Applying for a mortgage is often one of the most significant financial undertakings in an individual’s life. It’s the gateway to homeownership, a tangible asset that represents stability, an investment, and often, the realization of a lifelong dream. However, the process can seem daunting, riddled with complex terminology, extensive documentation requirements, and numerous decision points. This comprehensive guide aims to demystify the mortgage application journey, providing a clear, step-by-step roadmap for prospective homeowners. By understanding each phase, from initial preparation to final closing, you can approach this critical process with confidence and clarity, ensuring a smoother path to securing the financing for your dream home.

Preparing for Your Mortgage Application Journey

The foundation of a successful mortgage application lies in meticulous preparation. Before you even speak to a lender, taking the time to assess your financial standing and gather necessary information can significantly streamline the entire process and improve your chances of approval on favorable terms.

Assessing Your Financial Readiness

Before diving into the application process, an honest and thorough self-assessment of your financial health is paramount. This involves scrutinizing your income, expenses, savings, and existing debts. Lenders primarily assess your ability to repay the loan, and this readiness check allows you to view yourself through their lens. Start by calculating your debt-to-income (DTI) ratio, a critical metric lenders use. This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI ratio generally signals less risk to lenders. Furthermore, assess your down payment capacity. While many conventional loans require a minimum of 3-5%, a larger down payment can reduce your loan amount, lower your monthly payments, and potentially qualify you for better interest rates, often eliminating the need for private mortgage insurance (PMI). Having a robust emergency fund – typically three to six months’ worth of living expenses – beyond your down payment and closing costs is also advisable, demonstrating financial prudence and resilience. This preparation also includes understanding what you can truly afford, not just what a lender might pre-approve you for. Factor in potential property taxes, homeowners insurance, and maintenance costs in addition to your principal and interest payments.

Gathering Essential Documents

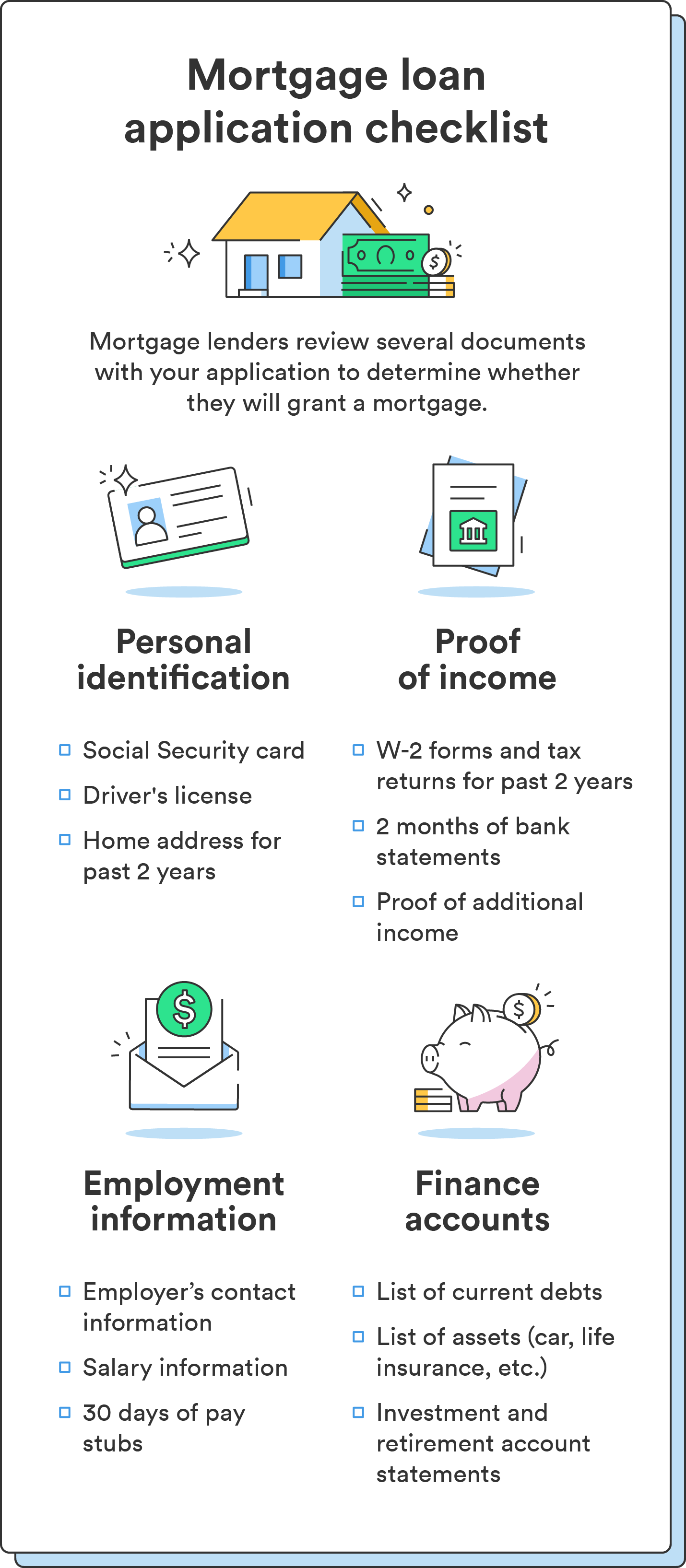

The mortgage application process is document-intensive. Proactively collecting and organizing these critical papers will save you considerable time and reduce stress during the application phase. Lenders require a comprehensive overview of your financial history to verify your identity, income, assets, and debts. Key documents typically include:

- Proof of Income: Recent pay stubs (usually for the last 30-60 days), W-2 forms (for the past two years), and federal tax returns (for the past two years). If you are self-employed, you’ll need two years of personal and business tax returns, along with profit and loss statements.

- Proof of Assets: Bank statements (checking and savings accounts for the past two to three months), investment account statements, and documentation for any other significant assets that could be used for the down payment or reserves.

- Proof of Debts: Statements for all outstanding loans, including credit cards, auto loans, student loans, and any other mortgages.

- Personal Identification: Government-issued photo ID (driver’s license or passport) and Social Security card.

- Rental History (if applicable): Proof of timely rent payments, often via canceled checks or landlord contact information.

Having these documents ready in an organized fashion not only speeds up the process but also presents you as a responsible and prepared borrower.

Understanding Credit Scores and Reports

Your credit score and credit report are central to your mortgage application. Lenders use them to evaluate your creditworthiness, determining your eligibility for a loan and influencing the interest rate you’ll be offered. A higher credit score signals a lower risk to lenders, typically resulting in more favorable loan terms. Before applying, obtain a copy of your credit report from all three major credit bureaus (Equifax, Experian, and TransUnion) via AnnualCreditReport.com. Review them meticulously for any inaccuracies or discrepancies. If you find errors, dispute them immediately, as correcting them can significantly improve your score. Understand the factors that influence your score: payment history, amounts owed, length of credit history, new credit, and credit mix. If your score is lower than desired, focus on paying down high-interest debt, making all payments on time, and avoiding opening new credit accounts in the months leading up to your mortgage application. A good credit score can literally save you thousands of dollars over the life of your loan.

Understanding Mortgage Types and Lenders

With your financial house in order, the next crucial step is to understand the landscape of mortgage products available and identify the right financial partner for your needs. The choices here can significantly impact your monthly payments, long-term costs, and overall financial flexibility.

Exploring Different Mortgage Products

The mortgage market offers a variety of loan products, each designed to meet different borrower needs and financial situations. Understanding these options is key to selecting the one that best suits you.

- Conventional Loans: These are not insured or guaranteed by the government. They often require a good credit score and a down payment (typically 3-20%). If your down payment is less than 20%, you will likely need to pay for Private Mortgage Insurance (PMI). They offer both fixed-rate and adjustable-rate options.

- FHA Loans: Insured by the Federal Housing Administration, these loans are popular among first-time homebuyers or those with lower credit scores. They allow for a lower down payment (as low as 3.5%) and have more lenient credit requirements, but they require mortgage insurance premiums (MIP) for the life of the loan or until certain conditions are met.

- VA Loans: Guaranteed by the U.S. Department of Veterans Affairs, these loans are available to eligible service members, veterans, and surviving spouses. They offer significant benefits, including no down payment requirements and no private mortgage insurance.

- USDA Loans: Backed by the U.S. Department of Agriculture, these loans are for low-to-moderate-income buyers in eligible rural areas. They also offer no down payment options.

- Fixed-Rate Mortgages: The interest rate remains the same for the entire loan term (e.g., 15-year or 30-year), providing predictable monthly payments.

- Adjustable-Rate Mortgages (ARMs): The interest rate is fixed for an initial period (e.g., 3, 5, 7, or 10 years) and then adjusts periodically based on market indices. ARMs can offer lower initial payments but carry the risk of higher payments later if rates rise.

Each product has its own eligibility criteria, benefits, and drawbacks, making a thorough comparison essential.

Choosing the Right Lender for Your Needs

Selecting the right lender is as important as choosing the right loan. Lenders can vary significantly in their rates, fees, customer service, and the types of loan products they specialize in.

- Banks: Traditional banks often offer a full range of financial services and may provide relationship discounts if you have other accounts with them.

- Credit Unions: Member-owned and non-profit, credit unions often offer competitive rates and personalized service.

- Online Lenders: These lenders typically have lower overhead costs, which can translate into competitive rates and a streamlined digital application process.

- Mortgage Brokers: Brokers act as intermediaries, working with multiple lenders to find the best loan product and terms for your specific situation. They can be particularly useful if you have a complex financial profile or are looking for specialized loans.

When choosing, compare interest rates, origination fees, closing costs, and customer reviews. Don’t hesitate to get quotes from several different lenders or work with a reputable mortgage broker to ensure you’re getting the best possible deal. Transparency in their fee structure and clear communication are key indicators of a good lender.

The Role of Mortgage Brokers

Mortgage brokers play a unique and often beneficial role in the application process. Unlike direct lenders (banks, credit unions, online lenders) who offer their own proprietary products, brokers act as independent agents. They have access to a wide array of loan programs from various wholesale lenders, essentially serving as a marketplace for mortgages. This allows them to shop around on your behalf, potentially finding more competitive rates or more flexible terms than you might find on your own, especially if you have a less-than-perfect credit history or unique financial circumstances. They can simplify the application process by acting as a single point of contact, helping you navigate paperwork and understanding complex loan jargon. However, it’s important to understand how they are compensated (typically by the lender or through a borrower-paid fee) and ensure their interests align with yours.

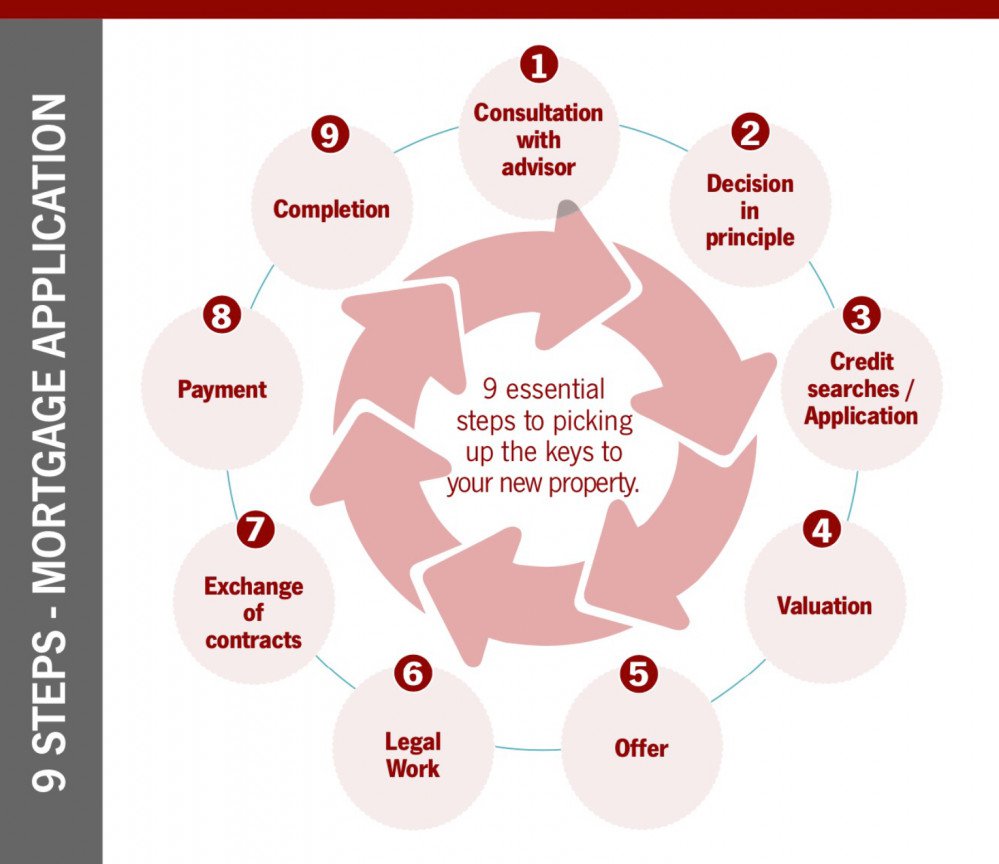

The Application Process: Step-by-Step

Once you’ve prepared your finances and decided on a loan type and lender, you’re ready to embark on the formal application process. This sequence typically begins with pre-approval and culminates in the submission of your full application.

Pre-Approval: Your First Critical Step

Obtaining a mortgage pre-approval is arguably the most crucial initial step in the home-buying journey. It provides a realistic estimate of how much a lender is willing to lend you, based on a preliminary review of your credit, income, and assets. A pre-approval letter is not a guarantee of a loan, but it serves several vital purposes:

- Budget Clarity: It helps you understand your realistic buying power, allowing you to focus your home search on properties within your affordability range.

- Credibility with Sellers: In a competitive real estate market, a pre-approval letter signals to sellers and real estate agents that you are a serious and qualified buyer, giving your offers more weight.

- Identifies Potential Issues Early: The pre-approval process can uncover any credit report inaccuracies or financial issues that need to be addressed before a formal application.

To get pre-approved, you’ll typically provide your social security number (for a credit check), income documentation, and asset information. This initial review gives you a conditional commitment for a loan amount and an estimated interest rate.

Submitting Your Formal Application

After you’ve had an offer accepted on a home, the pre-approval transforms into a full mortgage application. This stage involves providing all the documents you gathered earlier (proof of income, assets, debts, etc.) to your chosen lender. You will complete a detailed Uniform Residential Loan Application (Form 1003 in the U.S.), which is a comprehensive financial disclosure. This form asks for extensive information about your personal history, employment, income, assets, liabilities, and details about the property you intend to purchase. Be prepared to be thorough and accurate, as any discrepancies can cause delays or even rejection later in the process. At this point, you’ll also likely lock in your interest rate, which protects you from market fluctuations during the underwriting period.

Disclosures and Initial Reviews

Upon submitting your formal application, lenders are legally required to provide you with several important disclosures within a few business days. These documents are designed to ensure transparency and inform you about the terms of your loan. Key disclosures include:

- Loan Estimate (LE): This critical document details the estimated interest rate, monthly payment, and total closing costs for the loan. It allows you to compare offers from different lenders and understand the total cost of the mortgage.

- Initial Escrow Statement: This estimates the amount of property taxes and homeowners insurance that will be held in an escrow account.

- Truth-in-Lending Disclosures: These provide information about the total cost of the loan, including the Annual Percentage Rate (APR).

During this initial review period, the lender’s processing team will review all submitted documents for completeness and accuracy, often reaching out for clarification or additional information. Responding promptly to these requests is crucial to keeping your application on track.

Navigating the Underwriting and Closing Phases

With your application submitted and initial disclosures reviewed, the process moves into the critical underwriting phase, where the lender conducts a deep dive into your financial profile and the property itself. This is followed by the final steps leading up to closing.

The Underwriting Deep Dive

Underwriting is the heart of the mortgage approval process. During this stage, a professional underwriter meticulously assesses your creditworthiness, the property’s value, and the overall risk associated with lending to you. They verify all the information you provided in your application and supporting documents. This includes:

- Income Verification: Confirming employment history, salary, and stability of income.

- Asset Verification: Ensuring funds for the down payment and closing costs are legitimately sourced and readily available.

- Debt-to-Income Ratio Analysis: A thorough calculation to ensure you can comfortably manage your new mortgage payments alongside existing debts.

- Credit History Review: Beyond the score, underwriters look for patterns of responsible borrowing and any potential red flags.

The underwriter may request additional documentation or explanations for unusual transactions or employment gaps. This back-and-forth communication is common, so prompt and clear responses are essential. The goal is to ensure that you meet all the lender’s and loan program’s criteria.

Appraisal and Inspection: Protecting Your Investment

Simultaneously with underwriting your financial profile, the property you intend to purchase undergoes its own scrutiny.

- Appraisal: A licensed appraiser will evaluate the home’s market value. This is a crucial step for the lender, as they want to ensure the loan amount does not exceed the property’s actual worth. The appraisal protects the lender’s investment and helps ensure you aren’t overpaying for the home. If the appraisal comes in lower than the purchase price, you may need to renegotiate with the seller or bring more cash to closing.

- Home Inspection: While not strictly required by lenders, a professional home inspection is highly recommended for buyers. An inspector thoroughly examines the property’s condition, identifying any structural issues, needed repairs, or safety hazards. This empowers you to negotiate repairs with the seller or, if significant issues arise, potentially back out of the purchase agreement (if your contract allows).

These steps protect both you and the lender by ensuring the property is sound and accurately valued.

Preparing for Closing Day

Once underwriting is complete and all conditions are satisfied, you’ll receive a “clear to close” notification. This means your loan has been approved! The final stage involves preparing for the closing day, which is when the ownership of the property legally transfers to you, and the mortgage loan is finalized. A few days before closing, you will receive a Closing Disclosure (CD). This is a final statement of all loan terms, closing costs, and cash needed at closing. It’s imperative to compare this CD against your initial Loan Estimate to ensure there are no unexpected fees or significant changes. If you spot any discrepancies, address them immediately with your lender or real estate agent. You’ll need to arrange for a certified check or wire transfer for the remaining down payment and closing costs. Reviewing all documents carefully and understanding what you are signing at the closing table is critical.

Post-Approval: What to Expect and Next Steps

Congratulations, your mortgage is approved, and you’ve closed on your new home! While the application journey concludes, a new chapter of responsible homeownership begins.

Your Mortgage is Approved: Now What?

After the closing documents are signed and the funds disbursed, you are officially a homeowner. Your first mortgage payment will typically be due one month and a few days after your closing date. Your loan servicer (which might be the same as your original lender or a different company) will send you a welcome packet with all the details regarding your payment schedule, how to make payments, and contact information for customer service. This is also the time to ensure all utilities are transferred into your name and your homeowner’s insurance policy is fully active. Take a moment to celebrate this significant milestone, understanding the responsibilities that come with it.

Managing Your Mortgage Responsibly

Owning a home and managing a mortgage requires ongoing financial discipline. Making your mortgage payments on time, every time, is paramount for maintaining good credit and avoiding late fees. Consider setting up automatic payments to ensure consistency. It’s also wise to understand your loan’s amortization schedule, which shows how your payments are allocated between principal and interest over the loan’s life. Explore options like making extra principal payments, even small ones, as this can significantly reduce the total interest paid and shorten the loan term. Additionally, regularly review your property tax and insurance escrow accounts to ensure they are adequately funded and to understand any adjustments. Staying informed about your mortgage terms and responsibilities is key to long-term financial health.

Refinancing and Future Considerations

Life circumstances and market conditions can change, making refinancing an option to consider down the line. Refinancing involves replacing your existing mortgage with a new one, often to secure a lower interest rate, change the loan term, or convert an adjustable-rate mortgage to a fixed-rate one. It can also be a way to tap into your home equity (cash-out refinance). However, refinancing involves closing costs, so it’s crucial to calculate whether the long-term savings outweigh these upfront expenses. As your financial situation evolves, continue to monitor market interest rates and assess if a refinance could benefit you. Regular financial check-ups, even years after securing your initial mortgage, can ensure your home financing remains optimized for your goals.

In conclusion, applying for a mortgage is a multi-faceted process that demands preparation, diligence, and a clear understanding of the financial landscape. By meticulously preparing your finances, understanding the various loan products and lenders, navigating the application and underwriting stages with care, and responsibly managing your mortgage post-approval, you can successfully achieve homeownership and lay a strong foundation for your financial future. While challenging, the journey culminates in one of life’s most rewarding investments.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.