card, invest in stocks, and buy/sell Bitcoin, fundamentally enhancing the utility and flexibility of your account.

Key Verification Steps

The process of verifying your Cash App account is straightforward and designed to comply with “Know Your Customer” (KYC) regulations, which are standard in the financial industry. To verify your account, Cash App will typically request the following information:

- Full Legal Name: As it appears on government-issued identification.

- Date of Birth: To confirm you meet the age requirement (usually 18+).

- Last Four Digits of Your Social Security Number (SSN): This is a critical piece of information used for identity confirmation and regulatory reporting.

- Residential Address: To link your account to a physical location.

Providing this information allows Cash App to verify your identity through third-party databases, thereby building trust and compliance. Once verified, your account is upgraded, granting you access to higher limits and a more comprehensive suite of Cash App features. It’s a one-time process that pays significant dividends in terms of financial flexibility.

Beyond Basic Transactions: Limits on Specific Features

Cash App is more than just a peer-to-peer payment service; it has evolved into a multi-faceted financial platform offering various tools. Each of these specialized features comes with its own set of limits, which users need to understand to manage their finances effectively.

Cash Card Spending and ATM Withdrawals

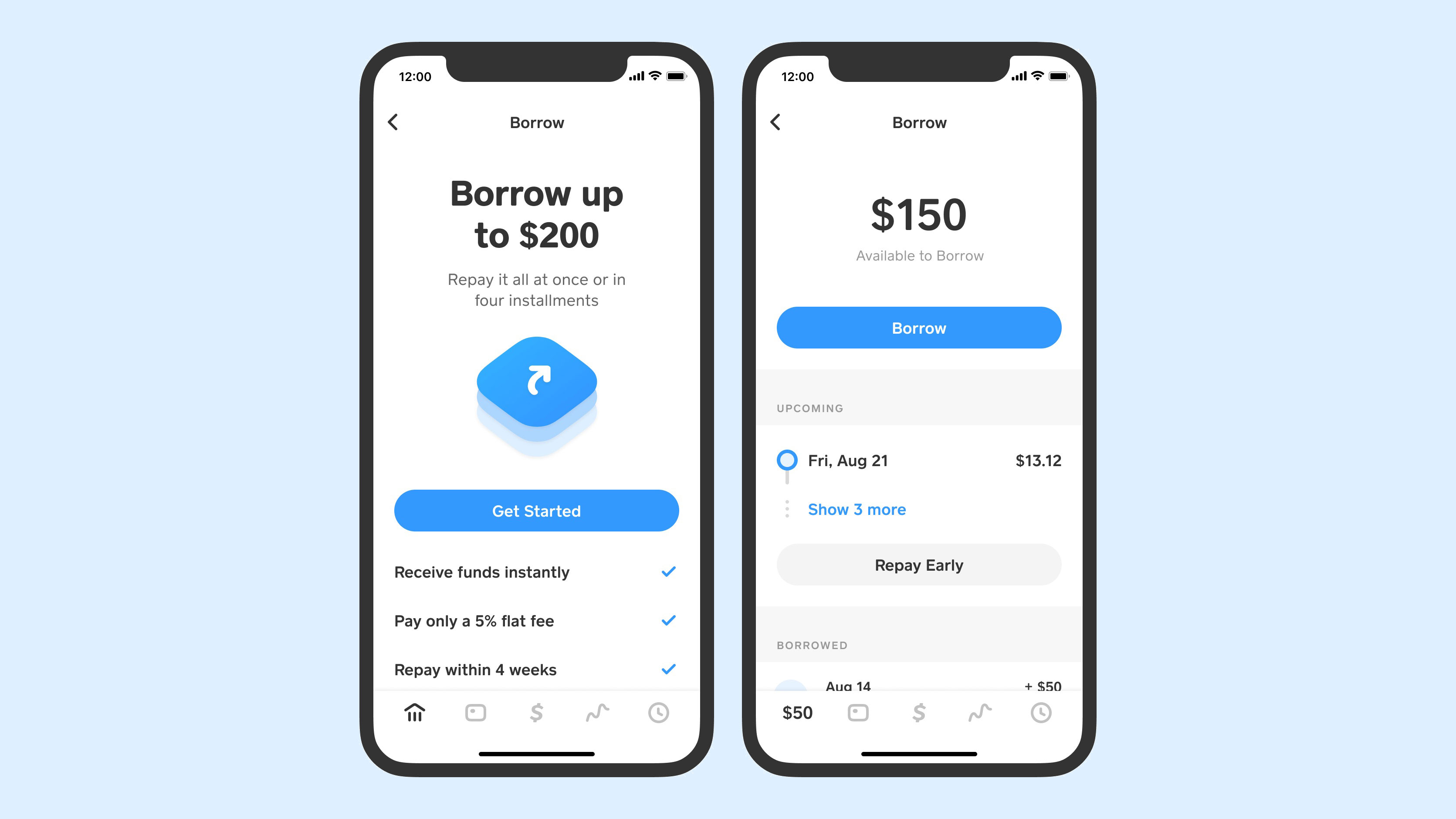

The Cash Card, a customizable debit card linked to your Cash App balance, offers a convenient way to spend money directly from your account. While a verified account allows for significant spending, there are still daily, weekly, and monthly limits associated with its use. Typically, the daily spending limit for the Cash Card can be around $7,000, with a weekly limit often reaching $10,000 and a monthly limit sometimes extending to $25,000. These limits are generous for most daily expenditures but are in place to prevent large-scale fraud should a card be compromised.

Similarly, the Cash Card allows for ATM withdrawals, providing access to physical cash. However, ATM withdrawals usually have much tighter limits. A common daily ATM withdrawal limit might be $1,000, and a weekly limit could be around $2,500. These lower limits are standard across the banking industry for ATM transactions, acting as a safeguard against theft and illicit cash movements. Understanding these limits is crucial for planning cash access, especially when traveling or making large purchases that require physical currency.

Understanding Bitcoin Purchase and Sale Limits

For users interested in the cryptocurrency market, Cash App offers an integrated platform to buy and sell Bitcoin. This feature has its own distinct limits, separate from general sending and receiving. Typically, a verified Cash App account might allow you to buy up to $100,000 worth of Bitcoin per week. Selling limits are often similar or even higher, sometimes allowing for hundreds of thousands of dollars in Bitcoin sales weekly. These limits are set considering market volatility, regulatory oversight of cryptocurrency transactions, and the need to prevent money laundering. While these limits are quite high for the average user, serious crypto traders might find them a consideration. It’s important to remember that these limits apply specifically to Bitcoin transactions and don’t affect your ability to send or receive traditional currency.

Stock Investing Thresholds

Cash App also provides a simplified way to invest in stocks and Exchange Traded Funds (ETFs) directly from the app. This feature aims to democratize investing, making it accessible to a broader audience. Like other features, stock investing comes with its own transaction limits. Users are typically allowed to invest a certain amount daily and weekly. For example, a common daily stock purchase limit might be around $25,000, with a weekly limit of $50,000. These limits are designed to align with regulatory requirements for brokerage services and to protect users from making overly impulsive or risky large investments without proper financial planning. While Cash App’s investing platform is user-friendly, it’s essential to understand that these limits apply to your investment activities, distinct from your regular cash transfers.

The Rationale Behind Cash App’s Financial Ceilings

The existence of financial limits across Cash App’s various services is not an arbitrary design choice; it’s a foundational element of responsible financial management in the digital age. These ceilings serve multiple critical purposes, safeguarding users, ensuring platform integrity, and complying with a complex web of financial regulations.

Safeguarding Against Fraud and Illicit Activities

One of the primary reasons for transaction limits is to mitigate the risk of fraud and other illicit activities. In an age where digital scams are rampant, imposing limits on how much money can be moved through an account acts as a crucial barrier. If an account is compromised, limits can restrict the amount of money a fraudster can steal or siphon off. Similarly, these limits make it more difficult for criminals to use the platform for money laundering, where large sums of illegally obtained money are moved through various accounts to disguise their origin. By restricting the volume and velocity of funds, Cash App adds a layer of defense against sophisticated financial crimes, protecting its users and maintaining the trust placed in its service.

Adhering to Regulatory Compliance (AML/KYC)

Financial institutions worldwide are subject to stringent regulations aimed at preventing financial crime. Two of the most significant are Anti-Money Laundering (AML) and Know Your Customer (KYC) laws. AML regulations require financial services to monitor transactions for suspicious patterns that might indicate money laundering or terrorist financing. KYC rules mandate that these institutions verify the identity of their customers. Transaction limits are a direct output of these requirements. By setting thresholds for unverified accounts and requiring personal information for verification, Cash App ensures it can trace the origin and destination of funds, report suspicious activity, and comply with government mandates. Without these limits and verification processes, Cash App would be unable to operate legally in many jurisdictions, making compliance a non-negotiable aspect of its service.

Mitigating Operational Risk

Beyond external threats, limits also help Cash App manage its own operational risks. Handling vast sums of money carries inherent risks, including technical glitches, system outages, or disputes between users. By controlling the maximum amount of money flowing through the system at any given time, Cash App can better manage its infrastructure, process transactions efficiently, and minimize potential losses from unforeseen operational issues. This risk management approach ensures the stability and reliability of the platform, allowing Cash App to provide consistent service to millions of users. The careful calibration of these limits reflects a balancing act between offering a highly functional service and maintaining financial prudence.

Strategies for Managing Larger Sums and Transactions

While Cash App’s limits are designed with good reason, they can sometimes pose challenges for users needing to handle larger financial transactions. Fortunately, with a verified account and some strategic planning, it’s possible to navigate these limits effectively or know when to seek alternative solutions.

Optimizing Verified Account Capabilities

For most users, simply verifying their Cash App account is the most impactful step toward managing larger sums. The significantly increased sending and receiving limits for verified accounts ($7,500 weekly for sending, virtually unlimited for receiving) accommodate a vast majority of personal and even small business financial needs. If you need to send an amount exceeding your weekly limit, you might consider splitting the transaction over two weeks. For receiving large amounts, the “unlimited” capacity means you generally won’t encounter issues, provided the source of funds is legitimate and compliant with Cash App’s terms of service. Regularly monitoring your transaction history and remaining aware of your weekly limits can help you plan your financial activities more efficiently, ensuring you don’t hit a ceiling unexpectedly.

When to Consider Alternative Financial Solutions

Despite the generous limits for verified accounts, there might be instances where Cash App is not the ideal tool for extremely large transactions. For example, if you frequently need to transfer tens of thousands of dollars, or even hundreds of thousands, Cash App’s daily/weekly limits on specific features like Bitcoin or stock investing, or even its general sending limits, might become restrictive. In such cases, it’s often more practical and secure to leverage traditional banking services. Wire transfers through a bank or credit union are designed for large-value, one-time transactions, offering higher limits, more robust legal protections, and typically clearer audit trails. For business finance, dedicated business banking accounts, commercial payment platforms, or payroll services are specifically designed to handle high volumes and large sums, often with specialized features for accounting and compliance that Cash App does not offer. Understanding the strengths and limitations of each financial tool is key to making informed decisions.

Best Practices for Secure and Efficient Transfers

Regardless of the transaction size, adopting best practices for secure and efficient transfers is paramount. Always double-check recipient details (Cash App $Cashtag, phone number, or email) before confirming any payment to avoid sending money to the wrong person, as Cash App payments are often irreversible. For larger transactions, communicate clearly with the recipient about the payment method and expected timeline. Keep your Cash App account secure with a strong, unique password, two-factor authentication, and regular monitoring of your activity. If you anticipate receiving a very large sum, inform Cash App support in advance if possible, to avoid any flags or temporary holds that might arise from an unusually large incoming transaction. By being proactive and security-conscious, you can ensure a smoother and more reliable experience with all your Cash App transactions.

Maximizing Your Cash App Experience Responsibly

Cash App is an incredibly versatile financial tool, offering convenience and accessibility that traditional banking often lacks. However, to truly maximize its potential and ensure a seamless financial experience, it’s imperative to use the platform responsibly and remain informed.

Regular Monitoring and Security Awareness

Active vigilance is a cornerstone of digital financial security. Regularly logging into your Cash App account to review transaction history can help you spot any unauthorized activity immediately. Enable notifications for all transactions, so you’re instantly aware of money coming in or going out. Implement strong security measures, such as a robust, unique password, a PIN or fingerprint lock for the app, and two-factor authentication (2FA) wherever possible. Be wary of phishing attempts and scams; Cash App will never ask for your PIN or full SSN via email or text message. Understanding common scam tactics, like requests for money to “verify” your account or offers that seem too good to be true, can save you from financial loss. Your proactive approach to security is the first line of defense against potential threats.

Staying Informed About Policy Changes

The financial technology landscape is dynamic, with regulations and company policies evolving continuously. Cash App regularly updates its terms of service, privacy policy, and even its transaction limits. These changes can be driven by new regulatory requirements, market conditions, or enhancements to the platform’s features. It is a user’s responsibility to stay informed about these updates. Cash App typically communicates significant changes through in-app notifications, email, or updates to its official support pages. Making it a habit to review these communications ensures that you are always operating within the current guidelines and can adapt your financial management strategies accordingly. Staying informed helps prevent unexpected issues and allows you to fully leverage any new features or relaxed limits that may be introduced.

In conclusion, Cash App offers a robust platform for managing a significant portion of your personal finances, especially once your account is verified. While limits exist for sending, receiving, using the Cash Card, and engaging with features like Bitcoin and stock investing, these are designed to enhance security, ensure compliance, and manage risk. By understanding these limits, verifying your account, adopting sound security practices, and staying informed, you can harness the full power of Cash App to streamline your financial life efficiently and responsibly. For transactions exceeding even its generous verified limits, traditional banking services remain a reliable alternative, ensuring you always have the right tool for your specific financial needs.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.