For many taxpayers, the annual ritual of filing taxes brings with it the inevitable question of how to settle any outstanding balance. While traditional methods like direct bank transfers or checks remain popular, the digital age has ushered in a range of electronic payment options, including the increasingly considered choice of using a credit card. Paying your IRS bill with plastic might seem counterintuitive at first, given the associated fees and potential for interest. However, for certain individuals and specific financial strategies, it can be a surprisingly advantageous route. This guide delves into the intricacies of paying your IRS taxes with a credit card, examining the mechanics, benefits, drawbacks, and strategic considerations to help you determine if this method aligns with your financial goals.

Understanding Your IRS Payment Options

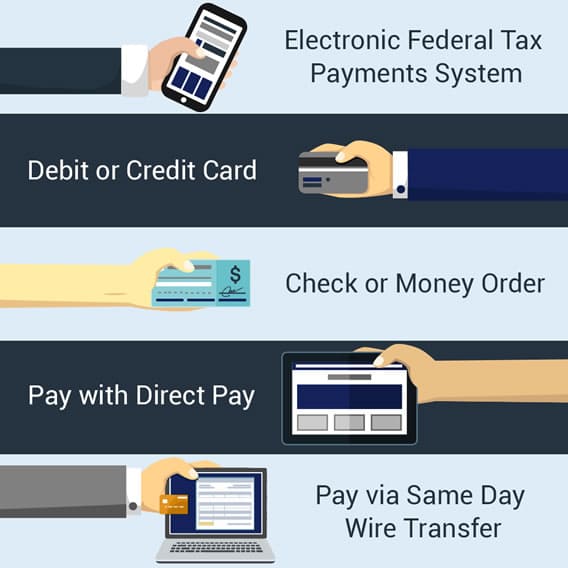

Before exploring the specifics of credit card payments, it’s crucial to understand the full spectrum of payment methods the IRS accepts. This context helps in evaluating whether a credit card truly offers an advantage over other, potentially more straightforward, options. The IRS aims to make tax payments as accessible as possible, offering a variety of methods to suit different taxpayer needs and preferences.

Direct Pay from Bank Account

One of the most common and cost-effective ways to pay your federal taxes is through IRS Direct Pay. This free service allows you to pay directly from your checking or savings account. It’s simple, secure, and there are no processing fees involved. You can schedule payments up to 365 days in advance, making it ideal for planning.

Electronic Federal Tax Payment System (EFTPS)

EFTPS is another free service offered by the Treasury Department. Primarily used by businesses but available to all taxpayers, it allows for federal tax payments to be made electronically. It requires enrollment and a verification process, but once set up, it offers a secure and convenient way to schedule payments for various federal taxes.

Debit Card, Credit Card, or Digital Wallet

This category is where our focus lies. The IRS does not directly process credit card payments. Instead, it authorizes third-party payment processors to handle these transactions. These processors charge a convenience fee for their service, which is a critical factor to weigh when considering this payment method. Digital wallet options, such as PayPal, may also fall under this umbrella, utilizing the same third-party processors.

Check or Money Order

For those who prefer traditional methods, paying by check or money order remains an option. You would typically mail your payment along with a payment voucher (e.g., Form 1040-V) to the IRS. While reliable, this method requires careful attention to mailing deadlines and can be slower than electronic options.

Cash

Paying with cash is also possible, though less common. This can be done in person at one of the IRS’s retail partners, often requiring a payment voucher and generating a receipt for your records. It’s an option primarily for those without bank accounts or who prefer handling cash.

Each of these methods has its pros and cons, and the optimal choice often depends on individual financial circumstances, the amount owed, and the desire for convenience or specific financial benefits.

The Mechanics of Paying IRS with a Credit Card

Once you’ve decided to consider paying your tax bill with a credit card, understanding the operational steps and associated costs is paramount. The process is straightforward, but awareness of the fees and approved channels is key to a smooth transaction.

Authorized Payment Processors

The IRS mandates that all credit and debit card payments be made through approved third-party payment processors. This is a crucial distinction: you do not pay the IRS directly with your credit card. The IRS lists these providers on its official website. Currently, there are typically three or four such processors, each offering slightly different fee structures and payment methods. It’s advisable to check the IRS website for the most current list and their respective fees before proceeding. These processors act as intermediaries, taking your credit card information, charging a convenience fee, and then transmitting your payment to the IRS.

Step-by-Step Payment Process

Paying through an authorized processor typically involves these steps:

- Visit the IRS Website: Navigate to the “Pay Your Taxes” section on IRS.gov.

- Choose Your Payment Method: Select the option for debit, credit card, or digital wallet.

- Select a Processor: The IRS website will list the authorized third-party processors. Click on the one you choose.

- Enter Payment Details: You’ll be redirected to the processor’s secure website. Here, you’ll enter your tax payment details (e.g., tax year, type of tax, amount), your personal information, and your credit card details.

- Review and Confirm: Before finalizing, carefully review all the information, including the total amount to be charged (your tax liability plus the convenience fee).

- Receive Confirmation: Upon successful payment, you’ll receive a confirmation number from the payment processor. It’s essential to keep this for your records, as it serves as proof of payment.

Understanding Convenience Fees

The most significant financial consideration when paying with a credit card is the convenience fee. This fee, charged by the third-party processor, is typically a percentage of your tax payment, ranging from about 1.87% to 1.99%. While it might seem small, on a large tax bill, it can add up quickly. For instance, paying a $5,000 tax bill with a 1.96% fee would cost an additional $98. These fees are non-refundable, even if you later amend your return and receive a refund. It’s critical to factor this cost into your decision-making process.

Pros and Cons: Is Paying IRS with a Credit Card Right for You?

Deciding whether to use a credit card for your tax payment requires a careful evaluation of the potential benefits against the costs and risks. For some, it’s a savvy financial move; for others, it could lead to unnecessary debt.

The Advantages

- Earning Rewards and Miles: This is often the primary motivator for using a credit card. If you have a rewards credit card that offers significant cash back, travel miles, or points, the value of these rewards might partially or even fully offset the convenience fee. For instance, if you have a card that offers 2% cash back, and the fee is 1.87%, you could theoretically come out ahead.

- Payment Flexibility and Bridge Financing: A credit card can provide a temporary financial bridge if you don’t have enough cash on hand by the tax deadline. It allows you to pay your taxes on time, avoiding late payment penalties from the IRS, and then gives you more time to gather the funds to pay off your credit card balance.

- Meeting Minimum Spending Requirements: Many premium credit cards offer substantial sign-up bonuses if you spend a certain amount within a specified timeframe. A large tax payment can easily help you meet these spending requirements, unlocking thousands of dollars in rewards or travel credits.

- Emergency Situations: In unexpected financial emergencies where liquid cash is unavailable, a credit card can be a last resort to fulfill your tax obligations and prevent more severe penalties from the IRS.

The Disadvantages

- Convenience Fees: As discussed, these fees can quickly erode any potential rewards benefits and represent an additional cost to your tax bill. Always calculate the net benefit (rewards earned minus fees paid).

- Potential for High-Interest Debt: If you cannot pay off your credit card balance in full and on time, the interest charges will almost certainly outweigh any rewards earned and the initial convenience fee. Credit card interest rates are typically high, and carrying a balance for even a few months can make your tax payment significantly more expensive. The IRS’s underpayment penalty and interest rates, while not negligible, might sometimes be lower than credit card interest.

- Impact on Credit Score: While paying off a large balance quickly can positively impact your credit utilization, carrying a high balance on your credit card, even temporarily, can increase your credit utilization ratio, potentially lowering your credit score. This is especially true if you are close to your credit limit.

Strategic Use of Credit Cards for Tax Payments

For those who decide to proceed, a strategic approach is essential to maximize benefits and minimize drawbacks. It’s not just about paying; it’s about paying smartly.

Calculating Your Net Benefit

Before making any payment, perform a clear calculation:

- Rewards Value: Estimate the monetary value of the rewards, points, or cash back you will earn from the tax payment.

- Convenience Fee: Determine the exact fee charged by the chosen processor.

- Net Gain/Loss: Subtract the convenience fee from the rewards value. Only proceed if there is a clear net gain or if the flexibility gained is worth the cost. Remember to account for any annual fees on your credit card if using it specifically for this purpose.

Choosing the Right Credit Card

Not all credit cards are created equal for tax payments.

- High Rewards Rate: Prioritize cards that offer a high flat-rate cash back (e.g., 2% on all purchases) or bonus categories that might occasionally include tax payments (though this is rare).

- Sign-Up Bonuses: If you’re chasing a sign-up bonus, ensure the tax payment will contribute to the minimum spending requirement and that the bonus value far exceeds the convenience fee.

- 0% APR Introductory Offers: Some credit cards offer 0% APR on new purchases for an introductory period (e.g., 12-18 months). If you can secure such a card and pay off your tax balance before the promotional period ends, you can effectively get an interest-free loan for your tax payment, making the convenience fee the only additional cost.

Avoiding Interest Charges

This is arguably the most critical aspect of paying with a credit card. Always plan to pay off your entire tax-related credit card balance before interest accrues. If you can’t commit to this, using a credit card for tax payments is likely a poor financial decision. Treat the credit card as a short-term cash flow management tool, not a means to finance an unpaid tax bill over the long term.

Considering Alternative Short-Term Funding

Before defaulting to a credit card, explore other short-term financing options if cash is tight:

- Personal Loan: If you have excellent credit, a low-interest personal loan could be a cheaper alternative than high-interest credit card debt.

- Home Equity Line of Credit (HELOC): For homeowners, a HELOC typically offers lower interest rates than credit cards, though it uses your home as collateral.

- Payment Plan with IRS: If you genuinely cannot afford to pay your taxes, the IRS offers various relief programs, including installment agreements (monthly payments) and offers in compromise. These options often have lower penalties and interest rates than credit cards and should be explored before incurring high-interest credit card debt.

Important Considerations and Best Practices

Successful navigation of credit card tax payments also involves an awareness of deadlines, potential penalties, and diligent record-keeping.

Payment Deadlines and Penalties

Regardless of your chosen payment method, understanding IRS payment deadlines is paramount. Filing your return on time but failing to pay can still result in penalties. The failure-to-pay penalty is 0.5% of the unpaid taxes for each month or part of a month that taxes remain unpaid, up to a maximum of 25% of your unpaid tax liability. By using a credit card, you can ensure your payment is registered on time, thus avoiding these specific penalties, even if you incur credit card interest.

Large Tax Liabilities

When dealing with very large tax liabilities, the convenience fees can become substantial. For example, a $50,000 tax bill at a 1.96% fee would cost $980 in fees. You would need to earn significantly more in rewards to make this worthwhile. In such cases, carefully evaluate if the rewards truly outweigh this substantial fee, or if alternative strategies like installment agreements are more prudent. Some credit cards might have daily or per-transaction spending limits, so if your tax bill is exceptionally high, you might need to make multiple payments or verify with your card issuer.

Alternative Payment Solutions for Financial Hardship

If you are facing true financial hardship and cannot pay your taxes, do not automatically resort to credit cards if you cannot pay them off. The IRS has programs designed to help:

- Installment Agreement: Allows you to make monthly payments for up to 72 months.

- Offer in Compromise (OIC): Allows certain taxpayers to resolve their tax liability with the IRS for a lower amount than they originally owed, based on their ability to pay, income, expenses, and asset equity.

- Temporary Delay in Collection: In some situations, the IRS may determine that you cannot pay any of your tax debt due to financial hardship.

These solutions are generally more favorable than accumulating high-interest credit card debt if you cannot pay your balance in full.

Record Keeping

Always maintain meticulous records of your tax payment.

- Confirmation Numbers: Keep the confirmation number provided by the third-party payment processor.

- Credit Card Statements: Retain statements showing the tax payment transaction.

- IRS Records: Verify that the IRS has recorded your payment correctly, which you can usually do by checking your tax account online or reviewing official correspondence.

In conclusion, paying your IRS tax bill with a credit card is a viable option for a specific subset of taxpayers. It offers benefits like earning rewards, gaining payment flexibility, and helping meet sign-up bonuses. However, these advantages are closely tied to the crucial condition of paying off the credit card balance in full and on time to avoid high-interest charges. By carefully calculating the costs versus benefits, choosing the right card, and adhering to best financial practices, you can leverage this payment method to your advantage. For others, particularly those unable to eliminate the credit card debt quickly, traditional, fee-free payment methods or IRS-offered payment plans will remain the more fiscally responsible choices.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.