Understanding the relentless march of inflation is not merely an academic exercise for economists; it is a vital skill for anyone managing personal finances, investing, or running a business. Inflation, the rate at which the general level of prices for goods and services is rising, and subsequently, purchasing power is falling, directly impacts our financial well-being. Without a clear grasp of how to measure it, we are often left reacting to its effects rather than proactively planning for them.

One of the most robust and widely accepted tools for measuring inflation is the Consumer Price Index (CPI). Developed and maintained by governmental statistical agencies, the CPI provides a snapshot of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services. By learning to calculate the inflation rate using CPI data, individuals and businesses can gain critical insights into the real value of their money, enabling more informed decisions regarding saving, investing, budgeting, and even salary negotiations. This article will demystify the CPI and equip you with the knowledge to accurately calculate and interpret the rate of inflation, empowering you to navigate the economic landscape with greater confidence.

Understanding Inflation and Its Impact on Your Finances

Before diving into calculations, it’s crucial to solidify our understanding of what inflation truly is and why its measurement is paramount for financial stability and growth. Inflation isn’t just about rising prices; it’s about the erosion of your money’s purchasing power over time.

What is Inflation?

At its core, inflation represents the sustained increase in the general price level of goods and services in an economy over a period. When prices rise, each unit of currency buys fewer goods and services than it could previously. Consequently, inflation reflects a reduction in the purchasing power per unit of money – a dollar today buys less than a dollar yesterday. This phenomenon can be driven by various factors, including demand-pull (too much money chasing too few goods), cost-push (rising production costs), and built-in inflation (inflationary expectations leading to wage-price spirals). While moderate inflation is often considered a sign of a healthy, growing economy, high or hyperinflation can be incredibly destructive, destabilizing markets and eroding savings.

Why Inflation Matters for Your Money

The implications of inflation permeate every facet of your financial life. For personal finance, it means your savings accounts, if not earning interest rates above inflation, are effectively losing value in real terms. Retirement funds planned decades ago may fall short of their purchasing power targets if inflation is underestimated. For investors, inflation dictates the real return on investments; a 5% nominal return is far less impressive if inflation is running at 4%. Businesses face rising costs for raw materials, labor, and energy, which can squeeze profit margins and necessitate price adjustments.

Moreover, inflation can disproportionately affect different segments of the population. Those on fixed incomes or with significant cash savings are often hit hardest, while those with assets that appreciate with inflation (like real estate or certain commodities) may fare better. Understanding how to quantify inflation is the first step in formulating strategies to protect and grow your wealth in an ever-changing economic environment.

Demystifying the Consumer Price Index (CPI)

The Consumer Price Index (CPI) is the most commonly used metric to track inflation and is foundational to our calculation. Developed and published by government agencies such as the Bureau of Labor Statistics (BLS) in the United States, it provides a standardized way to measure changes in the cost of living.

What is the CPI?

The CPI measures the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services. This “market basket” is a theoretical collection of items that represents what typical households buy. It includes a wide range of categories, such as food and beverages, housing, apparel, transportation, medical care, recreation, education and communication, and other goods and services. The CPI is often expressed as an index number, with a base period assigned a value (e.g., 100). Subsequent periods’ index numbers reflect the percentage change relative to this base. For instance, if the CPI in a later period is 110, it implies that prices have risen by 10% since the base period.

How the CPI is Constructed and Measured

The construction of the CPI is a meticulous process involving several key steps. First, statistical agencies conduct surveys to determine what goods and services urban households purchase and in what proportions. This forms the basis of the “market basket” and assigns weights to different categories. Housing, for example, typically carries a much heavier weight than apparel due to its larger share of consumer spending.

Second, prices for these thousands of goods and services are collected monthly from a sample of retail stores and service establishments across various geographical areas. These prices are then averaged and combined using the assigned weights to produce a single CPI value for a given month or period. The process is continually updated to account for changes in consumer spending patterns, product quality, and the introduction of new goods and services, ensuring the index remains relevant and reflective of current economic realities.

Limitations and Nuances of CPI

While the CPI is an invaluable tool, it’s essential to acknowledge its limitations. It measures inflation for “urban consumers,” which might not perfectly reflect the spending patterns of rural populations or specific demographic groups. The “market basket” is a generalized average and may not align perfectly with an individual’s specific spending habits. For example, someone who primarily eats at home might experience a different personal inflation rate than someone who dines out frequently.

Furthermore, the CPI can sometimes struggle to accurately capture changes in product quality or the introduction of new technologies. A new smartphone might cost more than its predecessor, but it also offers significantly improved features, making a direct price comparison difficult. Statisticians attempt to adjust for these “hedonic quality adjustments,” but it remains a complex area. Despite these nuances, the CPI remains the most robust and widely accepted standard for measuring broad inflation trends.

The Step-by-Step Guide to Calculating Inflation Using CPI

With a solid understanding of inflation and the CPI, we can now proceed to the practical calculation. The formula is straightforward, but its accurate application requires careful attention to data.

Gathering the Necessary Data

To calculate the inflation rate, you will need two CPI values:

- CPI (Current Period): The Consumer Price Index for the most recent period you are interested in (e.g., the current month, quarter, or year).

- CPI (Previous Period): The Consumer Price Index for the period immediately preceding your current period (e.g., the previous month, the same month last year, or the previous year).

These CPI values are readily available from the websites of national statistical agencies, such as the Bureau of Labor Statistics (BLS) for the United States, Eurostat for the European Union, or Statistics Canada. For example, you might look for “CPI data by month” or “annual CPI index.”

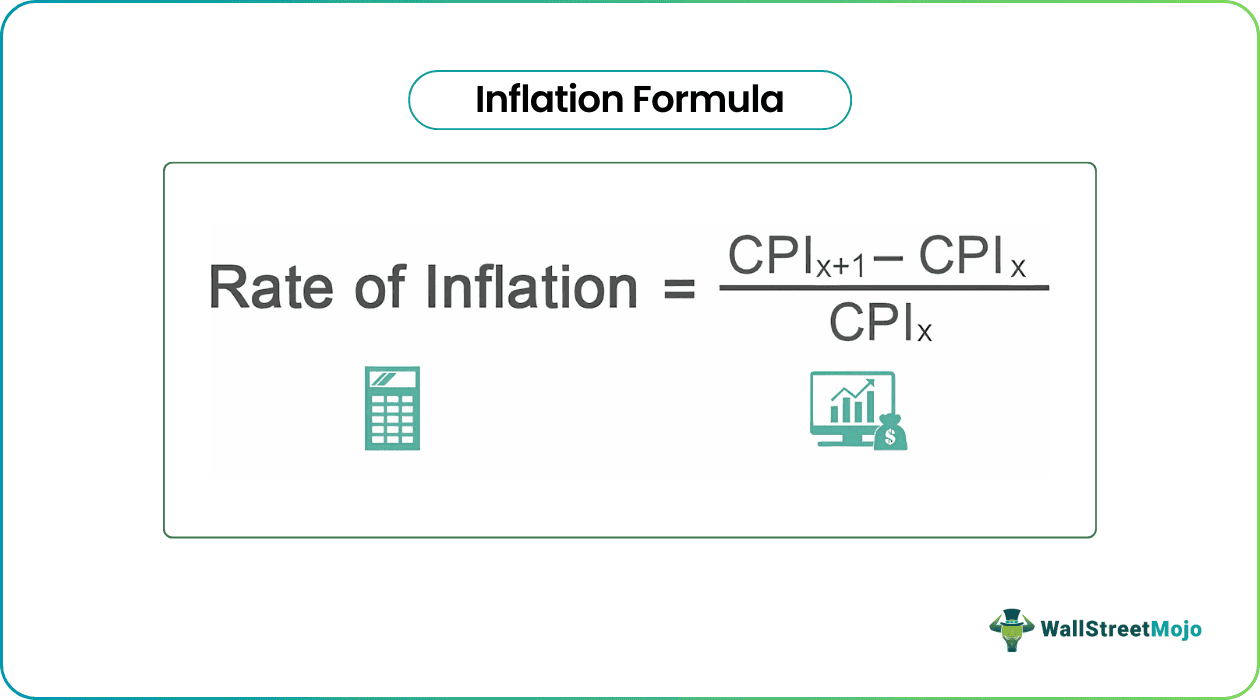

The Inflation Rate Formula

The formula for calculating the inflation rate between two periods using CPI is as follows:

$$ text{Inflation Rate} = frac{(text{CPI in Current Period} – text{CPI in Previous Period})}{text{CPI in Previous Period}} times 100 $$

This formula yields the percentage change in the CPI from the previous period to the current period, which is the inflation rate.

Working Through a Practical Example

Let’s illustrate this with a hypothetical example. Suppose we want to calculate the annual inflation rate between January 2023 and January 2024.

-

Step 1: Obtain CPI Data.

- CPI for January 2024 (Current Period): Let’s assume it is 308.417

- CPI for January 2023 (Previous Period): Let’s assume it is 299.170

-

Step 2: Apply the Formula.

$$ text{Inflation Rate} = frac{(308.417 – 299.170)}{299.170} times 100 $$

$$ text{Inflation Rate} = frac{9.247}{299.170} times 100 $$

$$ text{Inflation Rate} approx 0.03090 times 100 $$

$$ text{Inflation Rate} approx textbf{3.09%} $$

In this example, the annual inflation rate from January 2023 to January 2024 is approximately 3.09%. This means that, on average, the cost of goods and services in the market basket increased by 3.09% over that year, and the purchasing power of a dollar decreased by about 3.09% during the same period.

Interpreting Your Inflation Calculation and Its Financial Implications

Calculating the inflation rate is just the first step. The true value lies in interpreting these numbers and understanding their implications for your financial strategies.

Making Sense of the Numbers

Once you have calculated the inflation rate, compare it to historical averages, current economic forecasts, and your personal financial goals. A 3% inflation rate might seem low, but compounded over decades, it can significantly erode the real value of savings. Understanding whether inflation is accelerating or decelerating is also critical. An increasing inflation rate signals a greater urgency to adjust financial plans, while a decreasing rate (disinflation) might offer some reprieve, though prices are still rising, just at a slower pace. It’s also vital to distinguish between overall CPI inflation and specific price changes for goods and services you consume most, as your personal inflation rate might differ.

Strategies for Mitigating Inflation’s Effects

Armed with your calculated inflation rate, you can implement various strategies to safeguard your financial health:

- Seek Higher-Yielding Investments: Ensure your investments are generating returns that outpace inflation. This might mean exploring stocks, real estate, inflation-protected securities (TIPS), or commodities, rather than relying solely on low-yield savings accounts.

- Budgeting for Rising Costs: Adjust your household budget to account for increased expenses in categories prone to inflation, such as groceries, utilities, and transportation. Proactive budgeting helps prevent being caught off guard.

- Negotiate Wages and Prices: If you are an employee, understanding inflation provides leverage for salary negotiations, ensuring your compensation keeps pace with the cost of living. For business owners, it informs pricing strategies to maintain profit margins.

- Reduce Debt (Strategically): While inflation erodes the real value of fixed-rate debt, it also makes new borrowing more expensive as interest rates tend to rise in response. Prioritizing strategic debt reduction can be beneficial.

Utilizing Inflation Data for Smarter Financial Decisions

The power of knowing how to calculate and interpret inflation using CPI extends far beyond simple understanding; it becomes a critical input for robust financial planning and decision-making.

Budgeting and Cost of Living Adjustments

For personal finance, regular inflation calculations enable you to make realistic cost-of-living adjustments to your budget. If you anticipate a 3% inflation rate next year, you can factor in a 3% increase in your average expenses, ensuring your budget remains solvent and reflects actual purchasing power. This is particularly crucial for fixed expenses that are subject to price increases, such as rent, insurance premiums, and subscription services. Businesses use this data to adjust employee salaries, ensuring fair compensation and retaining talent, and to forecast operational costs more accurately.

Investment Strategies in an Inflationary Environment

For investors, inflation data is a cornerstone of portfolio management. High inflation typically favors certain asset classes over others. Assets that tend to perform well during inflationary periods include:

- Real Estate: Property values and rents often rise with inflation.

- Stocks (selectively): Companies with strong pricing power and low debt can pass on increased costs to consumers.

- Commodities: Raw materials like gold, oil, and agricultural products often serve as inflation hedges.

- Treasury Inflation-Protected Securities (TIPS): These bonds are designed to protect investors from inflation by adjusting their principal value based on changes in the CPI.

Conversely, traditional bonds with fixed interest rates and cash savings tend to lose real value during periods of high inflation. Understanding the CPI and its trends helps investors strategically reallocate assets to protect and grow their real wealth.

Long-Term Financial Planning

From retirement planning to saving for a child’s education, long-term financial goals are highly vulnerable to the silent erosion of inflation. A retirement plan crafted today without accounting for future inflation will likely fall drastically short in purchasing power decades down the line. By projecting future inflation rates (even if imperfectly) using historical CPI data and economic forecasts, individuals can set more realistic savings targets and investment growth expectations. This foresight allows for adjustments in contribution amounts, investment choices, and overall financial strategies to ensure that future financial aspirations remain achievable in real terms.

In conclusion, the ability to calculate and understand the rate of inflation using the Consumer Price Index is more than just a numerical exercise; it’s an indispensable financial literacy skill. It empowers individuals and businesses to transform from passive observers of economic shifts into active participants in shaping their financial destinies. By consistently monitoring CPI data, applying the inflation formula, and strategically adjusting financial plans, you can protect your wealth, optimize your investments, and build a more secure financial future, irrespective of the economic currents.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.