Navigating the landscape of insurance can often feel like deciphering a complex financial puzzle. Among the myriad of terms and policy options, “full cover insurance” stands out as a highly sought-after, yet frequently misunderstood, concept. For many, it represents the ultimate peace of mind, suggesting comprehensive protection against a wide array of potential risks. However, the exact meaning of “full cover” can vary significantly depending on the type of insurance—be it automotive, home, travel, or even health—and, more importantly, its cost is far from a fixed figure. This article aims to demystify “full cover insurance,” breaking down what it typically entails, the primary factors that influence its price, and strategies for both understanding and potentially reducing your premiums, all within the critical realm of personal finance.

For most individuals, “full cover insurance” is synonymous with maximum protection, particularly in the context of car insurance. It generally implies a policy that covers not only damages or injuries you might cause to others but also damages to your own property, regardless of fault. While this sounds straightforward, the specifics of what’s included, and more importantly, what’s not, can significantly impact the financial implications. Understanding these nuances is the first step toward making informed decisions that align with your financial health and risk tolerance. This guide will delve into the intricacies of insurance pricing, equipping you with the knowledge to better manage your budget and secure adequate protection without overpaying.

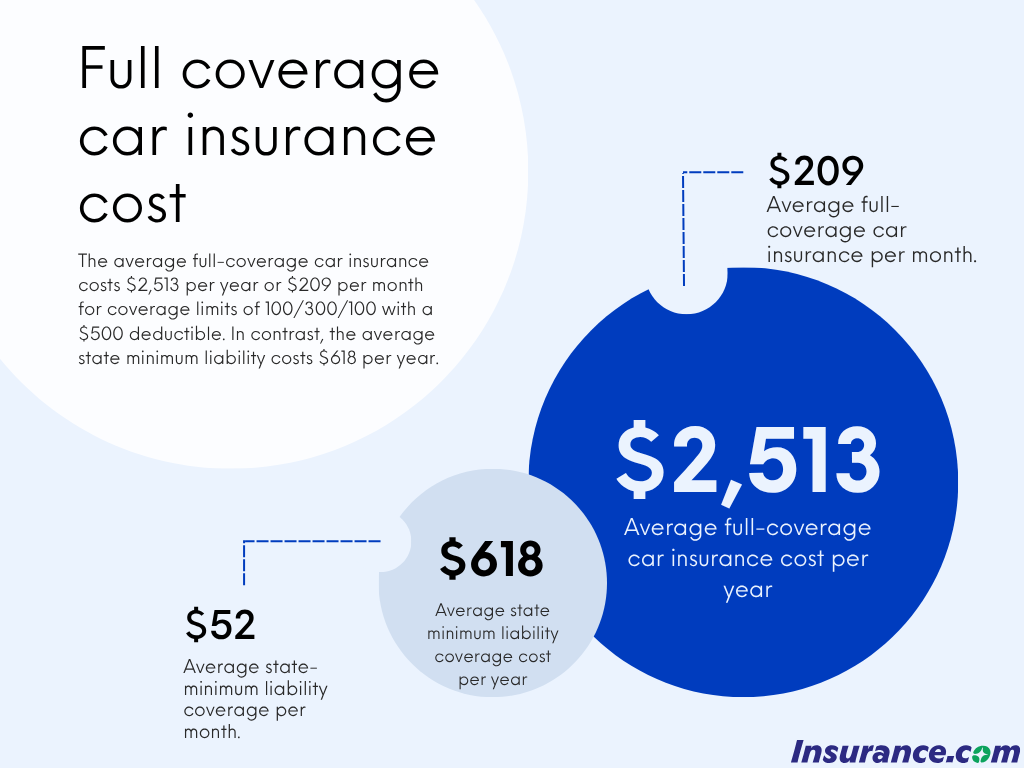

Deciphering “Full Cover” Insurance: What It Really Means

The term “full cover” is often used colloquially and can be a source of confusion because it doesn’t represent a single, universally defined insurance product. Instead, it’s a blanket term consumers use to describe what they perceive as robust, comprehensive protection. In reality, “full cover” is typically an amalgamation of several distinct types of coverage, each addressing different financial risks. Understanding these components is crucial, as they directly contribute to the overall premium.

Common Components of “Full Cover”

When discussing “full cover,” especially in the context of auto insurance (which is where the term is most frequently applied), it generally refers to a combination of several key policy types that go beyond the legally mandated minimums.

Liability Coverage

This is the foundational component of nearly all insurance policies and is often legally required. Liability coverage protects you financially if you are at fault in an accident, covering:

- Bodily Injury Liability: Pays for medical expenses, lost wages, and pain and suffering for others involved in an accident where you are at fault.

- Property Damage Liability: Covers the cost of repairs or replacement of property (like another vehicle or building) that you damage in an accident.

While basic liability is mandatory, “full cover” policies typically recommend or include higher liability limits to provide more robust financial protection against significant claims, which can easily exceed minimum state requirements.

Collision Coverage

This is a critical component that distinguishes “full cover” from basic liability. Collision coverage pays for damage to your own vehicle resulting from a collision with another vehicle or object, regardless of who is at fault. This includes hitting a tree, another car, or even a pothole that causes significant damage. Without collision coverage, you would be solely responsible for the repair or replacement costs of your own car in an at-fault accident.

Comprehensive Coverage

Often paired with collision coverage, comprehensive coverage protects your vehicle from non-collision-related incidents. This includes damage from:

- Theft or vandalism

- Fire

- Falling objects (like tree branches)

- Natural disasters (hail, floods, earthquakes)

- Animal collisions

This coverage is essential for protecting your investment in your vehicle from a wide range of unpredictable events that are outside of your control and not related to driving incidents.

Additional Coverages for Enhanced Protection

Beyond the core trio of liability, collision, and comprehensive, a truly “full cover” policy might also include:

- Uninsured/Underinsured Motorist (UM/UIM) Coverage: Protects you if you’re involved in an accident with a driver who has no insurance or insufficient insurance to cover your damages and medical bills.

- Medical Payments (MedPay) or Personal Injury Protection (PIP): These cover medical expenses for you and your passengers, regardless of who is at fault. PIP can also cover lost wages and essential services.

- Rental Car Reimbursement: Covers the cost of a rental car while your vehicle is being repaired after a covered incident.

- Roadside Assistance: Provides help for breakdowns, flat tires, dead batteries, or lockouts.

These additional coverages enhance the “fullness” of your protection, providing peace of mind for common inconveniences and unexpected events.

The Limits of “Full Cover”

It’s important to remember that even a “full cover” policy isn’t limitless. Every policy has specific coverage limits (the maximum amount the insurer will pay for a claim) and deductibles (the amount you must pay out-of-pocket before your insurance kicks in). Moreover, certain perils might be excluded, such as wear and tear, mechanical breakdowns, or intentionally caused damage. Always review the policy documents carefully to understand the exact scope of your coverage and any exclusions.

Key Factors Influencing Full Cover Insurance Costs

The question “how much is full cover insurance” doesn’t have a single answer because premiums are highly personalized. Insurers use sophisticated algorithms to assess risk, taking into account a multitude of variables. Understanding these factors can empower you to anticipate costs and identify areas for potential savings.

Driver-Specific Variables

Your personal profile as a driver is perhaps the most significant determinant of your insurance rates.

Age and Driving Experience

Statistically, younger, less experienced drivers (especially those under 25) pose a higher risk due to a greater likelihood of accidents. As drivers gain more experience and demonstrate a clean driving record over time, their premiums tend to decrease.

Driving Record

A clean driving record—free of accidents, moving violations (speeding tickets, DUIs), and traffic infractions—is paramount for lower rates. Conversely, a history of claims or violations will invariably lead to higher premiums. Insurers view these as indicators of future risk.

Location

Where you live and park your vehicle significantly impacts your rates. Urban areas with higher traffic density, greater rates of theft and vandalism, or a higher incidence of accidents typically have higher premiums than rural areas. Even specific zip codes within a city can have different rates due to varying crime rates or accident statistics.

Credit Score (in many states)

In many U.S. states, insurers use a credit-based insurance score to help predict the likelihood of future claims. Individuals with higher credit scores are often perceived as more responsible and thus lower risk, leading to lower premiums. However, some states prohibit the use of credit scores in determining insurance rates.

Marital Status and Gender

Married individuals often pay less for insurance than single individuals, as they are statistically less likely to be involved in accidents. Gender can also play a role, though its impact has lessened and is even prohibited as a rating factor in some regions due to anti-discrimination laws.

Vehicle-Specific Variables

The type of vehicle you drive also plays a substantial role in your full cover insurance costs.

Make, Model, and Year

Newer, more expensive vehicles generally cost more to insure due to higher repair or replacement costs. Luxury cars, sports cars, and high-performance vehicles typically command higher premiums. Certain models are also statistically more likely to be stolen or involved in accidents, affecting rates.

Safety Features

Vehicles equipped with advanced safety features (e.g., anti-lock brakes, airbags, electronic stability control, lane departure warning, automatic emergency braking) can sometimes qualify for discounts because they reduce the likelihood or severity of accidents.

Anti-Theft Devices

Cars with factory-installed or aftermarket anti-theft systems (e.g., alarms, immobilizers, tracking devices) are less likely to be stolen, which can lead to lower comprehensive coverage premiums.

Repair and Parts Cost

The cost and availability of replacement parts for your specific vehicle model can influence rates. Cars with expensive or rare parts, or those that require specialized labor for repairs, will generally have higher collision and comprehensive premiums.

Policy-Specific Variables

The choices you make when configuring your insurance policy directly impact the final premium.

Deductible Amount

Your deductible is the out-of-pocket amount you agree to pay before your insurance coverage kicks in for collision and comprehensive claims. A higher deductible typically results in lower premiums, as you’re taking on more of the initial financial risk. Conversely, a lower deductible means higher premiums.

Coverage Limits

The maximum amount your insurer will pay for a covered loss. Opting for higher liability limits, for example, provides greater financial protection but also increases your premium. Balancing adequate protection with affordability is key.

Discounts Applied

Insurers offer a wide range of discounts, such as multi-policy discounts (bundling auto and home insurance), good student discounts, safe driver discounts, loyalty discounts, professional affiliation discounts, and payment method discounts (e.g., paying in full or setting up automatic payments). Maximizing these can significantly reduce your premium.

Insurance Company

Different insurance companies have varying risk assessment models, overhead costs, and target demographics. This means the exact same “full cover” policy can have vastly different prices across different providers. Shopping around is therefore essential.

Strategies for Finding Affordable Full Cover Insurance

While the cost of full cover insurance can seem daunting, there are actionable steps you can take to find the most affordable rates without compromising essential protection. A proactive approach to managing your insurance portfolio can yield significant financial benefits.

Smart Shopping and Comparison

The single most effective strategy for finding competitive rates is to shop around diligently.

Gather Multiple Quotes

Never settle for the first quote you receive. Obtain quotes from at least three to five different insurance providers. Use online comparison tools, independent insurance agents, and direct insurers to cast a wide net. Each company uses its own underwriting criteria, leading to potentially significant price disparities for the same level of coverage.

Understand Quote Details

When comparing quotes, ensure you are comparing “apples to apples.” Verify that the coverage limits, deductibles, and included coverages are identical across all quotes. A seemingly cheaper policy might just have lower limits or exclude essential protections.

Work with an Independent Agent

An independent insurance agent works with multiple carriers and can help you compare policies and find the best fit for your needs and budget. They can also explain complex policy terms and identify potential gaps in coverage.

Optimizing Your Policy and Driving Habits

Beyond shopping around, several adjustments to your policy or lifestyle can lead to lower premiums.

Increase Your Deductibles (When Prudent)

If you have a robust emergency fund, consider increasing your collision and comprehensive deductibles. While this means higher out-of-pocket costs in the event of a claim, it can substantially lower your monthly or annual premiums. Ensure you can comfortably afford the deductible amount before committing.

Bundle Policies

Many insurers offer discounts if you purchase multiple policies (e.g., auto, home, renters, life insurance) from them. This “multi-policy discount” can lead to significant savings across all your insurance products.

Drive Safely and Maintain a Clean Record

This is perhaps the most fundamental and impactful long-term strategy. Avoiding accidents and traffic violations is the best way to keep your premiums low. Many insurers offer good driver or safe driver discounts for those with clean records over several years. Some even use telematics devices or apps to monitor driving habits and offer discounts for safe driving.

Utilize Available Discounts

Proactively ask about all available discounts. Common discounts include:

- Good Student Discount: For students maintaining a certain GPA.

- Defensive Driving Course Discount: For completing an approved safety course.

- Low Mileage Discount: If you drive fewer miles than average annually.

- Anti-Theft Device Discount: For vehicles equipped with approved security systems.

- Payment Discounts: For paying premiums in full or signing up for automatic payments.

- Loyalty Discounts: For remaining with the same insurer for an extended period.

Consider Your Vehicle Choice

When purchasing a new car, research its insurance costs before buying. Some vehicles are inherently more expensive to insure due to their cost, performance, theft rates, or repair expenses. Opting for a model known for its safety and affordability to repair can save you money on insurance over the long run.

Regular Review and Adjustment

Insurance needs change over time, and your policy should evolve with them.

Review Your Policy Annually

Circumstances change: you might pay off your car loan, move to a new area, get married, or your driving habits might shift. Annually review your policy with your agent or insurer to ensure your coverage is still appropriate and you’re not overpaying for coverage you no longer need. For instance, if your car is old and its market value has significantly depreciated, you might consider dropping collision and comprehensive coverage, as the cost of these coverages might outweigh the potential payout.

Inform Your Insurer of Life Changes

Marriage, moving, a new job with a shorter commute, or adding safety features to your vehicle are all life events that could qualify you for lower rates or new discounts. Keep your insurer informed to ensure your policy accurately reflects your current situation.

Maintain a Good Credit Score

As mentioned, a strong credit score can positively influence your insurance premiums in many states. Practicing good financial habits, such as paying bills on time and managing debt responsibly, can indirectly lead to lower insurance costs.

The Value Proposition: Is Full Cover Insurance Worth the Cost?

Deciding whether full cover insurance is “worth it” is a personal financial decision that hinges on your individual circumstances, risk tolerance, and financial capacity. While it undeniably comes with a higher premium compared to basic liability, the peace of mind and financial protection it offers can be invaluable.

Protecting Your Assets and Future Financial Stability

For most people, a car is a significant investment, often second only to a home. Full cover insurance protects that investment. Without collision and comprehensive coverage, a single accident or incident could result in thousands of dollars in out-of-pocket repair costs or the complete loss of your vehicle’s value, potentially crippling your finances. This is particularly true if you have a car loan, as lenders typically require full cover insurance to protect their interest in the vehicle.

Beyond your vehicle, robust liability coverage within a full cover policy protects your personal assets. If you are found at fault in a major accident resulting in severe injuries or significant property damage, legal judgments can easily exceed basic liability limits. The excess could then be sought from your personal savings, investments, or even future earnings. Higher liability limits offer a crucial buffer against such catastrophic financial ruin.

Peace of Mind and Reduced Stress

The psychological benefit of knowing you are adequately protected against unforeseen circumstances cannot be overstated. Accidents and incidents are stressful enough without the added burden of worrying about how you will pay for repairs, medical bills, or legal fees. Full cover insurance, particularly for significant assets like vehicles, mitigates this financial anxiety, allowing you to focus on recovery rather than fiscal repercussions.

Weighing Cost Against Risk

The key to determining if full cover is “worth it” lies in a careful evaluation of the cost versus the potential risk. Consider:

- Your vehicle’s value: The newer and more valuable your car, the more important collision and comprehensive coverage become.

- Your financial situation: Do you have an emergency fund sufficient to cover significant vehicle damage or potential liability claims out-of-pocket?

- Your driving environment: Do you drive frequently in high-traffic areas, or areas prone to theft or severe weather?

- Your risk tolerance: Are you comfortable with the possibility of a substantial financial loss if an accident occurs and you only have minimal coverage?

For many, the slightly higher premium for full cover insurance is a small price to pay for the extensive financial security and peace of mind it provides. It acts as a critical safety net, safeguarding your assets and ensuring that an unfortunate incident doesn’t derail your long-term financial goals. By diligently comparing quotes, leveraging discounts, and regularly reviewing your policy, you can secure robust protection at the most competitive price, making full cover insurance a truly valuable investment in your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.