The journey through higher education often comes with a significant financial component, and for many, that means student loans. While these loans can be invaluable in funding an education, they can also become a source of confusion and stress, especially if you lose track of them. Whether you’re nearing graduation, contemplating repayment, or simply trying to get a clearer picture of your financial obligations years after leaving school, knowing precisely how many student loans you have, who services them, and what their terms are is a fundamental step toward effective financial management.

For many, the initial excitement of academic pursuits often overshadows the intricate details of loan agreements. Over time, servicers can change, contact information can become outdated, and the sheer volume of paperwork can lead to critical information being misplaced. This article will serve as your comprehensive guide to uncovering your student loan landscape, outlining the official channels, practical strategies, and proactive steps you can take to regain control and clarity over your financial future.

The Critical Importance of Knowing Your Student Loan Landscape

Losing sight of your student loans isn’t just an inconvenience; it can have significant financial repercussions. Understanding your complete loan portfolio is the bedrock of responsible repayment and financial planning.

Why Tracking Your Loans is Non-Negotiable

Knowing the specifics of each student loan – including the principal balance, interest rate, loan servicer, and repayment status – is essential for several reasons. Firstly, it allows you to accurately budget for monthly payments, preventing missed payments that can negatively impact your credit score and lead to penalties. Secondly, it empowers you to explore and select the most suitable repayment plan, whether that’s an income-driven repayment (IDR) plan for federal loans or refinancing options for private loans. Without a full picture, you might inadvertently pay more than necessary or miss out on beneficial programs. Furthermore, tracking your loans helps you identify potential errors, negotiate better terms (if applicable), and avoid the severe consequences of default, which can include wage garnishment, tax refund offsets, and damage to your creditworthiness for years. In essence, knowledge is power when it comes to managing substantial debt like student loans.

Common Scenarios Leading to Lost Loan Information

It’s surprisingly common for individuals to lose track of their student loans. Several factors contribute to this phenomenon:

- Graduation and Life Transitions: Once you leave school, the consistent communication from your university’s financial aid office often ceases. As you move, change jobs, or update contact information, critical loan notices might fail to reach you.

- Changing Loan Servicers: Federal and private loan servicers can change over the lifespan of a loan. A loan originally serviced by Company A might be transferred to Company B without you fully grasping the implications or updating your records. These transitions, while usually accompanied by notifications, can sometimes be overlooked.

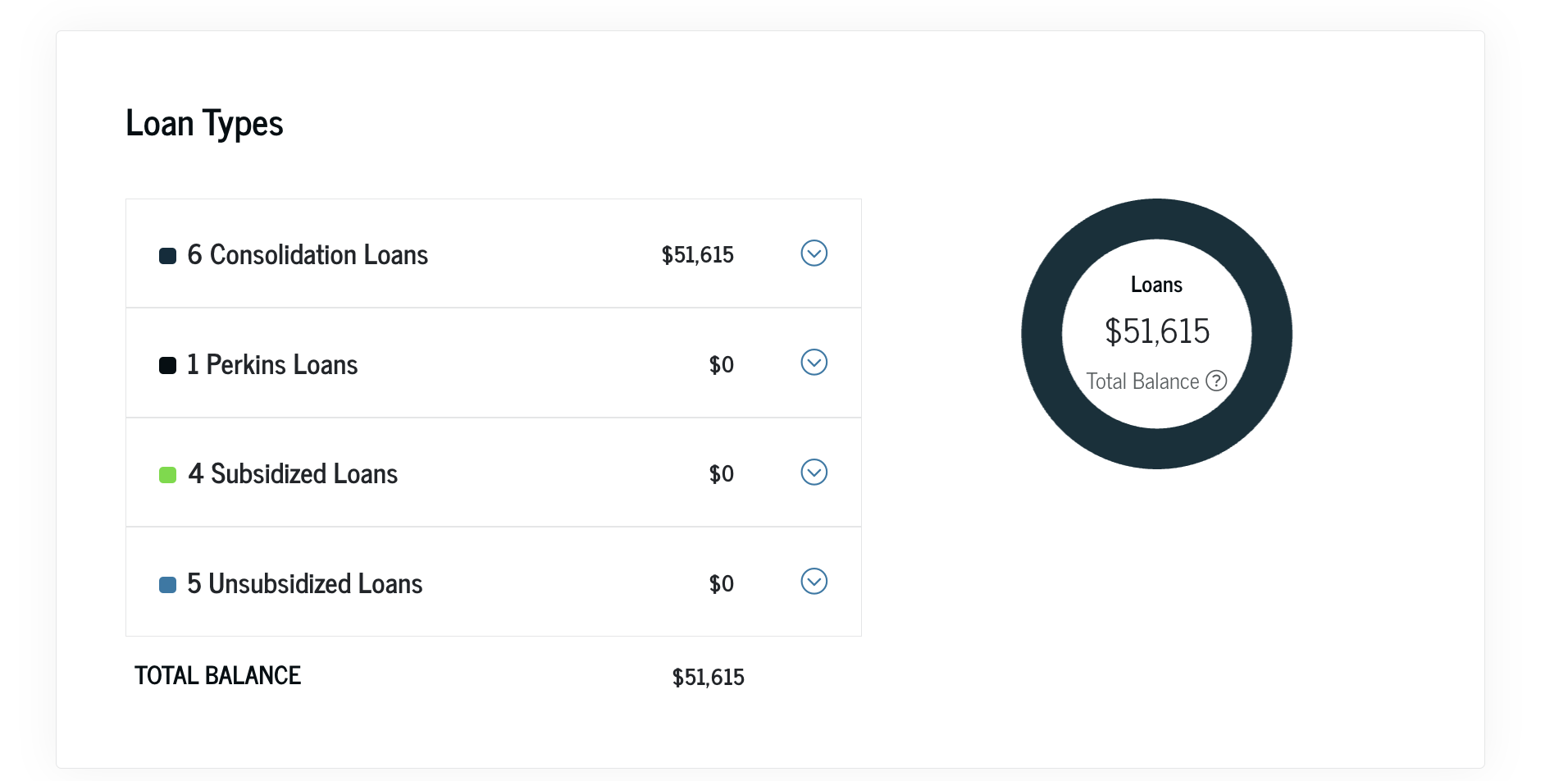

- Multiple Loans and Lenders: Many students take out multiple loans over several years from various sources – federal Direct Loans, Perkins Loans, FFELP loans, and private loans from different banks. Juggling numerous accounts, each with its own servicer and terms, can quickly become overwhelming.

- Time Lapse: Years can pass between borrowing and seriously engaging with repayment. Memories fade, and paper records get lost. Forgetting the specifics of loans taken out during an earlier phase of life is a natural occurrence.

Official Avenues for Federal Student Loan Discovery

For federal student loans, there are established, centralized systems designed to help you locate all your outstanding debts. These are your primary go-to resources.

Leveraging the National Student Loan Data System (NSLDS)

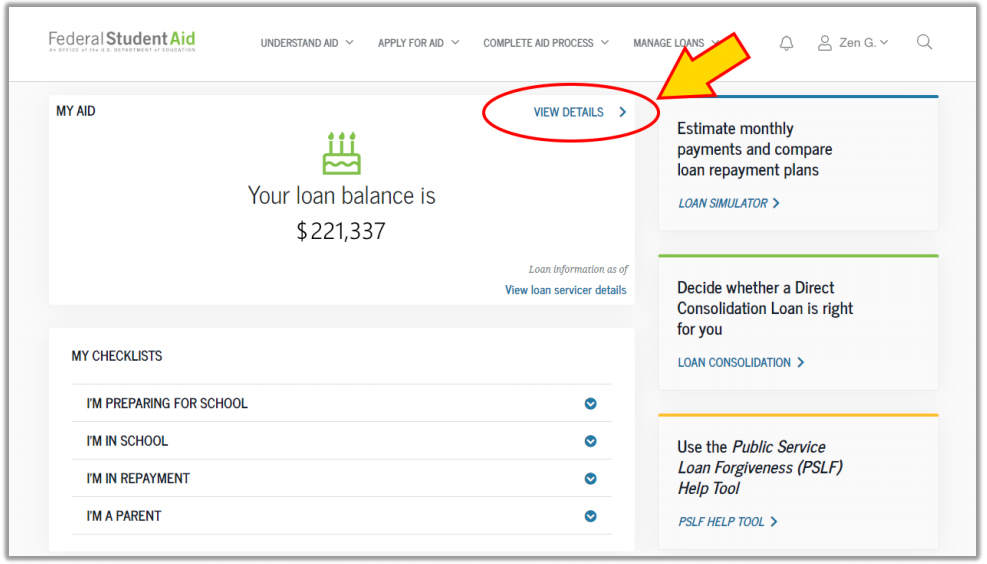

The National Student Loan Data System (NSLDS) is the U.S. Department of Education’s central database for federal student aid. It contains information on all federal grants and loans received by students, including details about your lenders, loan servicers, loan statuses, and current balances. This is arguably the single most important tool for finding your federal student loans.

To access your information, you’ll need to visit the Federal Student Aid website (StudentAid.gov) and log in using your FSA ID. If you don’t have an FSA ID, you’ll need to create one, which requires your Social Security number, date of birth, and full name. Once logged in, navigate to your “Dashboard” or “My Aid” section, where you should find a comprehensive list of all your federal student loans and grants, along with their respective servicers and contact information. This system provides a historical record, helping you trace loans even if they’ve changed hands.

Contacting Your Federal Loan Servicer(s)

Once you’ve identified your loan servicer(s) through NSLDS, the next step is to contact them directly. Each federal student loan servicer has a dedicated website and customer service line. They are responsible for managing your loan accounts, processing payments, and providing detailed information about your specific loans.

- Identifying Servicers: The NSLDS will list the current servicer for each of your federal loans.

- Direct Contact Methods: Visit the servicer’s website, log into your account (or create one if you haven’t already), and you’ll find information on your loan balances, interest rates, payment history, and available repayment plans. You can also call their customer service number for personalized assistance. It’s crucial to have your account number or Social Security number ready to verify your identity.

Understanding Different Federal Loan Types and Their Origins

Federal student loans are not monolithic. Understanding their different types can sometimes help you trace them, especially if NSLDS proves challenging for some reason (though it’s rare).

- Direct Loans: These are loans made directly by the U.S. Department of Education. They include Subsidized, Unsubsidized, PLUS, and Consolidation Loans. Most new federal student loans fall into this category.

- Federal Family Education Loan (FFEL) Program Loans: These loans were made by private lenders but guaranteed by the federal government. The FFEL Program ended in 2010, but many borrowers still have outstanding FFELP loans. These loans might be serviced by various agencies, even though they are federal in nature.

- Perkins Loans: These were low-interest federal student loans for undergraduate and graduate students with exceptional financial need. The program officially ended, and final disbursements were made in 2017. Some schools were the lenders and servicers for Perkins Loans, making their tracking slightly different from Direct Loans.

Knowing these categories helps you contextualize the information you find and understand potential differences in repayment options or consolidation eligibility.

Navigating the Private Student Loan Maze

Private student loans, unlike federal ones, do not appear on the NSLDS database. They are issued by banks, credit unions, and other private financial institutions. Finding them requires a different approach, primarily relying on your financial history and personal records.

Checking Your Credit Report: A Powerful Tool

Your credit report is an invaluable resource for uncovering private student loans. Lenders, both federal and private, report loan accounts to the three major credit bureaus: Equifax, Experian, and TransUnion.

- How to Access: You are entitled to a free copy of your credit report from each of the three major bureaus once every 12 months via AnnualCreditReport.com. It’s advisable to check all three, as some lenders may only report to one or two.

- What to Look For: Carefully review the “Accounts” section of your credit report. Look for entries labeled “student loan,” “education loan,” or similar. Each entry should specify the lender’s name, the account number, the original loan amount, and the current balance. This information will provide you with the identity of your private loan lenders.

- Importance of Regular Checks: Regularly checking your credit report not only helps you find existing loans but also allows you to monitor for identity theft and errors.

Reaching Out to Your Financial Institutions

If you suspect you took out private loans but can’t find them on your credit report (which is rare but possible, especially for very old or recently opened loans that haven’t yet been reported), consider reaching out to financial institutions you’ve banked with in the past.

- Banks and Credit Unions: If you remember applying for a student loan through a specific bank or credit union, contact their loan department directly. They may be able to search their records using your personal information.

- Reviewing Old Academic or Financial Aid Records: When you originally applied for student loans, you would have received disclosure statements, promissory notes, and financial aid award letters. Digging through old emails, physical files, or university portals might reveal information about private lenders you used. These documents would explicitly name the lender and provide contact details.

Reviewing Old Academic or Financial Aid Records

Your past academic institutions often retain records of the financial aid you received. While they won’t typically have detailed servicer information for private loans, they might have records of the initial private lenders listed on your financial aid award letters or other application documents. Similarly, your own old financial aid offer letters or loan promissory notes, if you still have them, would clearly state the lender and original terms. This can be a tedious process, but it can be a last resort if other methods fail for private loans.

Steps to Take When Information Remains Elusive

Despite utilizing official channels and credit reports, some loan information might still be hard to pin down. Here are additional investigative steps.

Utilizing Past Bank Statements and Tax Records

Your financial paper trail often holds clues:

- Bank Statements: Review old bank statements for recurring debits labeled “student loan payment.” The payee’s name on these transactions will be your loan servicer or lender. This method is particularly useful if you’ve been making payments but forgotten who you’re paying.

- Tax Records: If you’ve ever claimed the student loan interest deduction on your federal income tax return, your tax records (specifically, Schedule A or the “Student Loan Interest Deduction Worksheet”) will show the amount of interest paid and potentially the lender’s or servicer’s name, as they are required to send you a 1098-E form detailing interest paid. This form identifies the recipient of the interest.

Consulting Financial Advisors or Credit Counselors

If you’ve exhausted all other avenues and still can’t locate all your loans, or if you feel overwhelmed by the process, consider seeking professional help:

- Certified Financial Planners (CFPs): A CFP specializing in debt management or personal finance can help you piece together your financial history and strategize on how to uncover hidden loans.

- Non-Profit Credit Counseling Agencies: Organizations like the National Foundation for Credit Counseling (NFCC) offer services that can help you understand your credit report, identify creditors, and develop a debt repayment plan. They often provide their initial consultations for free or at a low cost.

What to Do If You Suspect Fraud or Errors

Finding discrepancies or unfamiliar loans on your credit report or other records could indicate an error or, more seriously, identity theft.

- Disputing Information: If you find a loan that doesn’t belong to you on your credit report, dispute it with all three credit bureaus immediately. Provide any evidence you have to support your claim.

- Identity Theft: If you suspect identity theft, report it to the Federal Trade Commission (FTC) at IdentityTheft.gov. They can guide you through the process of reporting the theft, placing fraud alerts on your credit, and recovering your identity. Act quickly, as identity theft can severely damage your financial health.

Proactive Strategies for Future Loan Management

Once you’ve successfully located all your student loans, the next crucial step is to implement strategies to keep them organized and manageable moving forward. Proactive management prevents future confusion and empowers you to make informed financial decisions.

Creating a Centralized Loan Portfolio

The most effective way to manage multiple loans is to create a single, comprehensive record.

- Spreadsheets: A simple spreadsheet can be incredibly powerful. Include columns for each loan’s name (e.g., “Direct Subsidized Loan, Year 1”), original principal, current balance, interest rate, servicer name, servicer contact information, account number, repayment plan type, and monthly payment due date and amount.

- Online Tools/Apps: Many personal finance apps and websites (e.g., Mint, YNAB, specific student loan management platforms) allow you to link your loan accounts, providing a consolidated view of your debts, payment schedules, and progress. Choose a tool that offers robust security and features that meet your needs.

- Physical Binder: For those who prefer paper, a dedicated binder with printed statements, promissory notes, and contact information for each loan servicer can serve as a reliable backup.

Regularly update this portfolio as balances change, payments are made, or servicers are reassigned.

Maintaining Regular Communication with Servicers

Don’t wait for problems to arise. Proactive communication with your loan servicers is key to smooth management.

- Update Contact Information: Ensure your physical mailing address, email address, and phone number are always current with every single loan servicer. This prevents missed notifications about account changes, repayment options, or important program updates.

- Understand Your Statements: Thoroughly review your monthly statements. They contain critical information about your payment history, accrued interest, and remaining balance. If anything seems unclear or incorrect, contact your servicer immediately.

- Ask Questions: If you’re struggling to make payments, facing financial hardship, or simply want to explore different repayment options, reach out to your servicer. They can explain available programs (like income-driven repayment for federal loans, deferment, or forbearance) and help you navigate your options.

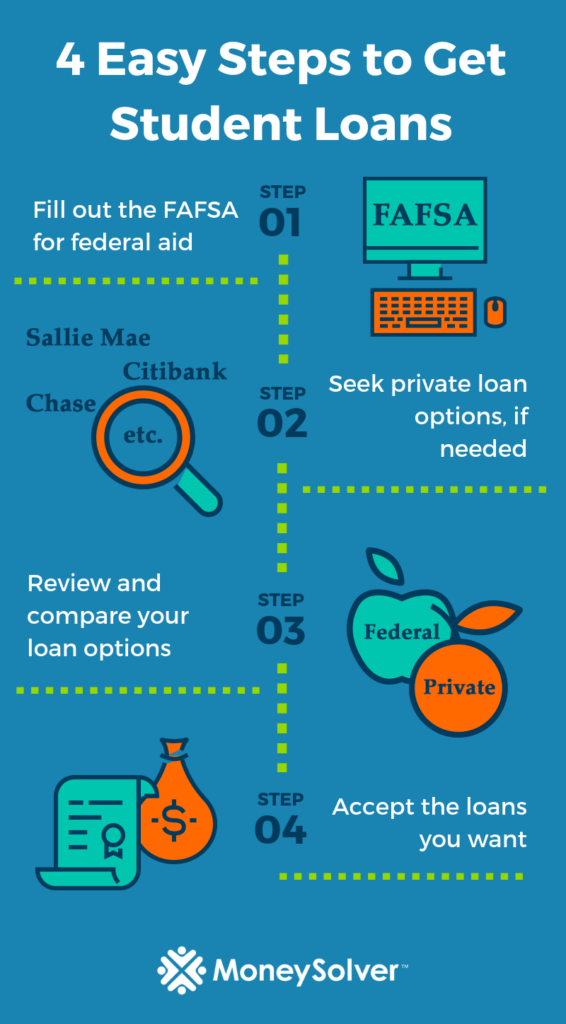

Understanding Repayment Options and Consolidation

Once you have a clear picture of all your loans, you can make strategic decisions about their repayment.

- Repayment Plans (Federal Loans): Familiarize yourself with the various federal repayment plans, including the Standard, Graduated, Extended, and Income-Driven Repayment (IDR) plans (REPAYE, PAYE, IBR, ICR). Each has different terms and eligibility requirements, and choosing the right one can significantly impact your monthly budget and long-term costs.

- Loan Consolidation (Federal Loans): A Direct Consolidation Loan allows you to combine multiple federal student loans into a single new loan with one servicer and one monthly payment. This can simplify your repayment and potentially allow access to certain IDR plans or Public Service Loan Forgiveness that some older loan types might not qualify for independently. Be aware that consolidation can sometimes extend your repayment period and might result in a slightly higher overall interest paid due to interest rate rounding.

- Refinancing (Private and Federal Loans): Refinancing involves taking out a new loan, typically from a private lender, to pay off existing student loans (both federal and private). This is often done to secure a lower interest rate, reduce monthly payments, or change loan terms. However, refinancing federal student loans into a private loan means forfeiting federal benefits like IDR plans, deferment, forbearance, and loan forgiveness programs. Carefully weigh the pros and cons before considering this option.

By diligently tracking your loans, proactively communicating with servicers, and strategically planning your repayment, you can transform what might seem like an overwhelming burden into a manageable financial responsibility. Taking the time to find and organize your student loans today is an investment in your financial peace of mind for tomorrow.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.