In the dynamic world of personal finance, few numbers hold as much significance for the average consumer as the current average mortgage rate. It’s a figure that dictates not just the monthly cost of homeownership but also influences broader economic trends, from housing market activity to consumer spending. For prospective homebuyers, current homeowners considering refinancing, or even seasoned investors, understanding the prevailing mortgage landscape is paramount to making informed financial decisions. While specific rates fluctuate daily, even hourly, due to a complex interplay of global and domestic economic factors, understanding the general trend and the underlying forces shaping it provides invaluable insight into one of life’s most significant financial commitments. This article delves into the current state of mortgage rates, explores the mechanisms behind their movements, and offers practical strategies for navigating this ever-evolving financial terrain.

Understanding Current Mortgage Rate Dynamics

The concept of an “average mortgage rate” is often quoted, but its derivation is far from simple. It’s a reflection of multiple economic indicators, market sentiments, and even geopolitical events. To truly grasp what constitutes the average rate at any given moment, one must first understand the fundamental forces that propel these numbers up or down.

Key Factors Influencing Mortgage Rates

Mortgage rates are not set in a vacuum; they are a direct response to a symphony of economic signals. At the forefront is the Federal Reserve’s monetary policy. While the Fed doesn’t directly set mortgage rates, its actions, particularly regarding the federal funds rate, profoundly influence the broader interest rate environment. When the Fed raises its benchmark rate to combat inflation, it typically leads to higher borrowing costs across the board, including mortgages. Conversely, rate cuts often aim to stimulate economic activity by making borrowing cheaper.

Inflation is another critical driver. Lenders charge interest to make a profit and to ensure the real value of their return isn’t eroded by rising prices. If inflation is high, lenders demand higher rates to compensate for the decrease in purchasing power of future repayment dollars. Conversely, low inflation can allow for lower rates.

Economic growth also plays a role. A robust economy often sees higher demand for credit, which can push rates up. However, it can also signal greater stability, which might attract bond investors. The bond market, particularly the yield on the 10-year Treasury note, is a significant barometer for fixed-rate mortgages. Mortgage rates tend to track the 10-year Treasury yield because mortgage-backed securities (MBS), which are bundles of mortgages sold to investors, compete with Treasuries for investor capital. When Treasury yields rise, MBS yields must also rise to remain competitive, leading to higher mortgage rates.

Lastly, housing market demand and supply can have localized impacts. High demand in a specific area could slightly influence lender pricing, though this is less of a national driver.

The Difference Between Fixed and Adjustable Rates

When discussing average mortgage rates, it’s crucial to distinguish between fixed-rate mortgages (FRMs) and adjustable-rate mortgages (ARMs).

Fixed-rate mortgages maintain the same interest rate for the entire life of the loan, typically 15 or 30 years. This offers predictability and stability in monthly payments, making budgeting easier. The “average rate” most commonly cited refers to a 30-year fixed mortgage, as it’s the most popular loan product. While offering security, FRMs might come with a slightly higher initial rate compared to ARMs, especially in certain market conditions, as lenders price in the risk of future interest rate fluctuations.

Adjustable-rate mortgages feature an interest rate that changes periodically after an initial fixed-rate period (e.g., 5/1 ARM, 7/1 ARM). For instance, a 5/1 ARM has a fixed rate for the first five years, after which it adjusts annually based on a chosen index (like SOFR) plus a margin. ARMs can offer lower initial interest rates, which can be attractive for buyers who plan to sell or refinance before the adjustable period begins, or those anticipating higher future income. However, they carry the risk of significantly higher payments if rates rise, making them less predictable. The average rates for ARMs are often lower initially but are subject to caps on how much they can increase in a given period and over the life of the loan.

How Lenders Determine Your Specific Rate

While national averages provide a benchmark, the specific mortgage rate you qualify for is highly personalized. Lenders assess several factors to determine your risk profile and, consequently, your interest rate:

Your credit score is paramount. A higher FICO score (generally above 740-760) signals a responsible borrower, often leading to access to the lowest available rates. Lower scores indicate higher risk and will result in higher rates.

Your debt-to-income (DTI) ratio, which compares your total monthly debt payments to your gross monthly income, is another critical metric. A lower DTI (typically below 43%) demonstrates that you can comfortably manage additional mortgage payments.

The size of your down payment also influences your rate. A larger down payment (e.g., 20% or more) reduces the lender’s risk, as you have more equity in the property from the start, often translating to better rates and avoiding private mortgage insurance (PMI).

The loan type (conventional, FHA, VA, USDA) and loan term (15-year vs. 30-year) also play a role. Shorter-term loans (e.g., 15-year fixed) typically carry lower interest rates because lenders recover their capital faster and face less long-term interest rate risk. Government-backed loans like FHA and VA have specific criteria and can offer competitive rates to eligible borrowers, often with lower down payment requirements.

Navigating the Current Mortgage Market Landscape

Understanding the current average mortgage rate means placing it within a broader economic context. Financial markets are constantly reacting to data, news, and sentiment, which in turn influences the cost of borrowing.

The Impact of Economic Indicators

Key economic indicators regularly released by government agencies and private firms act as vital signals for the mortgage market. The Consumer Price Index (CPI), a measure of inflation, is closely watched. Higher-than-expected inflation reports often lead to an immediate uptick in mortgage rates as lenders and investors adjust their expectations. Similarly, unemployment rates and job growth figures indicate the health of the economy; a strong jobs report might signal potential inflation pressure, while a weak report could suggest economic slowdown, both of which can impact rate forecasts. Gross Domestic Product (GDP), the broadest measure of economic output, provides a snapshot of economic growth. Robust GDP growth can lead to higher rates if accompanied by inflation concerns, or lower rates if the growth is seen as stable and non-inflationary. These indicators provide a constant pulse on the market, creating daily fluctuations in rates.

Historical Context of Mortgage Rates

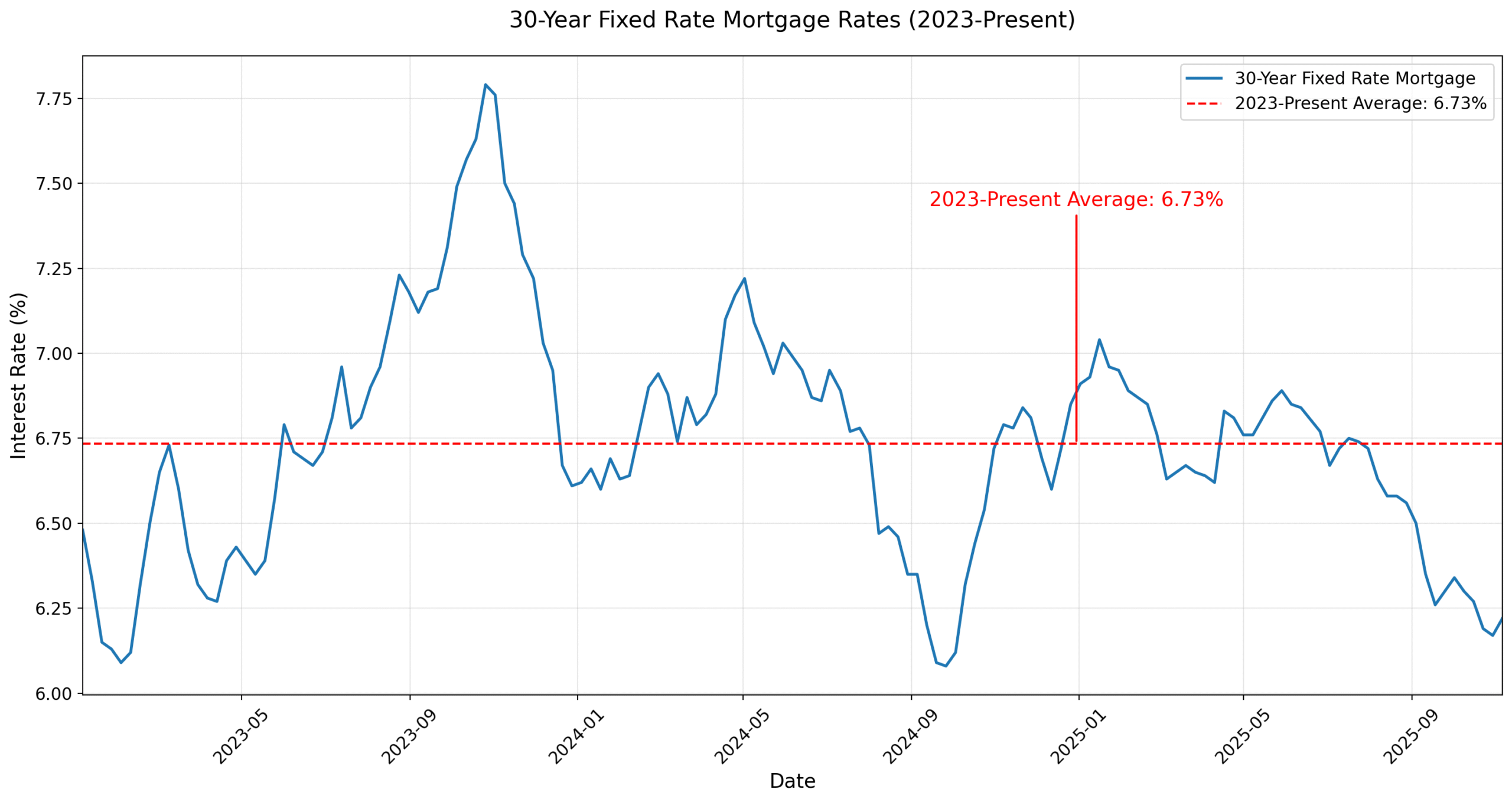

To truly appreciate current rates, it’s helpful to view them through a historical lens. Mortgage rates have seen significant swings over the decades. For example, in the early 1980s, the 30-year fixed mortgage rate soared into the double digits, exceeding 18% at one point, primarily due to aggressive Federal Reserve action to combat runaway inflation. Following this peak, rates gradually trended downwards for decades, reaching historic lows in the early 2020s, with average 30-year fixed rates dipping below 3% in many instances. This period was characterized by low inflation, accommodative monetary policy, and global economic uncertainties that drove investors towards the safety of bonds. Current rates, while higher than the pandemic lows, are still historically reasonable when compared to the average rates of the 1980s, 1990s, and even early 2000s, which often hovered around 6-8%. This perspective helps temper the anxiety around rate increases and provides a more balanced view of affordability.

Regional Variations in Mortgage Rates

While the primary drivers of mortgage rates are national and global, minor regional variations can exist. These differences are usually not substantial enough to be a primary deciding factor for where to buy a home, but they can contribute to the overall picture. Factors like local housing market competitiveness, the prevalence of specific types of lenders (e.g., local credit unions vs. national banks), and regional economic health can subtly influence the rates offered by lenders operating within those areas. Additionally, state-specific regulations or taxes related to real estate transactions can indirectly affect the overall cost of a mortgage, even if the interest rate itself isn’t drastically different.

Strategies for Securing the Best Mortgage Rate

Understanding the market is one thing; actively working to secure the most favorable rate for your personal situation is another. Even small differences in interest rates can translate into tens of thousands of dollars saved over the life of a loan.

Improving Your Financial Profile

The most impactful step you can take to secure a lower rate is to enhance your financial standing. Prioritize boosting your credit score by paying bills on time, reducing credit card balances, and avoiding new credit inquiries before applying for a mortgage. A higher score signifies lower risk to lenders. Next, focus on reducing your debt-to-income (DTI) ratio. Pay down existing debts, especially high-interest consumer loans. This demonstrates your capacity to handle additional monthly obligations. Finally, saving for a larger down payment is crucial. A down payment of 20% or more not only reduces your principal balance and monthly payments but also typically eliminates the need for private mortgage insurance (PMI) on conventional loans, further reducing your overall housing costs and often qualifying you for better interest rates due to the reduced loan-to-value ratio.

Shopping Around for Lenders

One of the most overlooked but effective strategies is to shop around for lenders. Do not simply accept the first offer you receive. Mortgage rates and fees can vary significantly between different financial institutions, including national banks, local credit unions, and independent mortgage brokers. Obtaining quotes from at least three to five different lenders within a short period (usually 14-45 days, so multiple inquiries count as one for credit scoring purposes) allows you to compare annual percentage rates (APRs), origination fees, and other closing costs. Mortgage brokers, in particular, can be valuable as they work with multiple wholesale lenders and can often find competitive rates and products that might not be available directly to consumers.

Understanding Loan Types and Terms

Choosing the right loan type and term for your financial goals is essential. While the 30-year fixed mortgage is popular for its lower monthly payments and stability, a 15-year fixed mortgage typically offers a significantly lower interest rate. Although the monthly payments are higher, you’ll pay substantially less interest over the life of the loan and build equity much faster. Consider government-backed options like FHA loans (for those with lower credit scores or smaller down payments), VA loans (for eligible service members and veterans, often with no down payment and competitive rates), and USDA loans (for properties in eligible rural areas). For higher loan amounts, jumbo loans are available but often have stricter qualification criteria and potentially higher rates. Carefully weigh the pros and cons of each to find the best fit.

The Role of Discount Points and Closing Costs

When reviewing loan offers, pay close attention to discount points and closing costs. Discount points are essentially prepaid interest; one point equals 1% of the loan amount and is paid upfront to reduce your interest rate over the life of the loan. Deciding whether to buy down your rate with points depends on how long you plan to stay in the home. If you plan to sell or refinance relatively soon, the break-even point for recouping the cost of points might not be met. Closing costs, which include fees for appraisals, title insurance, attorney fees, and more, can add 2-5% of the loan amount to your upfront expenses. Factor these into your overall cost analysis, as a loan with a slightly higher interest rate but lower closing costs might be more economical depending on your financial situation and how long you intend to keep the mortgage.

Future Outlook and Considerations for Homebuyers

The housing market and mortgage rates are perpetually in motion, making predictions an exercise in educated guesswork. However, understanding potential future trends is crucial for making timely decisions.

Expert Predictions for Mortgage Rates

Financial institutions and economic analysts constantly publish expert predictions for mortgage rates. While these forecasts are never guarantees, they provide valuable insights into market consensus. Most predictions factor in anticipated Federal Reserve actions, inflation trajectory, and overall economic health. For instance, if inflation is expected to cool, the Fed might ease its monetary policy, potentially leading to stable or even slightly lower mortgage rates. Conversely, persistent inflation or strong economic growth could keep rates elevated. It’s advisable for prospective borrowers to consult several reputable sources for these predictions and understand that they represent the most likely scenarios based on current information, subject to change with new economic data.

When to Lock in Your Rate

The decision of when to lock in your rate is a strategic one. Once you receive a loan offer, lenders typically allow you to “lock” your interest rate for a specific period (e.g., 30, 45, or 60 days) during the underwriting process. This protects you if rates rise before your closing date. If you believe rates are likely to increase, locking in early might be prudent. However, if you anticipate rates will fall, you might consider floating your rate or choosing a shorter lock period with a “float-down” option (if available) that allows you to secure a lower rate if market rates drop before closing. This decision often comes down to your risk tolerance and market outlook.

Refinancing Opportunities

For current homeowners, the average mortgage rate is also highly relevant for refinancing opportunities. Refinancing involves taking out a new mortgage to pay off your old one, often to secure a lower interest rate, change loan terms, or access home equity. If current average rates drop significantly below your existing mortgage rate, refinancing could lead to substantial savings on monthly payments and overall interest paid. Cash-out refinancing allows homeowners to tap into their home equity, but it means taking on a larger loan. The decision to refinance should always involve a thorough cost-benefit analysis, considering closing costs, the new interest rate, and how long you plan to stay in the home.

Broader Implications for the Housing Market

The average mortgage rate has broader implications for the housing market. Higher rates generally reduce buyer affordability, as monthly payments become more expensive for the same loan amount. This can cool demand, potentially leading to slower home price appreciation or even price corrections in some areas. Conversely, lower rates can stimulate demand, making homeownership more accessible and potentially driving up home prices. Rates also affect housing inventory; existing homeowners with low fixed rates may be reluctant to sell if it means buying a new home with a much higher rate, contributing to a shortage of available properties. The current average mortgage rate is therefore a vital indicator of the health and direction of the entire housing ecosystem.

In conclusion, the question “what is the average mortgage rate right now?” doesn’t have a single, static answer. It’s a dynamic figure that reflects the complex interplay of economic forces, lender policies, and individual financial profiles. For anyone engaging with the housing market, staying informed about these dynamics, understanding how rates are determined, and proactively managing their financial readiness are crucial steps toward making sound, long-term financial decisions. By focusing on improving personal credit, diligently shopping for lenders, and strategically choosing loan products, individuals can navigate the current landscape and secure the best possible mortgage rate, turning the dream of homeownership or financial optimization into a tangible reality.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.