Navigating the landscape of homeownership often begins with understanding the various financing options available. For many prospective homebuyers, especially those with lower credit scores or limited down payment funds, Federal Housing Administration (FHA) loans represent a vital pathway. The FHA, part of the U.S. Department of Housing and Urban Development (HUD), insures these loans, making them less risky for lenders and thus more accessible to a broader range of borrowers. However, the interest rates associated with FHA loans, like all mortgage rates, are dynamic, influenced by a complex interplay of economic forces. Understanding “what are FHA rates today” is not merely about checking a number; it’s about grasping the underlying factors that drive these rates, their implications for affordability, and how they fit into your overall financial strategy for buying a home.

For many first-time homebuyers or those with less-than-perfect credit, FHA loans offer an invaluable opportunity to achieve homeownership. These government-insured mortgages come with more lenient qualification requirements compared to conventional loans, making them a crucial tool for expanding access to housing. However, the exact interest rate you’ll secure on an FHA loan isn’t static. It fluctuates daily, even hourly, based on a myriad of economic indicators, Federal Reserve policies, and global market sentiments. This article aims to demystify FHA rates, providing a comprehensive guide to understanding what they are, what influences them, how they compare to other loan types, and crucially, how you can navigate the market to secure the best possible rate for your home purchase.

Understanding FHA Loans and Their Appeal

Before delving into the specifics of FHA rates, it’s essential to grasp the fundamental nature of FHA loans themselves. These loans are not issued by the FHA directly but are provided by FHA-approved lenders. The FHA’s role is to insure these mortgages, protecting lenders against potential losses if a borrower defaults. This insurance is what allows lenders to offer more favorable terms to borrowers who might not qualify for conventional financing.

The Core Purpose of FHA Loans

The primary objective of the FHA loan program, established during the Great Depression, was to stimulate the housing market and make homeownership more accessible. It achieves this by providing mortgage insurance that mitigates the risk for lenders, enabling them to offer loans with lower down payment requirements and more flexible credit score criteria. This structure has made FHA loans a cornerstone of affordable housing initiatives for nearly a century. They are designed to serve individuals and families who may struggle to meet the more stringent requirements of conventional mortgages, ensuring that the dream of homeownership remains within reach for a broader segment of the population.

Who Benefits Most from FHA Loans?

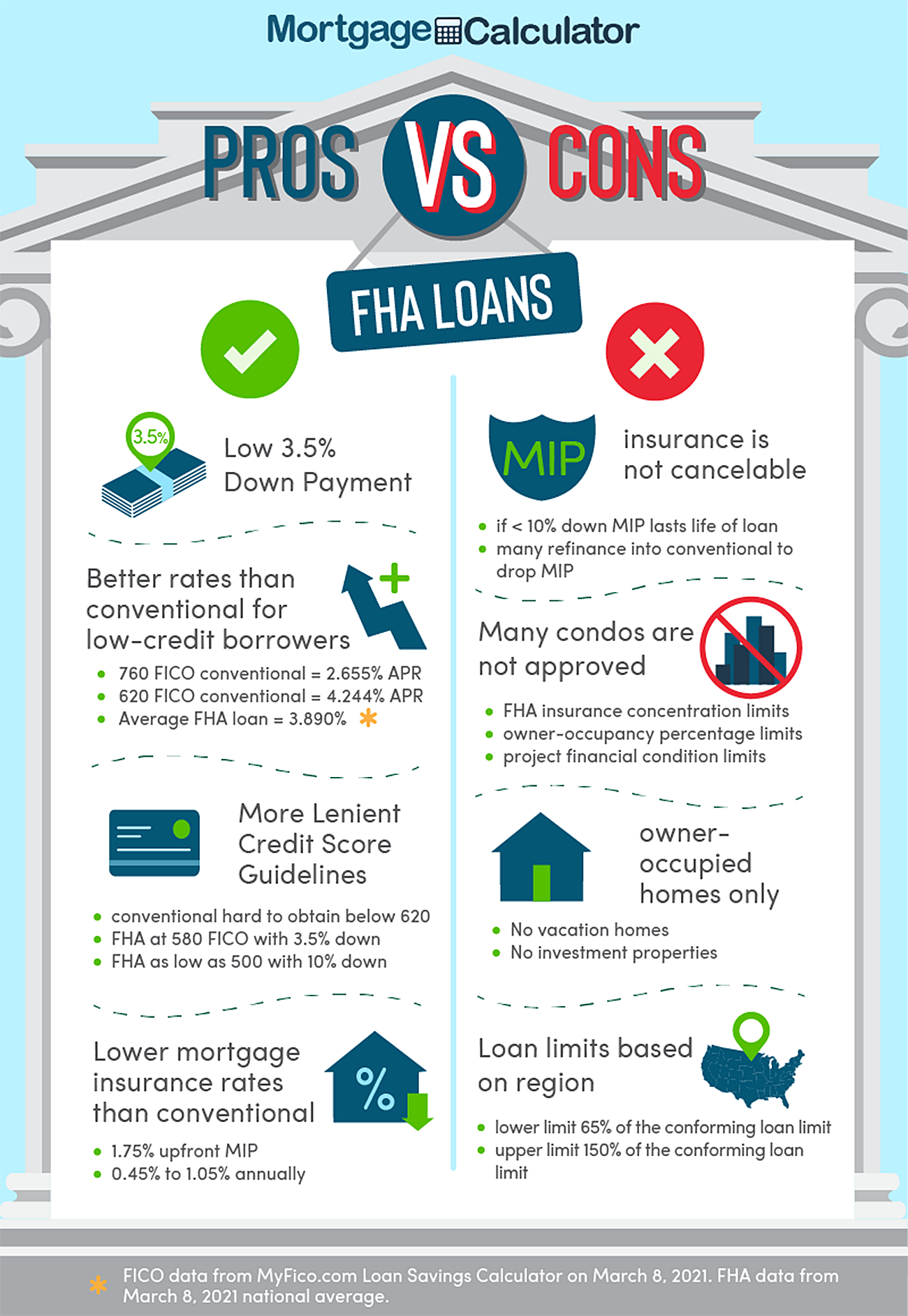

FHA loans are particularly beneficial for several key demographics. First and foremost are first-time homebuyers who may not have accumulated a substantial down payment. With FHA loans, it’s possible to qualify with as little as 3.5% down, a significant advantage over many conventional loans that often require 5% to 20%. Secondly, borrowers with less-than-perfect credit scores find FHA loans more forgiving. While conventional lenders typically demand FICO scores of 620 or higher, FHA guidelines can allow for scores as low as 580 (with the 3.5% down payment) or even lower (with a 10% down payment), though individual lenders may set their own higher minimums. Lastly, individuals with higher debt-to-income (DTI) ratios may also find FHA loans more accommodating, as the program often allows for slightly higher DTI limits than conventional loans, provided other compensating factors are present.

Key Distinctions from Conventional Loans

The differences between FHA and conventional loans extend beyond down payment and credit score requirements. One of the most significant distinctions is mortgage insurance. While conventional loans may require private mortgage insurance (PMI) if the down payment is less than 20%, FHA loans mandate both an upfront mortgage insurance premium (UFMIP) and an annual mortgage insurance premium (MIP) regardless of the down payment amount. MIP is paid monthly and typically lasts for the entire loan term for most FHA loans, distinguishing it from PMI, which can often be canceled once sufficient equity is built. Additionally, FHA loans have specific property requirements, meaning homes must meet certain safety, security, and structural soundness standards verified by an FHA appraisal.

Decoding Today’s FHA Interest Rates

Understanding “what are FHA rates today” requires a grasp of the broader mortgage market and the specific factors that dictate interest rate movements. Unlike a fixed price tag, mortgage rates are fluid, reacting to global and domestic economic shifts.

The Dynamics of Mortgage Rates

Mortgage rates, including those for FHA loans, are not set by any single entity. Instead, they are influenced by the bond market, specifically the yields on mortgage-backed securities (MBS). When MBS yields rise, mortgage rates generally follow suit, and vice versa. These yields react to investor sentiment, which in turn is driven by economic forecasts, inflation expectations, and monetary policy. Lenders then add their own margin to these base rates to cover operational costs, profit, and risk assessment for individual borrowers.

Factors Directly Influencing FHA Rates

Several key economic and policy factors exert significant influence over FHA rates:

- Economic Indicators (Inflation, Employment, GDP): Strong economic growth, low unemployment, and rising inflation often push mortgage rates higher. When the economy is robust, investors may shift funds from the relatively safe bond market to more lucrative investments, causing bond prices to fall and yields (and thus mortgage rates) to rise. Conversely, signs of economic weakness or recession tend to push rates down as investors flock to the safety of bonds. Inflation is a particularly critical factor; if lenders expect inflation to erode the value of future loan repayments, they will demand higher interest rates to compensate for that loss.

- Federal Reserve Policy: While the Federal Reserve does not directly set mortgage rates, its actions have a profound indirect impact. The Fed’s decisions on the federal funds rate, quantitative easing or tightening, and its overall commentary on economic outlook significantly influence the broader interest rate environment. When the Fed raises its benchmark rates to combat inflation, it typically leads to an increase in borrowing costs across the board, including mortgage rates.

- Market Competition and Lender Margins: The competitive landscape among mortgage lenders also plays a role. In a highly competitive market, lenders might slightly reduce their profit margins to attract borrowers, leading to marginally lower rates. Conversely, during periods of high demand or uncertainty, lenders might increase their margins. Furthermore, a lender’s own operational costs and risk appetite will influence the rates they offer.

- Global Events: Geopolitical events, international trade disputes, and global economic shifts can create uncertainty, causing investors to seek safe-haven assets like U.S. Treasury bonds. This increased demand for bonds can drive their prices up and yields down, potentially leading to lower mortgage rates. Conversely, a sudden global crisis that threatens stability could cause a flight to quality and impact rates in unpredictable ways.

How FHA Rates Compare to Conventional Rates

Historically, FHA loan interest rates have often been comparable to, or sometimes slightly lower than, conventional loan rates. This might seem counterintuitive given the FHA’s more lenient underwriting standards. However, the government insurance provided by the FHA effectively lowers the risk for lenders, allowing them to offer competitive interest rates. The key difference in overall cost, as mentioned earlier, often lies in the mortgage insurance. While FHA rates themselves might be attractive, the mandatory upfront and annual MIP can make the total monthly payment higher than a conventional loan for a borrower with excellent credit and a 20% down payment who can avoid PMI entirely. For borrowers with less than ideal credit or a small down payment, the competitive FHA rate combined with the accessibility of the loan program often makes it the more affordable and viable option.

The Full Cost of an FHA Loan: Beyond the Interest Rate

Understanding “what are FHA rates today” is just one piece of the puzzle. To accurately assess the affordability of an FHA loan, borrowers must consider all associated costs, not just the advertised interest rate.

Mortgage Insurance Premium (MIP): Upfront and Annual

The most significant additional cost unique to FHA loans is the Mortgage Insurance Premium (MIP). This comes in two forms:

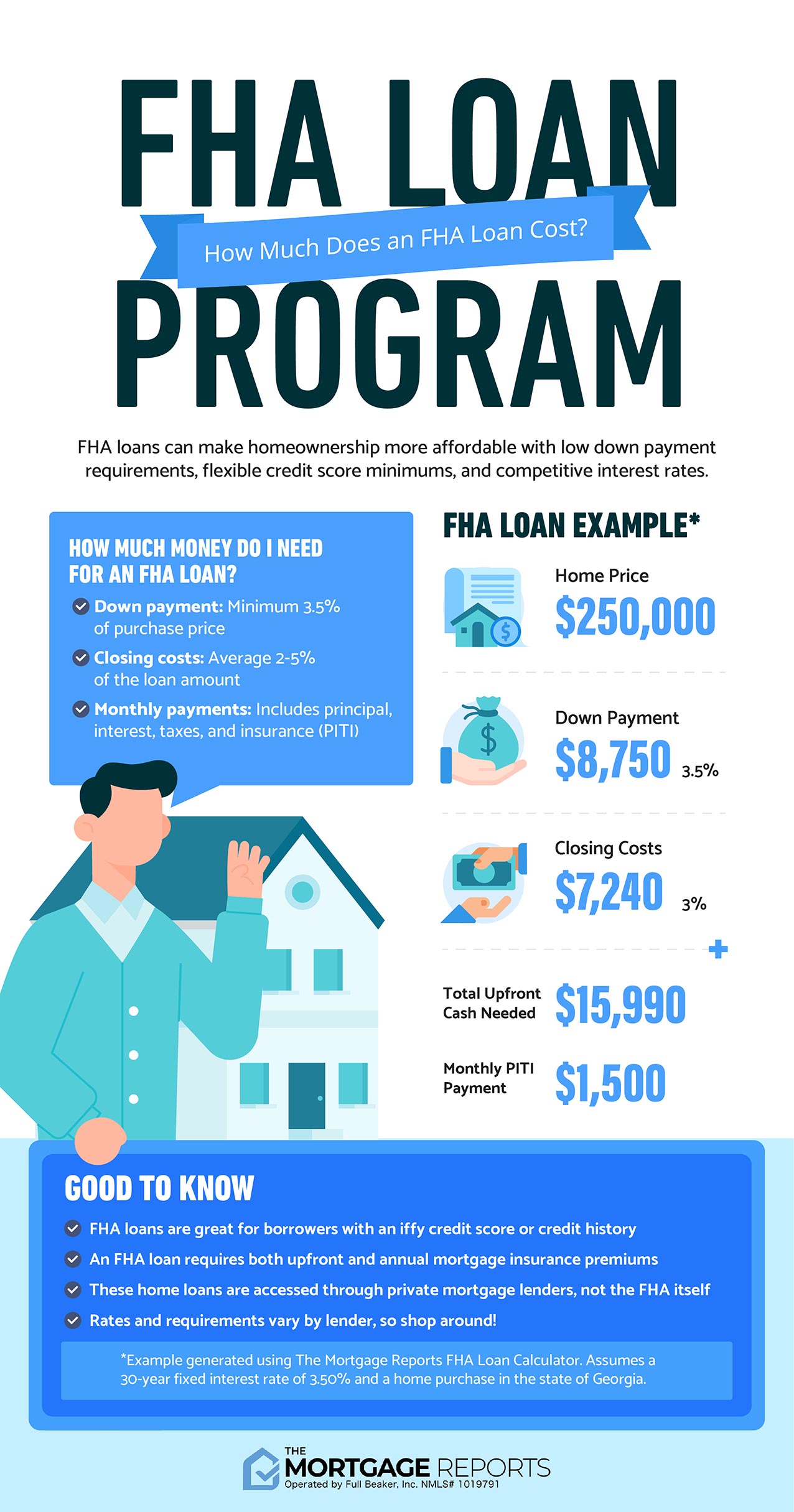

- Upfront Mortgage Insurance Premium (UFMIP): This is a one-time fee equal to 1.75% of the loan amount, regardless of your down payment. It’s typically paid at closing, though it can be financed into the loan, increasing your loan amount and subsequent interest charges. For example, on a $300,000 loan, the UFMIP would be $5,250.

- Annual Mortgage Insurance Premium (MIP): This is an ongoing premium paid monthly as part of your mortgage payment. The exact percentage varies but is typically between 0.45% and 1.05% of the outstanding loan balance annually. For most FHA loans with a down payment less than 10%, this annual MIP is charged for the entire loan term, regardless of how much equity you build. If your down payment is 10% or more, the MIP typically lasts for 11 years. This continuous cost significantly impacts the total monthly housing expense and is a critical factor when comparing FHA loans to conventional mortgages.

Closing Costs and Other Fees

Like all mortgage loans, FHA loans come with various closing costs. These are fees charged by the lender and third parties for services rendered in processing your loan and transferring property ownership. Common closing costs include:

- Origination Fees: Charged by the lender for processing the loan.

- Appraisal Fees: To determine the home’s value and ensure it meets FHA standards.

- Title Insurance and Escrow Fees: For ensuring clear ownership and managing the closing process.

- Recording Fees: For officially registering the property transfer with the local government.

- Attorney Fees: If applicable in your state.

- Prepaid Expenses: Such as property taxes and homeowner’s insurance premiums for the upcoming period.

These costs can typically range from 2% to 5% of the loan amount and are paid at closing. While the FHA has rules regarding what a seller can contribute to a buyer’s closing costs (up to 6% of the sales price), buyers should still budget for these significant expenses.

Calculating Your True Monthly Payment

To truly understand the affordability of an FHA loan, you must calculate your total monthly housing expense. This includes:

- Principal and Interest (P&I): Based on your loan amount and the FHA interest rate you secure.

- Annual Mortgage Insurance Premium (MIP): Divided by 12 and added to your monthly payment.

- Property Taxes: An estimated monthly amount, often held in an escrow account.

- Homeowner’s Insurance (HOI): An estimated monthly amount, also often held in escrow.

- Homeowners Association (HOA) Dues: If applicable to the property.

By summing these components, you get a realistic picture of your monthly financial commitment, allowing you to budget effectively and ensure the home is genuinely affordable.

Eligibility and Securing the Best FHA Rate

While FHA loans are designed for broader accessibility, there are still specific criteria borrowers must meet. Moreover, simply qualifying isn’t enough; strategic steps can help you secure the most competitive FHA rate available today.

FHA Loan Requirements: Credit Score, Down Payment, DTI

The FHA sets minimum requirements, but individual lenders often impose slightly stricter overlays, known as “lender overlays.” Generally, FHA requirements include:

- Credit Score: A FICO score of 580 or higher typically qualifies for the minimum 3.5% down payment. Borrowers with scores between 500 and 579 may still qualify but will need a larger down payment (at least 10%). Below 500, FHA loans are generally not an option.

- Down Payment: As mentioned, 3.5% for credit scores 580+, or 10% for scores 500-579. These funds can come from savings, gifts, or approved down payment assistance programs.

- Debt-to-Income (DTI) Ratio: This measures your gross monthly income against your monthly debt payments. The FHA generally looks for a front-end ratio (housing expenses only) of no more than 31% and a back-end ratio (total debt, including housing) of no more than 43%. However, with strong compensating factors (e.g., significant cash reserves, higher credit score), DTI ratios up to 50% or even higher may be approved.

- Stable Employment History: Lenders typically look for at least two years of consistent employment in the same line of work.

- Property Standards: The home must meet FHA appraisal guidelines, ensuring it’s safe, sound, and secure.

Strategies for Improving Your Rate Eligibility

Even if you meet the minimum FHA requirements, several actions can improve your chances of securing a lower interest rate:

- Improve Your Credit Score: A higher credit score signals less risk to lenders. Pay bills on time, reduce credit card balances, and avoid opening new credit accounts before applying for a mortgage. Even a slight improvement can lead to better rate offers.

- Increase Your Down Payment: While FHA allows low down payments, putting more money down can reduce your loan amount, potentially making your application more attractive to lenders, and in some cases, might even slightly influence the rate offered.

- Reduce Your Debt-to-Income Ratio: Paying down existing debts before applying can significantly lower your DTI, making you a more financially stable candidate in the eyes of lenders.

- Build Cash Reserves: Having a substantial savings buffer beyond your down payment and closing costs provides a financial cushion, which lenders view favorably.

The Importance of Shopping Around for Lenders

This is perhaps the most critical step in securing the best FHA rate. FHA rates can vary significantly between different lenders on any given day, sometimes by as much as a quarter or even half a percentage point. This difference, though seemingly small, can translate into thousands of dollars over the life of a 30-year mortgage.

- Get Quotes from Multiple Lenders: Contact at least three to five different FHA-approved lenders, including national banks, local banks, credit unions, and mortgage brokers.

- Compare Loan Estimates: Once you apply, lenders are required to provide a Loan Estimate within three business days. Carefully compare these documents, focusing not only on the interest rate but also on the annual percentage rate (APR), which reflects the total cost of the loan including some fees. Also, scrutinize the closing costs and any lender fees.

- Negotiate: Don’t be afraid to use a competitive offer from one lender to see if another can match or beat it.

Locking In Your Rate

Once you find a rate you’re comfortable with, discuss with your lender the option of “locking in” your interest rate. A rate lock guarantees that your interest rate will not change between the time of your lock and your closing, provided the closing occurs within the agreed-upon timeframe (typically 30 to 60 days). This protects you from potential rate increases during the loan processing period. Be aware of any fees associated with rate locks, especially for extended periods.

Navigating the FHA Market: Practical Advice for Homebuyers

The journey to homeownership with an FHA loan involves careful planning and continuous awareness of the market.

When is an FHA Loan the Right Choice?

An FHA loan is typically an excellent option if you:

- Are a first-time homebuyer with limited savings for a large down payment.

- Have a good but not excellent credit score (e.g., in the 580-700 range).

- Need more flexible debt-to-income ratio guidelines.

- Are struggling to qualify for a conventional loan due to stricter requirements.

- Are comfortable with the upfront and annual mortgage insurance premiums in exchange for accessibility.

It’s crucial to weigh the benefits of accessibility against the costs, especially the long-term MIP. For some, after building sufficient equity, refinancing from an FHA loan to a conventional loan might be a strategy to eliminate mortgage insurance.

Preparing Your Finances for an FHA Loan

Beyond improving your credit score and DTI, ensure all your financial documents are organized and readily available. This includes pay stubs, W-2s, bank statements, tax returns, and any other income or asset verification. Having these prepared can streamline the application process and prevent delays. Also, save for closing costs in addition to your down payment, as these are separate and significant expenses.

Staying Informed in a Volatile Market

Mortgage rates are influenced by a dynamic global economy. Keep an eye on economic news, particularly reports on inflation, employment, and the Federal Reserve’s monetary policy announcements. While you can’t predict rate movements with certainty, staying informed can help you understand the prevailing trends and make timely decisions about when to lock in a rate. Consult with a knowledgeable mortgage professional who can provide up-to-the-minute information and personalized advice.

Conclusion

Understanding “what are FHA rates today” involves much more than a simple Google search. It requires a comprehensive understanding of how FHA loans work, the economic forces that shape interest rates, and all the associated costs that contribute to your overall monthly payment. While FHA loans offer an invaluable pathway to homeownership for many, particularly those with less conventional financial profiles, securing the best possible rate and terms demands diligence, financial preparation, and savvy comparison shopping. By taking a proactive and informed approach, prospective homebuyers can effectively leverage the benefits of FHA financing to achieve their dreams of owning a home. Always seek advice from qualified financial and mortgage professionals to tailor strategies to your unique circumstances.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.