Investing in the stock market can often feel like navigating a complex maze, especially for newcomers. With countless individual stocks, bonds, mutual funds, and other financial instruments vying for attention, it’s easy to become overwhelmed. However, there’s one investment vehicle that stands out for its simplicity, broad diversification, and historically robust performance: the S&P 500 index. This guide will demystify the process, offering a clear, professional, and insightful roadmap for how to invest in the S&P 500, positioning you for long-term financial growth.

The S&P 500 isn’t just a collection of stocks; it’s a benchmark, a barometer of the U.S. economy’s health, and a powerful tool for wealth accumulation. Representing 500 of the largest publicly traded companies in the United States, it offers investors immediate diversification across numerous industries, from technology and healthcare to finance and consumer goods. For decades, it has served as a cornerstone of successful investment strategies, embodying the principle that betting on the collective strength of America’s leading enterprises is often a winning long-term play. Whether you’re a seasoned investor looking to simplify your portfolio or a novice taking your first steps into the market, understanding how to effectively harness the power of the S&P 500 is an invaluable skill for building financial resilience and achieving your monetary goals.

Understanding the S&P 500 Index

Before diving into the “how,” it’s crucial to grasp the “what” and “why” behind the S&P 500. This foundational knowledge will empower you to make informed decisions and appreciate the unique advantages this index offers.

What is the S&P 500?

The S&P 500, short for the Standard & Poor’s 500, is a market-capitalization-weighted index of 500 of the largest publicly traded companies in the United States. “Market-capitalization-weighted” means that companies with larger market values have a greater impact on the index’s performance. For instance, Apple and Microsoft, with their multi-trillion-dollar valuations, influence the S&P 500’s movements more significantly than a company with a market cap in the tens of billions. The index is maintained by S&P Dow Jones Indices and is widely regarded as the best gauge of large-cap U.S. equities and the overall health of the American stock market. It’s not a static list; companies are added and removed periodically to ensure it accurately reflects the leading companies in the U.S. economy.

Why Invest in the S&P 500?

The appeal of the S&P 500 stems from several compelling factors that align perfectly with sound investment principles:

- Broad Diversification: By investing in the S&P 500, you are simultaneously investing in 500 different companies across eleven major sectors. This inherent diversification significantly reduces the risk associated with investing in individual stocks. If one company or sector underperforms, its impact on your overall portfolio is mitigated by the performance of the other 499 companies.

- Historical Performance: Over the long term, the S&P 500 has demonstrated remarkable resilience and growth. Since its inception in 1957, the average annual return of the S&P 500 has been approximately 10-12% (including dividends), though past performance is not indicative of future results. This consistent, long-term upward trend makes it a powerful engine for wealth accumulation, especially when compounded over decades.

- Lower Risk Profile: While no investment is without risk, investing in the S&P 500 through an index fund or ETF is generally considered less risky than picking individual stocks. It eliminates the “company-specific risk” where a single bad decision can decimate a large portion of your portfolio. Instead, you’re betting on the enduring strength and innovation of the U.S. economy as a whole.

- Simplicity and Accessibility: For many investors, particularly those new to the market, the S&P 500 offers a straightforward path to participation. You don’t need to be a financial analyst to understand its premise or to invest in it. This accessibility makes it an excellent choice for building a core portfolio.

Common Methods to Invest in the S&P 500

Once you understand the benefits, the next step is to explore the practical avenues available for investing in the S&P 500. Fortunately, there are several highly efficient and cost-effective ways to gain exposure to this index.

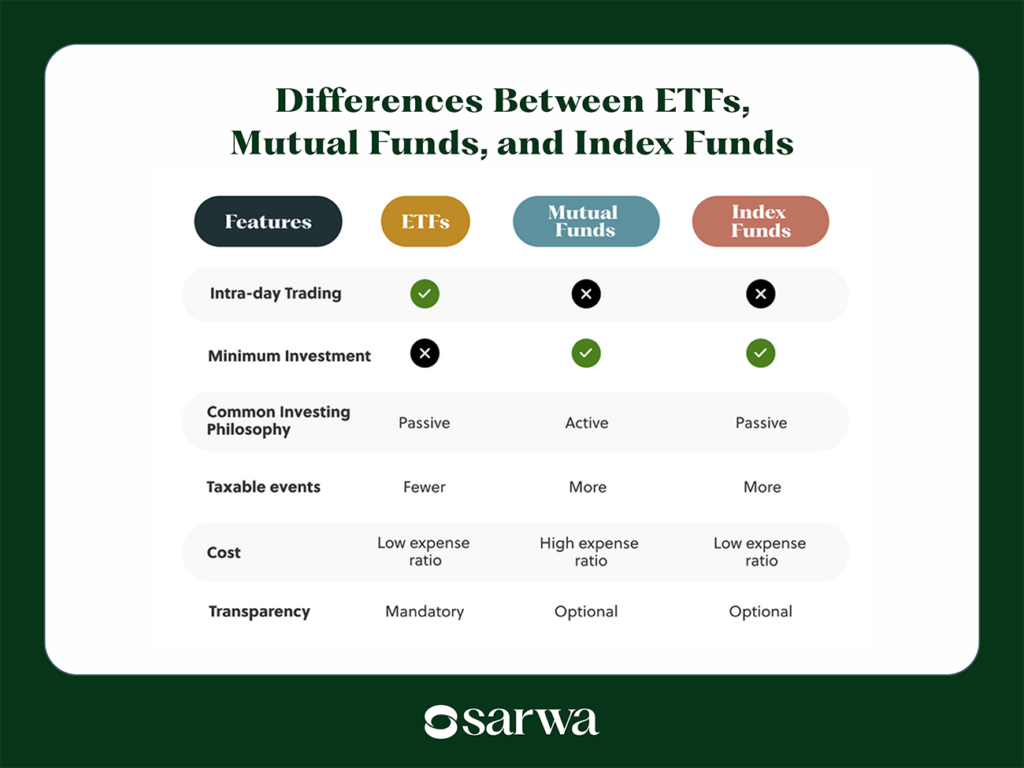

S&P 500 Exchange-Traded Funds (ETFs)

Exchange-Traded Funds (ETFs) are arguably the most popular and flexible way to invest in the S&P 500. An S&P 500 ETF is a type of fund that holds the stocks of the 500 companies in the S&P 500 index in the same proportion as the index itself.

- What are ETFs? ETFs are baskets of securities that trade on stock exchanges, much like individual stocks. When you buy an S&P 500 ETF, you are purchasing a share of a fund that owns all 500 underlying stocks, effectively replicating the index’s performance.

- Advantages:

- Low Expense Ratios: S&P 500 ETFs are passively managed, meaning they simply track the index rather than trying to beat it. This results in very low management fees (expense ratios), often less than 0.10% annually, which significantly preserves your returns over time.

- Liquidity: ETFs can be bought and sold throughout the trading day at market prices, offering flexibility that traditional mutual funds typically do not.

- Diversification: Instant diversification across 500 companies.

- Popular Examples: Some of the largest and most well-known S&P 500 ETFs include:

- SPDR S&P 500 ETF Trust (SPY): The oldest and one of the largest S&P 500 ETFs.

- iShares Core S&P 500 ETF (IVV): Another highly popular, low-cost option from BlackRock.

- Vanguard S&P 500 ETF (VOO): Known for its extremely low expense ratio, typical of Vanguard funds.

- How to Buy Them: You can purchase S&P 500 ETFs through any brokerage account (e.g., Fidelity, Schwab, Vanguard, E*TRADE, Robinhood). Simply open an account, fund it, and search for the ticker symbol of your chosen ETF.

S&P 500 Index Mutual Funds

Index mutual funds are another excellent way to invest in the S&P 500, particularly for those who prefer setting up automated investments.

- What are Index Mutual Funds? Like ETFs, index mutual funds pool money from many investors to invest in a portfolio of securities that mirror a specific index, in this case, the S&P 500.

- Advantages:

- Automatic Reinvestment: Many mutual funds offer automatic dividend reinvestment, allowing your returns to compound effortlessly.

- Simplicity: Often ideal for dollar-cost averaging, where you invest a fixed amount regularly, regardless of market fluctuations.

- Professional Management (Passive): Though passively managed, the fund manager ensures the fund precisely tracks the index.

- Disadvantages:

- Trading Restrictions: Mutual funds are typically traded only once a day after the market closes, at their Net Asset Value (NAV).

- Potentially Higher Expense Ratios: While S&P 500 index mutual funds are generally low-cost, some might have slightly higher expense ratios than their ETF counterparts, or impose minimum investment requirements.

- How to Buy Them: You can purchase S&P 500 index mutual funds through a brokerage account or directly from the fund company (e.g., Vanguard’s VFIAX, Fidelity’s FXAIX). Many 401(k) and 403(b) retirement plans also offer S&P 500 index funds as investment options.

Robo-Advisors

For those who prefer a hands-off approach to investing, robo-advisors offer an automated solution.

- Automated Investment Management: Robo-advisors are digital platforms that use algorithms to build and manage diversified investment portfolios tailored to your financial goals and risk tolerance.

- S&P 500 Inclusion: Many robo-advisors construct portfolios primarily using low-cost ETFs, including S&P 500-tracking funds, alongside other asset classes like bonds and international equities.

- Advantages:

- Low Cost: Generally lower fees than traditional financial advisors.

- Automated Rebalancing: Robo-advisors automatically rebalance your portfolio to maintain your desired asset allocation.

- Goal-Based Planning: They often help set up and track progress towards specific financial goals (e.g., retirement, buying a home).

- Suitable for: Hands-off investors who want professional-grade portfolio management without the high fees or complexity of managing investments themselves. Popular robo-advisors include Betterment, Wealthfront, and Vanguard Digital Advisor.

Setting Up Your Investment Journey

Once you’ve decided on your preferred investment vehicle (ETFs or index mutual funds), the next step involves setting up the practical aspects of your investing journey.

Opening a Brokerage Account

This is your gateway to the stock market. You’ll need an account with a brokerage firm to buy and sell investments.

- Types of Accounts:

- Taxable Brokerage Accounts: Standard investment accounts where capital gains and dividends are taxed in the year they are realized. Best for short-term goals or money you might need before retirement.

- Individual Retirement Accounts (IRAs):

- Traditional IRA: Contributions might be tax-deductible, and growth is tax-deferred until retirement.

- Roth IRA: Contributions are made with after-tax dollars, but qualified withdrawals in retirement are tax-free. Excellent for long-term growth.

- Employer-Sponsored Retirement Plans (401(k), 403(b)): Many employers offer S&P 500 index funds as options within these plans. Maximize these, especially if there’s an employer match.

- Choosing a Broker: Consider factors like fees (commission-free ETF trading is common), platform usability, research tools, customer service, and investment options. Reputable brokers include Vanguard, Fidelity, Charles Schwab, E*TRADE, and Merrill Edge.

- Steps to Open and Fund an Account: The process is typically online and involves providing personal information, linking a bank account for funding, and selecting your desired account type.

Determining Your Investment Strategy

While investing in the S&P 500 is inherently simpler than active stock picking, a clear strategy is still beneficial.

- Time Horizon: S&P 500 investing is almost exclusively a long-term strategy. The benefits of compounding and market recovery from downturns are maximized over decades, not months or a few years. Aim for a time horizon of 5-10 years minimum, ideally much longer.

- Risk Tolerance: While diversified, the S&P 500 is still subject to market volatility. Be prepared for periods where your portfolio value may drop significantly. A strong long-term perspective helps weather these storms.

- Dollar-Cost Averaging (DCA): This is a powerful strategy for S&P 500 investors. It involves investing a fixed amount of money at regular intervals (e.g., $200 every month) regardless of the market’s current price. When prices are high, you buy fewer shares; when prices are low, you buy more shares. Over time, this averages out your purchase price, reduces the impact of volatility, and removes emotional decision-making. Consistency is key.

- Contribution Consistency: The more regularly you contribute, and the earlier you start, the more significant the impact of compounding on your wealth. Make saving and investing a consistent habit.

Key Considerations and Potential Pitfalls

While investing in the S&P 500 is an excellent strategy, being aware of certain considerations will further enhance your success and mitigate potential issues.

Expense Ratios

The expense ratio is the annual fee charged by a fund (ETF or mutual fund) for its management and operational costs, expressed as a percentage of your investment.

- Impact on Long-Term Returns: Even a seemingly small difference in expense ratios can have a massive impact over decades due to compounding. For example, a 0.50% expense ratio versus a 0.03% expense ratio means you’re losing 0.47% of your annual returns to fees. Always opt for the lowest possible expense ratio for S&P 500 index funds/ETFs.

- Comparing Funds: When choosing between similar S&P 500 funds, prioritize those with the lowest expense ratios, assuming they track the index accurately.

Taxes

Understanding the tax implications of your investments is crucial for maximizing your net returns.

- Taxable vs. Tax-Advantaged Accounts: As discussed, investing in tax-advantaged accounts like IRAs and 401(k)s offers significant tax benefits. Prioritize these accounts, especially for long-term growth.

- Capital Gains and Dividends: In taxable brokerage accounts, you’ll pay taxes on capital gains (when you sell a fund for more than you paid) and dividends (income distributions from the fund). Dividends are often automatically reinvested, but they are still taxable in the year they are received in a taxable account.

- Importance of Consulting a Tax Professional: Tax laws are complex and can change. Always consult a qualified tax professional for personalized advice specific to your financial situation.

Market Volatility and Long-Term Perspective

The stock market is cyclical and experiences periods of both growth and decline. The S&P 500, while stable over the long run, is not immune to short-term fluctuations.

- Understanding Market Fluctuations: Bear markets (declines of 20% or more) and corrections (declines of 10% or more) are a normal part of investing. Do not panic and sell during these times; historically, markets have always recovered and reached new highs.

- The Importance of Staying Invested: The biggest mistake investors make is selling during a downturn. Time in the market, not timing the market, is what matters. Remaining invested through turbulent periods allows you to capture the eventual recovery and growth.

- Avoiding Emotional Decisions: Emotional reactions to market news can derail a sound investment strategy. Stick to your plan, continue dollar-cost averaging, and focus on your long-term goals.

Diversification Beyond the S&P 500 (Optional)

While the S&P 500 offers excellent diversification within U.S. large-cap stocks, a truly robust portfolio might consider even broader diversification.

- International Equities: Investing in international developed and emerging markets can provide exposure to global growth and further diversify your portfolio beyond U.S. borders.

- Bonds: As you approach retirement, or if you have a lower risk tolerance, including a small allocation to bonds can help stabilize your portfolio and provide income.

- Real Estate/Other Assets: Depending on your financial situation and goals, other asset classes could also play a role in a highly diversified portfolio.

In conclusion, investing in the S&P 500 through low-cost index funds or ETFs is one of the most effective and accessible strategies for long-term wealth building. By understanding the index, choosing the right investment vehicle, adopting a consistent investment strategy like dollar-cost averaging, and maintaining a long-term perspective through market volatility, you can confidently navigate your financial journey. Start small, stay disciplined, and let the power of the S&P 500 work for you.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.