Navigating the world of mortgages can feel like an intricate dance, with interest rates acting as the lead choreographer. For many aspiring homeowners and those looking to refinance, the 30-year fixed-rate mortgage remains the quintessential choice, largely due to its predictable payments and long-term stability. However, the “current” interest rate is a moving target, influenced by a complex interplay of economic forces, market sentiment, and individual borrower characteristics. Understanding these dynamics is crucial for making informed financial decisions that can impact your budget for decades.

This article will delve into what constitutes the current interest rate for a 30-year mortgage, the myriad factors that cause it to fluctuate, different types of 30-year mortgage options available, and actionable strategies for securing the most favorable rate. By demystifying the process, we aim to equip you with the knowledge needed to confidently approach one of life’s most significant financial commitments.

Understanding Today’s 30-Year Fixed Mortgage Landscape

The 30-year fixed-rate mortgage is a cornerstone of the American housing market, offering a unique blend of affordability and long-term security. Its prevalence stems from the promise of consistent monthly principal and interest payments over three decades, providing homeowners with a stable financial outlook regardless of market shifts.

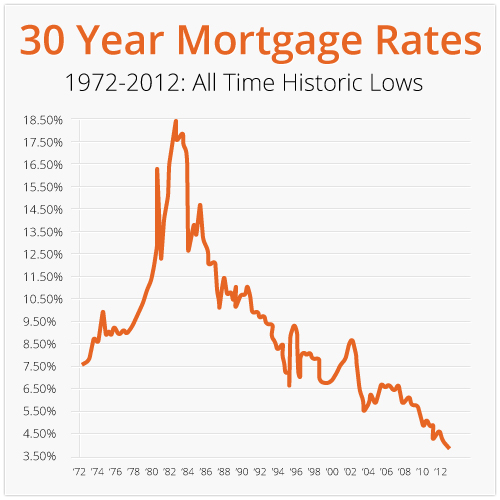

The Snapshot: Averages and Real-Time Data

When people ask “what is the current interest rate,” they’re often seeking a single, definitive number. In reality, mortgage rates are dynamic and can change not just daily, but even hourly. What’s quoted as an “average” rate typically comes from financial institutions like Freddie Mac or the Mortgage Bankers Association, which aggregate data from numerous lenders across the country. These averages serve as valuable benchmarks, indicating general market trends, but they are not guarantees of the rate an individual borrower will receive.

For instance, an average rate published last Tuesday might be different from the rate available this afternoon. Factors such as inflation reports, Federal Reserve announcements, or even geopolitical events can cause swift adjustments. To get a truly “current” rate, you must engage directly with lenders, as they will provide personalized quotes based on the most up-to-date market conditions and your specific financial profile. Online mortgage rate comparison tools can offer a good starting point, providing a quick glance at offerings from various lenders, but always remember to verify with direct quotes.

Why the 30-Year Fixed Remains Popular

The enduring popularity of the 30-year fixed-rate mortgage is not accidental. Its primary appeal lies in its predictability. With a fixed interest rate, your principal and interest payments remain constant for the entire 30-year term, insulating you from the potential volatility of interest rate hikes. This stability simplifies budgeting and provides peace of mind, especially during periods of economic uncertainty.

Furthermore, spreading payments over 30 years typically results in lower monthly installments compared to shorter-term mortgages (like a 15-year fixed). This enhanced affordability allows more individuals to qualify for homeownership and frees up more disposable income for other financial goals or expenses. While a longer term means paying more interest over the life of the loan, the stability and lower monthly burden are often compelling advantages for many borrowers, making it a prudent choice for those prioritizing consistent cash flow and long-term financial planning.

Key Factors Driving Mortgage Rate Fluctuations

Mortgage interest rates are not arbitrarily set; they are a direct reflection of a complex ecosystem influenced by various economic indicators, market forces, and individual circumstances. Understanding these drivers is essential for anticipating rate movements and timing your mortgage decisions effectively.

Economic Indicators and Federal Reserve Policy

The health of the broader economy plays a pivotal role in shaping mortgage rates. Inflation, unemployment rates, and Gross Domestic Product (GDP) growth are all closely watched indicators. When inflation rises, the Federal Reserve often steps in to cool the economy by increasing the federal funds rate. While the federal funds rate doesn’t directly dictate mortgage rates, it influences the cost of borrowing for banks, which then trickles down to consumers. Similarly, the Fed’s quantitative easing (buying bonds) or tightening (selling bonds) policies significantly impact the supply and demand for mortgage-backed securities, thereby affecting rates. A strong economy, often characterized by low unemployment and robust GDP growth, can lead to higher interest rates as lenders anticipate increased demand for credit and potential inflationary pressures. Conversely, economic slowdowns or recessions often see rates dip as the Fed attempts to stimulate activity.

Bond Market Influence

Perhaps the most direct influence on fixed mortgage rates comes from the bond market, specifically the yield on U.S. Treasury bonds and mortgage-backed securities (MBS). Mortgage rates tend to track the yield of the 10-year Treasury note. When investors demand higher returns on these bonds (i.e., their yields rise), mortgage rates typically follow suit. This is because MBS compete with Treasury bonds for investor dollars. If Treasury yields are attractive, MBS must offer a competitive yield (higher interest rate) to attract investors. News, economic reports, and investor sentiment can cause rapid shifts in bond yields, which in turn leads to daily fluctuations in mortgage rates. Geopolitical events, global economic trends, and even stock market performance can also indirectly impact bond yields and, consequently, mortgage rates.

Lender-Specific Considerations

While economic and bond market factors set the general trend, individual lenders also contribute to rate variations. Each bank or mortgage company has its own operational costs, risk assessment models, and profit margins. A lender with lower overhead or a more aggressive growth strategy might offer slightly more competitive rates to attract business. Furthermore, a lender’s current loan volume and capacity can influence their pricing. If a lender is struggling to meet lending targets, they might temporarily lower rates, or if they are overwhelmed, they might subtly increase them to slow the influx of applications. It’s why shopping around is so crucial: the same borrower might be offered different rates from different institutions on the very same day.

Borrower-Specific Factors

Beyond the broader market, your personal financial profile is a significant determinant of the interest rate you’ll be offered. Lenders assess risk, and a higher-risk borrower typically receives a higher interest rate.

- Credit Score: A strong credit score (typically 740 or above) signals to lenders that you are a reliable borrower with a history of timely payments. This usually qualifies you for the lowest available rates. Scores below this threshold often result in higher rates or more stringent lending requirements.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates that you have sufficient income to manage your new mortgage payments, making you a less risky borrower. Most lenders prefer a DTI below 43%, though some government-backed loans have more flexible guidelines.

- Loan-to-Value (LTV) Ratio & Down Payment: The LTV ratio compares the loan amount to the home’s appraised value. A larger down payment reduces your LTV, meaning you’re borrowing a smaller percentage of the home’s value. This reduces the lender’s risk and can lead to a more favorable interest rate. A down payment of 20% or more often helps avoid Private Mortgage Insurance (PMI) on conventional loans, further reducing your overall housing costs.

- Loan Type: While we’re focusing on 30-year fixed, even within this category, different loan programs (e.g., conventional, FHA, VA, USDA) carry different risk assessments and therefore different rates.

Navigating Different 30-Year Mortgage Options

While the “30-year mortgage” broadly refers to a loan amortized over three decades, there are important distinctions within this category that can significantly impact your financial commitment and risk exposure. Choosing the right option involves evaluating your financial situation, risk tolerance, and long-term housing plans.

Fixed-Rate Mortgages: The Standard

The 30-year fixed-rate mortgage is the most common and often the most recommended option for many homebuyers. Its defining characteristic is that the interest rate remains constant throughout the entire 30-year term. This stability means your principal and interest payments will never change, regardless of economic fluctuations.

Pros:

- Predictability: Easy budgeting and financial planning due to consistent monthly payments.

- Protection: Immune to rising interest rates, providing security during inflationary periods.

- Simplicity: Straightforward payment structure.

Cons:

- Higher Initial Rate: Often starts at a slightly higher interest rate compared to an introductory period of an ARM.

- Slower Equity Build-Up: More interest is paid in the early years compared to principal.

- No Benefit from Falling Rates: If market rates drop significantly, you’ll need to refinance to take advantage, incurring new closing costs.

This option is ideal for those who value stability, plan to stay in their home for many years, and prefer the peace of mind that comes with predictable housing costs.

Adjustable-Rate Mortgages (ARMs): A Niche for Some

While less common for a full 30-year term, hybrid ARMs offer a fixed interest rate for an initial period (e.g., 3, 5, 7, or 10 years) and then adjust periodically based on a predetermined index plus a margin for the remainder of the 30-year loan term. For example, a 5/1 ARM means the rate is fixed for the first five years, then adjusts annually.

Pros:

- Lower Initial Rate: Often provides a lower interest rate during the initial fixed period compared to a 30-year fixed-rate mortgage.

- Potential Savings: If rates fall, your payments could decrease (though there’s no guarantee).

- Flexibility for Short-Term Plans: Good for those who anticipate selling or refinancing before the fixed period ends.

Cons:

- Rate Volatility: Payments can increase significantly after the fixed period, making budgeting challenging.

- Complexity: Understanding the index, margin, and caps (limits on how much the rate can change) can be complicated.

- Increased Risk: Exposes borrowers to interest rate risk if rates rise.

ARMs are typically suited for financially savvy individuals who are comfortable with risk, expect their income to rise significantly, or plan to move or refinance before the adjustable period begins.

Government-Backed Loans: Specific Benefits and Eligibility

Beyond conventional loans, several government-backed programs offer 30-year mortgages with specific advantages and eligibility criteria.

- FHA Loans: Insured by the Federal Housing Administration, these loans are popular for first-time homebuyers or those with less-than-perfect credit. They typically require a lower down payment (as low as 3.5%) and have more lenient credit score requirements. However, they mandate mortgage insurance premiums (MIP) for the life of the loan in many cases.

- VA Loans: Guaranteed by the U.S. Department of Veterans Affairs, these loans are available to eligible active-duty service members, veterans, and surviving spouses. They often feature 0% down payment requirements, no private mortgage insurance, and competitive interest rates, making them an incredibly valuable benefit for those who qualify.

- USDA Loans: Backed by the U.S. Department of Agriculture, these loans are designed for low-to-moderate-income borrowers purchasing homes in eligible rural areas. They also offer 0% down payment options and competitive rates but come with income limits and specific property location requirements.

These government-backed options can significantly expand access to homeownership for various groups, offering favorable terms that conventional loans might not. It’s crucial to explore these if you meet the eligibility criteria, as they can sometimes provide a more affordable path to a 30-year mortgage.

Strategies for Securing the Best Mortgage Rate

Obtaining the lowest possible interest rate on your 30-year mortgage can save you tens of thousands of dollars over the life of the loan. It requires a proactive approach, diligent preparation, and strategic decision-making.

Improving Your Financial Profile

Before even speaking to a lender, taking steps to enhance your financial standing can make a significant difference in the rates you’re offered.

- Credit Score Optimization: Your credit score is paramount. Pay all bills on time, reduce outstanding debt, especially on credit cards, and avoid opening new lines of credit in the months leading up to your mortgage application. Dispute any errors on your credit report. Aim for a FICO score of 740 or higher for the best rates.

- Debt Reduction: Lowering your debt-to-income (DTI) ratio makes you a less risky borrower. Focus on paying down high-interest debts or consolidating them to free up monthly cash flow. Lenders look for a DTI generally below 43%, though lower is always better.

- Saving for a Larger Down Payment: A larger down payment (e.g., 20% or more) reduces your loan-to-value (LTV) ratio, which can qualify you for better rates and often eliminates the need for private mortgage insurance (PMI) on conventional loans. Even if you can’t hit 20%, a larger down payment still signals financial stability to lenders.

The Power of Comparison Shopping

This is arguably the most impactful strategy. Do not settle for the first quote you receive.

- Multiple Lenders: Contact at least three to five different lenders—including large banks, local credit unions, and online mortgage companies. Each lender has different pricing models, overheads, and appetites for risk, leading to varying rate offers.

- Mortgage Brokers: Consider working with a mortgage broker. They act as intermediaries, working with multiple lenders to find you the best rates and terms for your specific situation, potentially saving you time and effort.

- Online Tools: Utilize online mortgage rate comparison websites. While these provide estimates, they can quickly give you a sense of current market rates and highlight lenders offering competitive terms.

- “Shopping Window”: Apply for all your mortgage pre-approvals within a short timeframe (typically 14-45 days). Credit bureaus recognize this as a single credit inquiry for mortgage shopping, minimizing the impact on your credit score.

Understanding Rate Locks and Closing Costs

Once you receive a favorable rate, it’s crucial to understand how to secure it and the additional costs involved.

- Rate Locks: A rate lock guarantees your interest rate for a specific period (e.g., 30, 45, or 60 days) while your loan application is processed. This protects you from rate increases. Discuss the length of the lock with your lender, as longer locks might come with a small fee or a slightly higher rate. Ensure the lock period is sufficient for your closing timeline.

- Closing Costs: Beyond the interest rate, closing costs can significantly impact the overall expense of your mortgage. These typically range from 2% to 5% of the loan amount and include appraisal fees, origination fees, title insurance, attorney fees, and more. Compare the total closing costs from different lenders, as a slightly higher rate with lower closing costs might be more beneficial in the long run, or vice versa. Some costs might be negotiable, so don’t hesitate to ask.

Professional Guidance

The mortgage process is complex, and expert advice can be invaluable.

- Mortgage Brokers vs. Direct Lenders: Understand the pros and cons of each. Brokers offer choice; direct lenders might offer a more streamlined process.

- Financial Advisors: For those with complex financial situations, a financial advisor can help assess how a mortgage fits into your broader financial plan and long-term goals.

The Long-Term Impact of Your Mortgage Rate Decision

The interest rate you secure on your 30-year mortgage is far more than just a number; it’s a financial lever that will profoundly influence your monthly budget and total wealth accumulation over three decades. Even a small difference in basis points can translate into substantial savings or added costs.

Monthly Payments and Budgeting

The most immediate impact of your interest rate is on your monthly principal and interest (P&I) payment. A lower rate directly translates to a lower monthly payment, which can significantly improve your household cash flow. For instance, on a $300,000 30-year fixed mortgage, reducing the interest rate from 7.0% to 6.5% could save you approximately $98 per month. Over a year, that’s nearly $1,200, money that could be allocated to savings, investments, other debt reduction, or discretionary spending. This immediate financial relief makes a lower rate highly desirable for budgeting and maintaining financial flexibility. Conversely, a higher rate can strain your budget, limiting your financial choices and potentially impacting your ability to save for other important goals.

Total Cost Over the Loan Term

While the monthly payment is a primary concern, it’s the total interest paid over 30 years that truly highlights the long-term financial ramifications of your rate. The compounding effect of interest means that even a seemingly minor difference in the rate can add up to tens of thousands of dollars. Using the previous example of a $300,000 loan:

- At 7.0%, the total interest paid over 30 years would be approximately $418,638, leading to a total cost of $718,638.

- At 6.5%, the total interest paid would be about $381,623, bringing the total cost to $681,623.

This difference of $37,015 in total interest paid for just a 0.5% rate reduction underscores the profound impact of securing a favorable interest rate. This significant sum represents capital that could have been invested, used for retirement, or passed down as wealth, illustrating how a wise mortgage decision contributes to long-term financial well-being.

Refinancing Opportunities

Your mortgage rate decision isn’t necessarily set in stone for 30 years. The market is dynamic, and interest rates fluctuate over time. If rates drop significantly after you’ve secured your mortgage, refinancing becomes a viable option. Refinancing involves taking out a new loan to pay off your existing mortgage, ideally at a lower interest rate, or to change the loan terms. This can reduce your monthly payments, decrease the total interest paid, or even shorten your loan term.

However, refinancing comes with its own set of closing costs, similar to your original mortgage. Therefore, it’s crucial to calculate the break-even point – how long it will take for your monthly savings to offset the refinancing costs – to determine if it’s a financially sound decision. Monitoring market rates and consulting with a mortgage professional periodically can help you identify opportune times to consider refinancing and further optimize your long-term housing costs.

In conclusion, the interest rate on your 30-year mortgage is a cornerstone of your personal financial landscape. It dictates not only your immediate monthly outlay but also the overall cost of your home for decades to come. By understanding the forces that shape these rates, diligently preparing your financial profile, and engaging in thorough comparison shopping, you empower yourself to make a decision that can save you a significant amount of money, fostering greater financial stability and peace of mind throughout your homeownership journey. Always consider professional advice to tailor these strategies to your unique circumstances.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.