Managing credit cards effectively is a cornerstone of sound personal finance. While the convenience and flexibility offered by credit cards are undeniable, their benefits are fully realized only when accompanied by diligent and timely bill payments. Understanding “how to pay credit bill” goes beyond merely sending money to your issuer; it encompasses a strategic approach to managing your finances, protecting your credit score, and avoiding unnecessary fees and interest charges. This guide will delve into the various methods of payment, best practices, and crucial considerations to ensure your credit card usage supports your financial goals rather than hindering them.

The Fundamentals of Credit Card Payments

Before exploring the mechanics of payment, it’s vital to grasp the foundational elements that govern your credit card account and its billing cycle. A clear understanding here sets the stage for effective financial management.

Understanding Your Credit Card Statement

Your monthly credit card statement is more than just a bill; it’s a comprehensive report of your spending, payments, and account status. Key elements to scrutinize include:

- Statement Date: The date your billing cycle closes and your statement is generated.

- Payment Due Date: The deadline by which your payment must be received by the issuer. This is typically 21-25 days after the statement date.

- New Balance: The total amount owed for the current billing cycle.

- Minimum Payment Due: The smallest amount you must pay by the due date to keep your account in good standing. Paying only the minimum can lead to significant interest charges over time.

- Previous Balance: The amount owed from the prior billing cycle.

- Transactions: A detailed list of all purchases, cash advances, and balance transfers made during the billing cycle.

- Interest Charged: The interest accrued on any outstanding balance.

- Fees: Any late payment fees, annual fees, or other charges.

Thoroughly reviewing your statement each month helps you track spending, identify potential errors or fraudulent charges, and plan your payment strategy.

The Importance of Timely Payments

Paying your credit card bill on time is arguably the most critical aspect of responsible credit card management. The repercussions of late payments extend far beyond a mere inconvenience, impacting both your immediate finances and long-term financial health.

- Avoid Late Fees: Credit card companies typically charge a late fee, which can be substantial, for payments received after the due date.

- Prevent Interest Accrual: If you don’t pay your full balance by the due date, interest will be charged on the outstanding amount, often retroactively from the date of purchase (if you’ve lost your grace period). This can quickly escalate your debt.

- Protect Your Credit Score: Payment history is the single largest factor in determining your credit score, accounting for 35% of your FICO score. A single late payment reported to credit bureaus (typically 30 days past due) can cause a significant drop in your score, making it harder to secure loans, mortgages, or even rent apartments in the future.

- Maintain Good Standing: Timely payments ensure your account remains in good standing, preserving your access to credit and potentially qualifying you for better card offers or credit line increases.

Consequences of Late or Missed Payments

The cascade effect of late payments can be severe. Missing a payment by more than 30 days will almost certainly be reported to credit bureaus, impacting your credit score for up to seven years. Multiple late payments can lead to:

- Increased Interest Rates: Many credit card agreements include a penalty APR (Annual Percentage Rate) that can be triggered by late payments, significantly increasing the cost of carrying a balance.

- Account Closure or Credit Limit Reduction: Issuers may reduce your credit limit or even close your account if you consistently fail to make timely payments, further damaging your credit utilization ratio and score.

- Collection Efforts: For severely overdue accounts, the issuer may sell your debt to a collection agency, leading to aggressive collection calls and further negative marks on your credit report.

- Difficulty Obtaining Future Credit: A history of late payments signals high risk to potential lenders, making it challenging to qualify for loans, mortgages, or even other credit cards at favorable terms.

Diverse Methods for Credit Bill Payment

Fortunately, modern banking offers a variety of convenient ways to pay your credit card bill, catering to different preferences and technological comfort levels. Choosing the right method can enhance your ability to pay on time consistently.

Online Banking and Mobile Apps

The most popular and often recommended method for bill payment is through your credit card issuer’s online portal or mobile application.

- Convenience: Payments can be made 24/7 from anywhere with an internet connection.

- Speed: Payments often process quickly, sometimes within minutes, though they may take 1-2 business days to post to your account.

- Control: You can initiate payments manually, choose the exact amount, and select the payment date.

- Tracking: Digital platforms provide instant confirmation and a clear record of your payment history.

- Security: These platforms employ robust encryption and security measures to protect your financial information.

To pay online, you typically link a checking or savings account from which funds will be drawn. Ensure you have sufficient funds to cover the payment to avoid non-sufficient funds (NSF) fees from your bank.

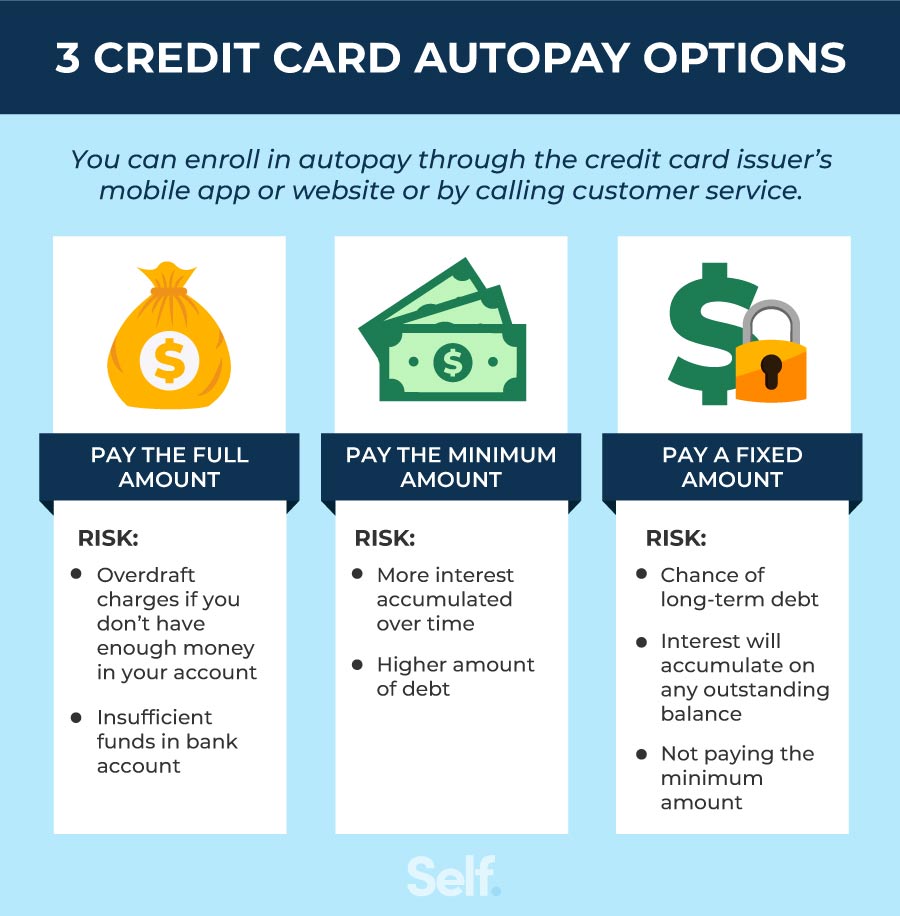

Automated Payments: Setting Up Auto-Pay

For ultimate peace of mind and to virtually eliminate the risk of missing a due date, automated payments are an excellent option.

- Guaranteed On-Time Payments: Auto-pay ensures your payment is made consistently by the due date, protecting your credit score and avoiding late fees.

- Customizable: You can usually set auto-pay to transfer the minimum payment, the full statement balance, or a fixed amount each month. Paying the full statement balance is highly recommended to avoid interest charges.

- Reduced Stress: Once set up, you no longer need to remember to make manual payments.

However, always monitor your account for fraudulent activity and ensure you have enough funds to cover the automated payment. Review your statements even with auto-pay enabled to verify transactions and confirm payments are processed correctly.

Traditional Payment Methods: Phone, Mail, and In-Person

While less common for everyday payments, these methods still serve an important purpose.

- Payment by Phone: You can call your credit card company’s customer service number and make a payment over the phone, typically using a linked bank account or debit card. Some issuers may charge a small fee for this service, especially for expedited payments.

- Payment by Mail: Sending a check or money order via postal service is a viable option, but it requires careful planning due to mail transit times. Always mail your payment several business days before the due date to ensure it arrives on time. Include the payment coupon from your statement and write your account number on the check.

- In-Person Payments: Some credit card issuers, particularly those affiliated with a bank, allow you to make payments at their physical branches. Retail credit cards may also accept payments at their store locations. This method offers immediate confirmation of payment.

Third-Party Payment Services

In some cases, you might use third-party bill payment services, such as those offered by your bank’s online banking platform or independent services like Plastiq (for payments that aren’t typically accepted by credit card). Be mindful of any fees associated with these services and ensure their processing times align with your credit card’s due date.

Best Practices for Optimal Credit Management

Beyond choosing a payment method, adopting smart habits can significantly enhance your credit card management and overall financial health.

Paying in Full vs. Minimum Payments

This is a critical distinction for your financial well-being:

- Paying in Full: Always aim to pay your full statement balance each month. This strategy ensures you avoid all interest charges and utilize your credit card purely for its convenience and rewards. It’s the most financially responsible approach.

- Minimum Payments: While paying the minimum keeps your account in good standing and avoids late fees, it allows interest to accrue on the remaining balance. Over time, paying only the minimum can lead to carrying debt for years, paying significantly more than the original purchase price due to compounding interest. If you can only afford the minimum, make it a priority to pay more as soon as possible.

Monitoring Your Payment Schedule and Due Dates

Vigilance is key. Regardless of your chosen payment method:

- Calendar Reminders: Set up digital calendar reminders a few days before each due date.

- Issuer Alerts: Most credit card companies offer email or SMS alerts to notify you of upcoming due dates, statements ready, and payment confirmations.

- Consistent Review: Regularly check your online account or mobile app to confirm payments have posted and to monitor your current balance.

Strategies for Multiple Credit Cards

If you manage several credit cards, organization is paramount.

- Centralized Tracking: Use a spreadsheet or a personal finance app to track due dates, minimum payments, and balances for all your cards.

- Payment Prioritization: If you can’t pay all cards in full, prioritize paying down cards with the highest interest rates first (the “debt avalanche” method) after ensuring all minimum payments are met. Alternatively, some prefer the “debt snowball” method of paying off the smallest balances first for psychological wins.

- Staggered Due Dates: Contact your issuers to potentially adjust due dates so they are spread throughout the month, making it easier to manage cash flow.

Leveraging Payment Reminders and Alerts

Take advantage of every tool at your disposal to ensure timely payments. Beyond issuer alerts, many personal finance apps (like Mint, YNAB, or even your bank’s app) offer customizable reminders for bills due across all your accounts. These proactive notifications serve as an essential safeguard against oversight.

Navigating Challenges and Advanced Strategies

Even with the best intentions, financial difficulties can arise. Knowing how to react can mitigate long-term damage.

What to Do If You Can’t Pay Your Bill

If you anticipate or face difficulty paying your credit card bill, immediate action is crucial:

- Contact Your Issuer Immediately: Don’t wait until after the due date. Explain your situation. They may offer options like a temporary hardship program, a deferred payment, or a reduced interest rate.

- Prioritize Payments: If you absolutely cannot pay in full, at least make the minimum payment to avoid late fees and a negative mark on your credit report.

- Emergency Fund: This is precisely what an emergency fund is for. If you have one, consider using it to cover essential payments to protect your credit.

- Budget Review: Re-evaluate your budget to cut non-essential spending and free up funds for debt repayment.

Impact of Payments on Your Credit Score

Every payment you make (or don’t make) shapes your credit score.

- Positive Impact: Consistent, on-time payments of the full balance demonstrate financial responsibility and steadily build a strong credit history, leading to higher credit scores.

- Negative Impact: Late payments (especially 30+ days overdue), missed payments, and consistently carrying a high balance (high credit utilization) can severely harm your score, making future credit more expensive or inaccessible. Keeping your credit utilization (the percentage of your credit limit you’re using) below 30% is generally recommended for a good score.

Seeking Professional Financial Guidance

If you find yourself consistently struggling with credit card debt or feel overwhelmed, don’t hesitate to seek professional help. Non-profit credit counseling agencies can provide personalized advice, help you create a debt management plan, or guide you through options like debt consolidation. These services can be a lifeline, offering structured solutions and education to help you regain control of your finances.

Conclusion: Mastering Your Credit Payments for Financial Well-being

Paying your credit bill is a fundamental responsibility that underpins your entire financial health. It’s a continuous process that requires attention, discipline, and a clear understanding of the tools and strategies available. By embracing timely payments, leveraging modern payment methods, and adopting best practices like paying in full, you not only avoid costly fees and interest but also build a robust credit history that opens doors to better financial opportunities. Mastering the art of credit bill payment is not just about settling a debt; it’s about investing in your financial future and achieving peace of mind.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.