Securing capital is often one of the most critical challenges faced by small business owners. While traditional bank loans exist, many entrepreneurs turn to Small Business Administration (SBA) loans for their favorable terms, lower down payments, and longer repayment periods. These government-backed loans provide a lifeline for businesses that might not qualify for conventional financing. But the process can seem daunting. This guide will demystify the SBA loan application process, providing a clear roadmap for small business owners seeking this vital financial support.

Understanding the SBA Loan Landscape

Before diving into the application, it’s crucial to grasp what an SBA loan entails and why it might be the right fit for your business. These aren’t direct loans from the government; rather, the SBA guarantees a portion of loans made by participating lenders (banks, credit unions, and other financial institutions). This guarantee reduces the risk for lenders, making them more willing to provide financing to small businesses.

What is an SBA Loan?

An SBA loan is a commercial loan issued by a private lender and partially guaranteed by the U.S. Small Business Administration. This federal agency’s primary role is to aid, counsel, assist, and protect the interests of small business concerns. By guaranteeing a percentage of the loan, the SBA encourages lenders to extend credit to small businesses that may otherwise be deemed too risky. This mechanism allows businesses to access capital for various purposes, from starting up and expanding to purchasing equipment or real estate.

Why Consider an SBA Loan?

SBA loans offer several distinct advantages over conventional financing options. Firstly, the government guarantee often translates into more competitive interest rates, which can significantly reduce the overall cost of borrowing over the life of the loan. Secondly, SBA loans typically feature longer repayment terms, sometimes extending up to 10 years for working capital and 25 years for real estate, resulting in lower monthly payments and improved cash flow for the business. Thirdly, they often come with more flexible collateral requirements and lower down payments compared to traditional loans. These benefits make SBA loans an attractive option for startups, growing businesses, and those in industries that might face difficulties securing conventional bank financing.

Key SBA Loan Programs

The SBA offers several programs tailored to different business needs. Understanding the distinctions is vital for selecting the right one:

- SBA 7(a) Loan Program: This is the most common and flexible SBA loan program, suitable for a wide range of purposes, including working capital, equipment purchases, inventory, real estate, and business acquisition. Loan amounts can go up to $5 million.

- SBA 504 Loan Program: Designed for financing fixed assets, such as real estate or machinery and equipment. It typically involves three parties: the borrower, a conventional lender, and a Certified Development Company (CDC) which is a private, non-profit corporation. This program usually offers long-term, fixed-rate financing.

- SBA Microloan Program: Provides smaller loans, up to $50,000, for working capital or the purchase of inventory, supplies, furniture, fixtures, machinery, or equipment. These loans are administered through non-profit community-based lenders with experience in lending and technical assistance.

- SBA Disaster Loans: These are direct loans from the SBA (not guaranteed) provided to businesses and homeowners in declared disaster areas to help them recover from physical damage and economic injury caused by natural disasters.

Essential Eligibility Criteria

Qualifying for an SBA loan isn’t just about having a great business idea; it requires meeting specific criteria set by both the SBA and the participating lender. While the exact requirements can vary slightly between programs and lenders, some fundamental eligibility factors apply across the board.

General Business Requirements

The SBA defines what constitutes a “small business” for its programs, which typically involves limits on revenue and/or employee count, varying by industry. Beyond size, your business must:

- Operate for profit: Non-profits are generally not eligible (except for some disaster assistance).

- Do business in the U.S. or its territories.

- Have reasonable owner equity invested in the business.

- Be unable to obtain credit elsewhere on reasonable terms (this is often a self-certification, but lenders will assess it).

- Not be involved in certain ineligible industries (e.g., speculation, gambling, passive investments, pyramid schemes).

Personal Financial Health

Lenders will scrutinize the personal financial health of the business owner(s), as this significantly impacts the business’s creditworthiness, especially for smaller businesses and startups. Key elements include:

- Credit Score: A strong personal credit score (typically 650 or higher, though some programs or lenders might accept lower with mitigating factors) indicates responsible financial management.

- Debt-to-Income Ratio: Lenders assess your ability to manage existing personal debts in addition to the proposed business loan.

- Personal Guarantees: For most SBA loans, business owners with 20% or more ownership are required to provide a personal guarantee, meaning they are personally liable for the loan if the business defaults.

Industry-Specific Considerations

While many industries are eligible, some face specific scrutiny or are outright excluded. Furthermore, the longevity and stability of your industry can influence a lender’s decision. For instance, a business in a rapidly growing, stable sector might be viewed more favorably than one in a declining or highly volatile market. It’s crucial to check if your industry falls into any prohibited categories or has special requirements.

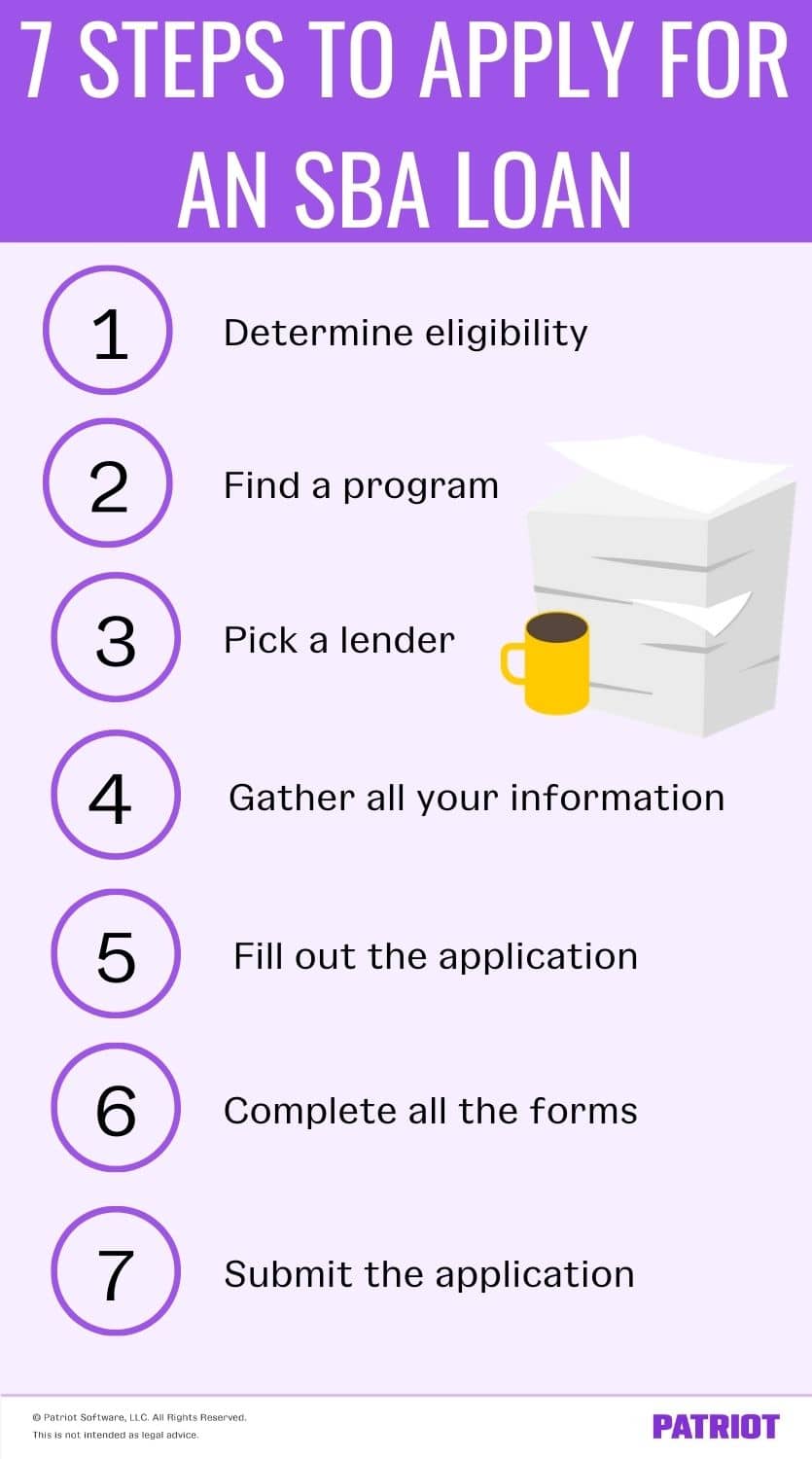

The Step-by-Step Application Process

The SBA loan application process, while detailed, is manageable when approached systematically. Breaking it down into distinct phases can help you organize your efforts and improve your chances of success.

Step 1: Determine Your Needs and Program Type

Before anything else, clearly define why you need the loan and how much capital you require. Are you buying equipment, expanding your premises, or needing working capital? Your specific need will guide you toward the most appropriate SBA loan program (7(a), 504, Microloan, etc.). Research each program thoroughly to understand its terms, limitations, and eligibility.

Step 2: Prepare Your Business Plan and Financials

This is arguably the most critical preparatory step. Lenders want to see a clear vision and a solid financial foundation. You’ll need:

- A Comprehensive Business Plan: Outline your business concept, market analysis, management team, operational plan, and marketing strategy. This should demonstrate viability and how the loan will contribute to growth.

- Detailed Financial Projections: This includes profit and loss statements, cash flow projections, and balance sheets for at least the next 1-3 years. Be realistic and well-supported by your market research.

- Historical Financials: If an existing business, provide at least three years of financial statements (income statements, balance sheets, cash flow statements) and federal tax returns.

- Personal Financial Statement: A summary of your personal assets, liabilities, and net worth.

Step 3: Find an SBA-Approved Lender

The SBA doesn’t lend money directly (except for disaster loans). You need to find a bank, credit union, or other financial institution that participates in SBA loan programs. Many large national banks are active SBA lenders, but smaller regional and community banks often have dedicated SBA departments and may offer more personalized service. The SBA website provides a “Lender Match” tool that can help connect you with potential lenders. It’s advisable to speak with multiple lenders to compare terms and find the best fit.

Step 4: Submit Your Application

Once you’ve chosen a lender and gathered all required documentation, you’ll submit your formal application. The lender will provide their specific application forms, which will include questions about your business, its owners, and the loan’s purpose. Ensure all forms are filled out accurately and completely, and that all supporting documents are attached and clearly labeled. This is where your meticulous preparation pays off.

Step 5: Underwriting and Approval

After submission, the lender’s underwriting team will thoroughly review your application, business plan, financial statements, credit history (both business and personal), and collateral. They will assess the risk, your repayment capacity, and whether your business meets both their internal lending criteria and the SBA’s requirements. This process can take several weeks or even months, depending on the loan type and the complexity of your application. If approved, you’ll receive a commitment letter outlining the terms and conditions of the loan.

Critical Documentation for a Strong Application

A well-organized and complete set of documents is paramount for a smooth SBA loan application. Missing or incomplete information is a common reason for delays or rejections.

Business Information & Legal Documents

- Business License & Registrations: Proof of legal operation.

- Business Lease/Deed: If renting or owning property.

- Articles of Incorporation/Organization: Shows legal structure (sole proprietorship, partnership, LLC, corporation).

- Employer Identification Number (EIN): Federal tax ID.

- Business Bank Statements: Recent statements, typically 12 months.

- Resumes of Key Management: Demonstrating experience and expertise.

- Business Plan: As detailed in Step 2.

- Franchise Agreement: If applicable.

Comprehensive Financial Statements

- Federal Tax Returns: Business and personal, typically for the last three years.

- Profit & Loss (Income) Statements: Year-end for the last three years, plus a current interim statement.

- Balance Sheets: Year-end for the last three years, plus a current interim statement.

- Cash Flow Statements: Showing how money moves in and out of your business.

- Accounts Receivable and Payable Aging Reports: Current lists of who owes you money and who you owe.

- Debt Schedule: A list of all existing business debts, including lender, balance, payment, and collateral.

- Pro Forma Financial Statements: Projections for the next 1-3 years.

Personal Financial Details

- Personal Financial Statement: SBA Form 413, detailing personal assets and liabilities.

- Personal Tax Returns: Last three years.

- Personal Credit Report: Lenders will pull this, but it’s good to know your score beforehand.

Supporting Documents

- Loan Request Letter: Briefly explaining the loan purpose and amount.

- Collateral List: A detailed list of assets being offered as collateral.

- Letters of Intent/Purchase Agreements: If using the loan for specific acquisitions (e.g., equipment, real estate, business purchase).

- Environmental Reports: May be required for real estate loans.

Tips for a Successful Application and Beyond

Navigating the SBA loan process can be complex, but strategic preparation and proactive engagement can significantly enhance your chances of approval and set your business up for long-term success.

Be Thorough and Organized

The sheer volume of required documentation means organization is key. Create a digital folder and physical binder for all your documents. Label everything clearly and be ready to provide additional information promptly if requested. Inaccuracies or omissions can lead to significant delays or even outright rejection. Demonstrating your attention to detail reassures lenders about your capability to manage finances.

Build a Relationship with Your Lender

Don’t treat your loan application as a one-off transaction. Engage proactively with your lender. Ask questions, seek clarification, and be responsive to their requests. A good banking relationship can be invaluable, not just for the current loan but for future financing needs and financial advice. Lenders are more likely to support businesses they know and trust.

Understand the Timeline

SBA loan processing times can vary widely, from a few weeks to several months, depending on the program, the lender, the complexity of your business, and the completeness of your application. Don’t wait until the last minute if you have an urgent financing need. Plan ahead and factor in potential delays. Microloans and smaller 7(a) loans might process faster than larger, more complex requests or 504 loans.

What Happens Post-Approval

Once approved, you’ll receive a commitment letter outlining all the terms and conditions. Review this carefully with legal counsel if necessary. After signing, the funds will be disbursed according to the agreed-upon schedule. Remember that the loan is a significant responsibility. Adhere to the repayment schedule, maintain accurate financial records, and continue to execute your business plan. The SBA often requires periodic reporting to ensure compliance with the loan terms. Successful repayment strengthens your business’s credit profile, opening doors for future growth and investment.

Applying for an SBA loan is a significant undertaking, but the benefits—including favorable terms and access to vital capital—make it a worthwhile endeavor for many small businesses. By understanding the programs, meticulously preparing your documentation, and engaging proactively with lenders, you can significantly increase your likelihood of securing the funding your business needs to thrive.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.