The quest for the “current” 30-year mortgage interest rate is a perpetual journey for homebuyers and homeowners alike. It’s a number that holds immense power, dictating the affordability of a dream home, the potential savings from a refinance, and the overall trajectory of personal wealth. Yet, the answer is rarely a simple, singular figure. Instead, it’s a dynamic, multifaceted entity, influenced by a complex interplay of global economic forces, domestic financial policies, and individual borrower profiles. Understanding this intricate ecosystem is paramount for anyone looking to navigate the often-turbulent waters of real estate finance. This article will delve into the mechanisms that shape the 30-year fixed mortgage rate, providing insights into its fluctuations, its impact, and strategies for securing the most favorable terms.

Understanding the Dynamics of Mortgage Rates

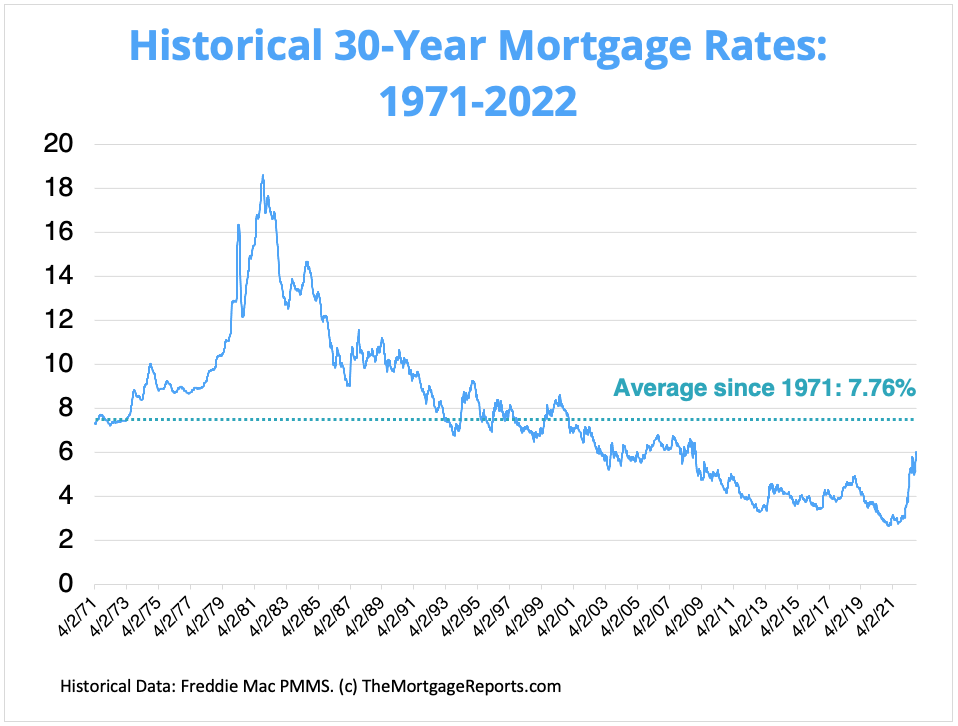

To truly grasp what constitutes the “current” 30-year mortgage interest rate, one must first appreciate the myriad forces that constantly sculpt it. It’s not a static number published daily by a central authority, but rather an average derived from various lenders, each with their own risk assessments and profit margins, all operating within a broader economic framework.

The Elusive “Current” Rate

When searching for the “current” rate, it’s crucial to understand that the figure you see online, in financial news, or even from an initial lender inquiry is often a snapshot or an estimate. Mortgage rates are quoted daily, sometimes hourly, and are subject to change without notice based on market conditions throughout the day. Furthermore, the rate offered to any individual borrower is highly personalized. Factors such as the borrower’s credit score, down payment amount, debt-to-income ratio, property type, location, and the specific loan product will all influence the final rate. Therefore, the “current rate” is best thought of as a range, with the best rates reserved for the most creditworthy borrowers and ideal loan scenarios. To get an accurate current rate, one must engage directly with a lender and apply for a specific loan.

Key Economic Drivers

Several macro-economic indicators exert significant influence over mortgage rates. One of the most prominent is inflation. When inflation is high or expected to rise, lenders demand higher interest rates to compensate for the erosion of the dollar’s purchasing power over the 30-year term of the loan. Conversely, low inflation can lead to lower rates. Employment figures, GDP growth, and consumer confidence also play roles, signaling the overall health of the economy. A robust economy might suggest higher demand for credit, potentially pushing rates up, while a slowing economy could see rates drop as investors seek safer havens like mortgage-backed securities. The global economic landscape also matters, as international events and capital flows can indirectly affect domestic bond markets and, subsequently, mortgage rates.

The Federal Reserve’s Influence

While the Federal Reserve does not directly set mortgage rates, its monetary policy decisions have a profound indirect impact. The Fed’s primary tool is the federal funds rate, the target rate for overnight lending between banks. Changes to the federal funds rate ripple through the financial system, affecting other short-term interest rates. More significantly for mortgages, the Fed’s stance on quantitative easing (QE) or quantitative tightening (QT) directly influences the market for mortgage-backed securities (MBS). When the Fed buys MBS (QE), it increases demand, pushing prices up and yields (which inversely relate to rates) down. When it sells MBS (QT), it has the opposite effect. The Fed’s forward guidance and public statements regarding its outlook on inflation and economic growth also guide market expectations, which in turn affect long-term rates like those for 30-year mortgages.

Factors Beyond Macroeconomics: Your Personal Impact

While economic tides undeniably shape the broad strokes of mortgage interest rates, an individual’s financial profile and choices play a critical role in determining the specific rate they are offered. These personal factors can lead to significant differences in monthly payments and the total cost of the loan over three decades.

The Power of Your Credit Score

Your credit score is arguably the most significant personal determinant of the mortgage interest rate you’ll receive. Lenders use credit scores (like FICO or VantageScore) as a primary indicator of your creditworthiness and your likelihood of repaying the loan. A higher credit score (typically above 740-760) signals lower risk to lenders, often qualifying you for the most competitive interest rates. Conversely, a lower credit score suggests a higher risk, prompting lenders to charge a higher interest rate to compensate for that elevated risk. It’s not uncommon for a borrower with an excellent credit score to receive an interest rate that is a full percentage point or more lower than someone with a fair credit score, leading to tens of thousands of dollars in savings over the life of a 30-year mortgage. Before applying for a mortgage, reviewing and improving your credit score is a crucial step.

Loan-to-Value Ratio and Down Payment

The loan-to-value (LTV) ratio is another critical factor. It represents the amount of your mortgage compared to the appraised value of the home, expressed as a percentage. A lower LTV ratio means you’ve made a larger down payment, signaling to the lender that you have more equity in the property from the outset and are less likely to default. Lenders typically view a lower LTV as less risky, which can translate into a better interest rate. For instance, a 20% down payment (resulting in an 80% LTV) often secures a more favorable rate than a 5% down payment (95% LTV). Beyond the interest rate, a down payment of 20% or more also typically allows you to avoid private mortgage insurance (PMI), a costly added expense that further increases your monthly housing costs.

Choosing the Right Loan Type

While the 30-year fixed-rate mortgage is the most popular choice, variations in loan types can also affect the interest rate offered. Conventional loans, which are not insured or guaranteed by the government, typically require stronger credit and higher down payments for the best rates. Government-backed loans, such as FHA, VA, and USDA loans, have different eligibility requirements and often cater to specific borrower groups. FHA loans, for example, are popular for first-time homebuyers or those with lower credit scores, allowing for down payments as low as 3.5%. While they can make homeownership more accessible, FHA loans come with mandatory mortgage insurance premiums (MIP) for the life of the loan, which adds to the overall cost, even if the quoted interest rate seems competitive. VA loans, for eligible veterans and service members, often boast some of the lowest interest rates and require no down payment or PMI, making them exceptionally attractive. Understanding the nuances of each loan type and its implications for interest rates and overall costs is essential for making an informed decision.

Navigating the Mortgage Market: How to Secure Your Best Rate

Armed with an understanding of both macro and personal influences on mortgage rates, the next step is to strategically navigate the market. Securing the “best” rate isn’t just about timing; it’s about meticulous preparation, informed comparison, and tactical decision-making.

The Importance of Shopping Around

One of the most impactful actions a borrower can take is to shop around and compare offers from multiple lenders. Studies consistently show that borrowers who obtain quotes from several lenders tend to secure lower interest rates. The difference between the highest and lowest rates offered for the same borrower on the same day can be substantial, often amounting to hundreds or even thousands of dollars in savings over the loan’s lifetime. Don’t limit your search to just your existing bank; explore credit unions, online lenders, and mortgage brokers who can access a wide range of loan products from various providers. Each lender has different overhead costs, risk appetites, and pricing strategies, leading to variations in the rates and fees they offer. Submitting applications to multiple lenders within a short timeframe (typically 14-45 days, depending on the credit scoring model) will usually only count as a single hard inquiry on your credit report, minimizing the impact on your score.

Deciphering APR vs. Interest Rate

When comparing loan offers, it’s crucial to understand the distinction between the nominal interest rate and the Annual Percentage Rate (APR). The interest rate is simply the cost of borrowing money, expressed as a percentage of the principal. The APR, however, provides a more comprehensive measure of the total cost of the loan over its term, as it includes not only the interest rate but also most of the closing costs and other fees associated with the mortgage (e.g., origination fees, discount points, mortgage insurance premiums). While the interest rate determines your monthly principal and interest payment, the APR gives you a truer picture of the loan’s overall expense. When comparing loan offers, always use the APR for an apples-to-apples comparison, as it reflects the true cost more accurately. A loan with a slightly lower interest rate but a significantly higher APR might actually be more expensive in the long run due to higher fees.

Strategic Rate Locking and Mortgage Points

Once you’ve found a competitive rate, the next step is often to “lock it in.” A mortgage rate lock is a guarantee from the lender that the interest rate offered to you will not change before your closing, provided the loan closes within a specified period (e.g., 30, 45, or 60 days). Rate locks protect you from market fluctuations that could drive rates higher during the loan processing period. However, be aware of the lock period; if your closing is delayed beyond the lock expiration, you may need to pay an extension fee or accept the prevailing market rate.

Another strategic consideration is whether to pay mortgage points, also known as discount points. A point is an upfront fee equal to 1% of the loan amount, paid at closing, in exchange for a lower interest rate. For example, paying one point on a $300,000 loan would cost $3,000 but could reduce your interest rate by a fraction of a percentage point. Whether paying points is worthwhile depends on how long you plan to stay in the home and the specific cost-benefit analysis. If you plan to live in the home for many years, the long-term savings from a lower interest rate might outweigh the upfront cost of the points. Conversely, if you expect to move or refinance within a few years, paying points might not make financial sense.

The Far-Reaching Impact of 30-Year Mortgage Rates

The interest rate on a 30-year mortgage is far more than just a number; it is a pivotal economic lever that profoundly influences personal financial health, housing market dynamics, and broader economic stability. Its movements dictate accessibility to homeownership and shape long-term financial planning.

Monthly Payments and Long-Term Affordability

The most immediate and tangible impact of the 30-year mortgage interest rate is on your monthly mortgage payment. Even a seemingly small change in the interest rate can translate into a significant difference in your payment over three decades. For example, on a $300,000 loan, a difference of just half a percentage point (e.g., 6.0% vs. 6.5%) can alter your monthly payment by approximately $95, adding up to over $34,000 in additional interest paid over the life of the loan. This directly affects a household’s disposable income, budget flexibility, and overall capacity to save or invest. Higher rates can price potential buyers out of the market, particularly in high-cost areas, by pushing monthly payments beyond their affordability thresholds or debt-to-income limits. Conversely, lower rates enhance purchasing power, making homeownership attainable for a wider segment of the population.

Housing Market Trends and Refinancing Opportunities

Beyond individual finances, prevailing mortgage rates act as a critical driver for the entire housing market. When rates are low, demand for homes typically increases, as borrowing becomes more affordable. This often leads to a sellers’ market, characterized by rising home prices, competitive bidding, and quicker sales. Conversely, higher rates tend to cool the market, reducing buyer demand, slowing price appreciation, and potentially increasing inventory.

For existing homeowners, fluctuations in 30-year mortgage rates present significant refinancing opportunities. When rates drop significantly below their current mortgage rate, homeowners can refinance to secure a lower interest rate, thereby reducing their monthly payments, decreasing the total interest paid over time, or even shortening their loan term (e.g., from a 30-year to a 15-year mortgage). Cash-out refinancing, which allows homeowners to tap into their home equity, also becomes more attractive when rates are low, providing funds for home improvements, debt consolidation, or other investments. Monitoring market rates is thus a continuous financial strategy for homeowners, not just prospective buyers.

The Road Ahead: Forecasting Future Rate Movements

Predicting the precise trajectory of 30-year mortgage rates is an inherently challenging endeavor, fraught with uncertainty due to the multitude of global and domestic factors at play. However, understanding expert perspectives and being prepared for market volatility is crucial for financial planning.

Expert Predictions and Market Volatility

Financial institutions, economists, and housing market analysts frequently release forecasts for mortgage rates, often taking into account projections for inflation, economic growth, and Federal Reserve policy. While these predictions offer valuable insights, they are not guarantees. Geopolitical events, unexpected economic data, or shifts in central bank rhetoric can quickly alter the outlook. For instance, an unexpected surge in inflation could prompt the Fed to adopt a more hawkish stance, leading to upward pressure on rates, while signs of an impending recession might encourage the Fed to consider rate cuts, potentially driving mortgage rates down. It is wise for consumers to consult a range of expert opinions rather than relying on a single forecast and to understand that volatility is a constant feature of financial markets.

Adapting to Changing Financial Landscapes

Given the unpredictable nature of mortgage rates, a flexible and informed approach is essential. For those planning to purchase a home, securing pre-approval early can provide a clearer picture of their buying power at a specific rate. Staying in close communication with a mortgage lender and monitoring market trends can help identify opportune moments to lock in a rate. For existing homeowners, regularly reviewing current mortgage rates against their own can highlight potential refinancing advantages. Financial tools and calculators can help assess the break-even point for refinancing or the long-term savings from paying points. Ultimately, success in navigating the mortgage market hinges on proactive engagement, continuous learning, and strategic decision-making, ensuring that one’s financial goals remain aligned with the evolving economic landscape.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.