Investing in the S&P 500 is often cited as the gold standard for individual investors seeking to build long-term wealth. Comprising approximately 500 of the largest and most influential publicly traded companies in the United States, the Standard & Poor’s 500 Index represents about 80% of the total market capitalization of the U.S. equity market. When you buy an S&P 500 index fund, you are essentially purchasing a small piece of the entire American economy. This strategy, popularized by investment legends like John Bogle and endorsed by Warren Buffett, allows investors to capture the market’s returns with minimal effort, low costs, and high diversification.

Understanding the Foundations of S&P 500 Index Investing

Before executing a trade, it is crucial to understand what you are actually buying. An index fund is a type of mutual fund or exchange-traded fund (ETF) with a portfolio constructed to match or track the components of a financial market index. In this case, the fund seeks to replicate the performance of the S&P 500.

What Makes the S&P 500 Unique?

The S&P 500 is a market-capitalization-weighted index. This means that larger companies, such as Apple, Microsoft, and Amazon, have a greater impact on the index’s performance than smaller companies. Because the index is rebalanced periodically by a committee, it naturally weeds out failing companies and includes rising stars. This “survival of the fittest” mechanism is one reason why the S&P 500 has historically delivered an average annual return of approximately 10% over long periods before inflation.

The Philosophy of Passive Management

The primary advantage of an S&P 500 index fund is its passive nature. Unlike active funds, where a manager attempts to “beat the market” by picking specific stocks, an index fund simply aims to be the market. This leads to significantly lower management fees, known as expense ratios. Research consistently shows that over long horizons, low-cost passive index funds outperform the vast majority of actively managed funds, primarily because of the high fees and inconsistent performance associated with active trading.

A Step-by-Step Guide to Purchasing Your First Fund

Buying an S&P 500 index fund is a straightforward process, but it requires making a few key decisions regarding where to hold your money and which specific investment vehicle to use.

Step 1: Open a Brokerage Account

To buy an index fund, you need a gateway to the financial markets. Most investors use online brokerages. When choosing a broker, look for firms that offer commission-free trades on ETFs and have no monthly account maintenance fees. Major providers like Vanguard, Fidelity, Charles Schwab, and Vanguard are industry leaders known for their robust platforms and low-cost offerings.

You will also need to decide on the account type. If you are investing for retirement, a tax-advantaged account like a Roth IRA or a Traditional IRA is often the best choice due to the tax benefits. For general wealth building with no withdrawal restrictions, a standard taxable brokerage account is appropriate.

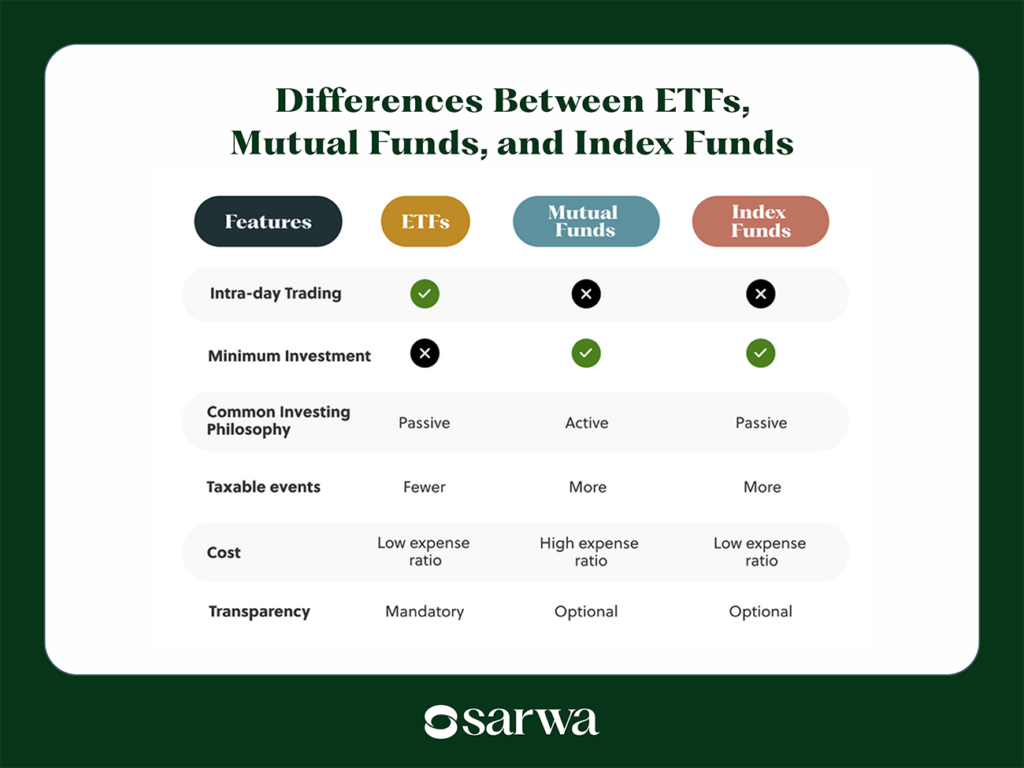

Step 2: Choose Between an ETF and a Mutual Fund

S&P 500 index funds generally come in two flavors: Exchange-Traded Funds (ETFs) and Mutual Funds.

- ETFs (e.g., VOO, SPY, IVV): These trade on an exchange like a stock. You can buy them throughout the day at fluctuating prices. They are often more tax-efficient in taxable accounts and usually have no minimum investment beyond the price of a single share (or even less if your broker allows fractional shares).

- Mutual Funds (e.g., VFIAX, FXAIX, SWPPX): These are priced once at the end of the trading day. They allow for easy automated investing, where you can set a specific dollar amount to be invested every month. However, some mutual funds require a minimum initial investment, such as $3,000.

Step 3: Identify the Ticker Symbol

Once your account is funded, you need to search for the specific fund you want to buy. Here are some of the most popular and lowest-cost S&P 500 index funds:

- Vanguard S&P 500 ETF (VOO): Extremely low expense ratio and highly liquid.

- iShares Core S&P 500 ETF (IVV): A massive fund from BlackRock with very low costs.

- SPDR S&P 500 ETF Trust (SPY): The oldest and most liquid, though its expense ratio is slightly higher than VOO or IVV.

- Fidelity 500 Index Fund (FXAIX): An excellent mutual fund option with one of the lowest expense ratios in the industry.

Step 4: Execute the Trade

In your brokerage platform, enter the ticker symbol, choose the “Buy” action, and specify the number of shares or the dollar amount you wish to invest. If you are buying an ETF during market hours, a “Market Order” will execute the trade immediately at the current price, while a “Limit Order” allows you to set a maximum price you are willing to pay.

Key Factors to Evaluate Before Investing

While most S&P 500 funds are similar, small differences in costs and structure can impact your long-term returns.

The Importance of the Expense Ratio

The expense ratio is the annual fee that the fund provider charges to manage the fund, expressed as a percentage of your investment. For an S&P 500 fund, you should never pay a high fee. The best funds have expense ratios between 0.02% and 0.09%. A 0.03% expense ratio means you pay only $3 per year for every $10,000 invested. Over decades, the difference between a 0.03% fee and a 1.0% fee can amount to hundreds of thousands of dollars in lost gains due to the power of compounding.

Tracking Error and Liquidity

Tracking error measures how closely the fund’s performance follows the actual S&P 500 index. While most major funds have negligible tracking errors, it is a metric worth glancing at in a fund’s prospectus. Liquidity is also vital for ETF investors; high-volume ETFs like SPY or VOO ensure that you can buy or sell shares instantly without significantly affecting the price or dealing with wide bid-ask spreads.

Dividend Reinvestment Plans (DRIP)

The companies in the S&P 500 frequently pay dividends. To maximize your wealth, you should ensure your brokerage account is set to “automatically reinvest dividends.” This means that instead of receiving the dividend as cash, the money is used to buy more shares of the index fund. This creates a powerful compounding loop where you earn dividends on your dividends.

Advanced Strategies for S&P 500 Investors

Once you have mastered the basics of buying a fund, you can optimize your strategy to suit your financial goals and risk tolerance.

Dollar-Cost Averaging vs. Lump Sum

Deciding when to buy can be stressful. Dollar-cost averaging (DCA) involves investing a fixed amount of money at regular intervals (e.g., $500 every month), regardless of whether the market is up or down. This removes the emotional temptation to “time the market” and ensures you buy more shares when prices are low and fewer when prices are high. Conversely, if you have a large windfall, historical data suggests that “lump sum” investing—putting it all in at once—often yields better results because the market tends to go up over time, and the sooner the money is working for you, the better.

The S&P 500 as a Core Holding

While the S&P 500 provides excellent diversification across industries (Technology, Healthcare, Financials, etc.), it consists entirely of large-cap U.S. companies. Many investors use an S&P 500 fund as their “core” holding (perhaps 70-80% of their portfolio) and then “satellite” other investments around it, such as international stocks or small-cap stocks, to achieve even broader diversification.

Tax-Loss Harvesting

In a taxable brokerage account, if the S&P 500 experiences a temporary downturn, you may be able to utilize tax-loss harvesting. This involves selling your shares at a loss to offset capital gains or up to $3,000 of ordinary income on your taxes, then immediately buying a similar (but not “substantially identical”) fund to stay invested in the market. This is an advanced move that can significantly increase after-tax returns.

Long-Term Maintenance and Behavioral Discipline

The most difficult part of buying an S&P 500 index fund is not the purchase itself, but the act of holding it through market volatility.

Weathering the Storms

The stock market does not move in a straight line. History is full of “corrections” (10% drops) and “bear markets” (20% or more drops). During these times, the media often generates fear-based headlines. Successful S&P 500 investors understand that these downturns are a natural part of the economic cycle. Because the index contains the 500 strongest companies in the U.S., it has a 100% historical track record of recovering and reaching new all-time highs.

Avoiding Over-Trading

One of the greatest enemies of investment success is activity. Every time you sell and buy, you risk making a mistake, incurring taxes, or missing out on a sudden recovery. The beauty of the S&P 500 index fund is that it requires no maintenance. There is no need to watch the daily news or analyze earnings reports. By adopting a “buy and hold” mentality, you allow the collective ingenuity of the world’s most successful corporate leaders to work for you.

Reassessing Your Goals

As you approach retirement or your specific financial goal, you may want to gradually shift some of your S&P 500 holdings into more stable assets like bonds or high-yield cash accounts. While the S&P 500 is an incredible wealth generator, its volatility can be risky if you need the money in the very short term. Most experts recommend a five-to-ten-year time horizon for any money placed into an S&P 500 index fund to ensure you can ride out any potential market cycles.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.