Finding the cheapest car insurance is a perennial goal for many drivers, yet the answer is rarely a single, static name. In the world of personal finance, auto insurance represents one of the most significant recurring expenses for the average household. Because premiums are calculated using complex, proprietary algorithms that weigh hundreds of different factors, the company that offers the lowest rate for a 40-year-old homeowner in Ohio may be the most expensive option for a 22-year-old renter in Florida.

Navigating this landscape requires more than just a quick search; it requires an understanding of how the insurance industry prices risk and how you can position your financial profile to attract the lowest possible rates. This guide explores the market leaders in affordability, the mechanics behind premium pricing, and the strategic financial moves you can make to reduce your annual outlay.

Understanding the Landscape of Modern Auto Insurance Pricing

Before identifying specific providers, it is crucial to understand that “cheap” is a relative term in the insurance industry. Insurance companies are essentially risk managers. Their goal is to predict the likelihood that you will file a claim and price your policy accordingly. When a company offers you a low rate, it is because their specific data models view you as a low-risk investment.

The Variables That Dictate Your Premium

Your car insurance premium is a reflection of your personal financial and behavioral history. While most drivers are aware that their driving record impacts their rates, other factors are equally influential. For instance, in many states, your credit-based insurance score plays a massive role. Actuarial data suggests a correlation between financial responsibility and driving safety; therefore, individuals with high credit scores often enjoy significantly lower premiums.

Other variables include the type of vehicle you drive (repair costs and safety ratings), your annual mileage, and your zip code. High-traffic urban areas with high rates of theft and accidents will naturally command higher premiums than quiet rural districts. By understanding these variables, you can begin to see insurance not as a fixed cost, but as a manageable financial metric.

Why “Cheapest” is Relative to Your Profile

There is no “one size fits all” in car insurance. Some companies specialize in “preferred” drivers—those with pristine records and high credit scores—and offer them bottom-dollar rates. Other companies specialize in the “non-standard” market, catering to those with DUIs or multiple accidents. If you apply to a company that prefers high-credit homeowners when you are a young renter with a spotty driving record, you will receive a quote that is intentionally uncompetitive. The “cheapest” insurance is found at the intersection of your specific profile and a company’s preferred demographic.

Top Contenders for the Most Affordable Car Insurance

While rates vary, several national carriers consistently rank at the top of the list for affordability across a broad spectrum of drivers. These companies leverage massive scale, advanced technology, and diverse business models to keep their pricing competitive.

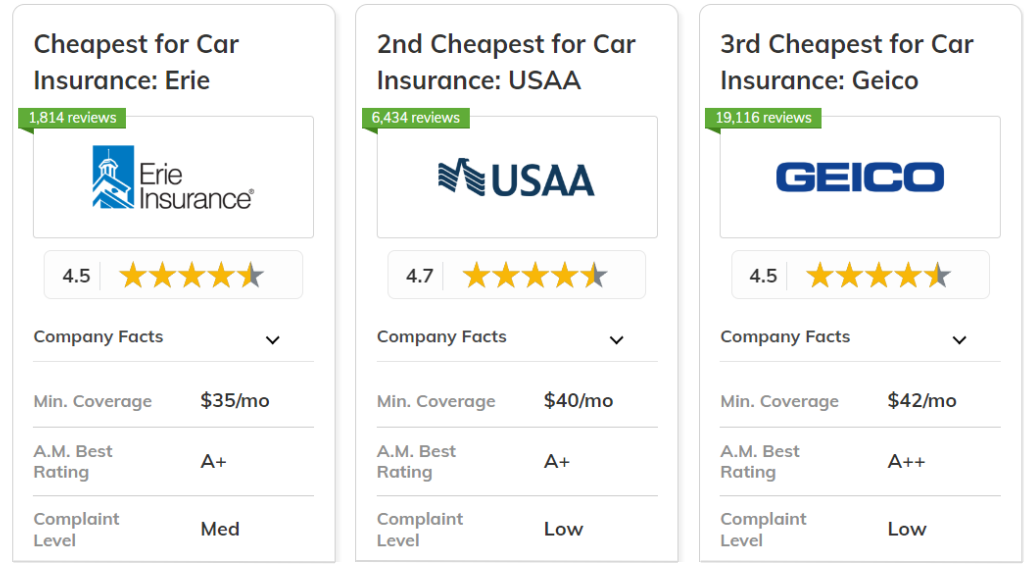

Geico: The King of Direct-to-Consumer Value

Geico has built its brand on the promise of “15 minutes could save you 15% or more,” and for many, this isn’t just marketing hyperbole. As a direct-to-consumer insurer, Geico avoids the overhead costs associated with maintaining a vast network of local agents. These savings are often passed down to the consumer. Geico is particularly competitive for drivers with clean records and those who prefer managing their policies via a robust mobile app. Their efficiency in processing and underwriting makes them a frequent winner for the title of the cheapest national carrier.

State Farm: Strength in Scale and Local Presence

Unlike Geico’s direct model, State Farm utilizes a massive network of local agents. Despite this overhead, State Farm remains one of the most affordable options in the United States, particularly for families and multi-policy holders. Because State Farm is a mutual insurance company—meaning it is owned by its policyholders rather than shareholders—it often prioritizes long-term stability and competitive pricing over short-term profit spikes. They are frequently the cheapest option for drivers who want a personal relationship with an agent without paying a premium for the privilege.

Progressive: Transparency and the “Name Your Price” Model

Progressive is a pioneer in the use of data and technology to drive down costs. Their “Name Your Price” tool and comparative rating systems allow consumers to see how Progressive’s rates stack up against the competition in real-time. Progressive is often the most affordable choice for drivers who have a few blemishes on their record, as their high-tech underwriting models are often better at “forgiving” minor infractions than more traditional carriers.

USAA: The Gold Standard for Military Families

It is impossible to discuss the cheapest car insurance without mentioning USAA. Consistently ranked as the least expensive and highest-rated insurer in the country, USAA is unfortunately limited to active-duty military, veterans, and their immediate families. If you qualify for USAA, it is almost certainly the most cost-effective financial decision you can make regarding your vehicle. Their lean operations and commitment to the military community allow them to offer rates that commercial competitors often cannot match.

Strategic Tactics to Lower Your Premiums

Finding the cheapest insurance isn’t just about picking the right company; it’s about active financial management. By employing specific strategies, you can force your premiums downward regardless of which carrier you choose.

Telematics and Usage-Based Insurance (UBI)

The most significant shift in car insurance in the last decade is the rise of telematics. Programs like Progressive’s Snapshot or State Farm’s Drive Safe & Save use a plug-in device or a smartphone app to monitor your actual driving habits—braking, acceleration, and time of day. For a safe, low-mileage driver, opting into a telematics program can result in discounts of 30% or more. This moves the needle from “estimated risk” to “actual risk,” rewarding you directly for your behavior on the road.

The Power of Bundling and Loyalty Discounts

From a business finance perspective, it is cheaper for an insurance company to retain a customer than to acquire a new one. This is why “bundling” is so effective. By combining your auto insurance with homeowners, renters, or life insurance, you can often save 10% to 25% across all policies. Additionally, many companies offer “tenure” discounts. While it pays to shop around every few years, jumping ship for a $20 annual saving might cost you more in the long run by resetting your loyalty status.

Adjusting Deductibles and Coverage Limits

One of the most direct ways to lower your premium is to assume more of the risk yourself. Increasing your deductible from $500 to $1,000 can significantly reduce your monthly payments. However, this is a personal finance decision that requires a healthy emergency fund. You should only raise your deductible to a level you can comfortably afford to pay out of pocket in the event of a claim. Similarly, if you drive an older vehicle with low market value, dropping collision or comprehensive coverage can result in immediate and substantial savings.

The Impact of Demographics and Geography on Your Wallet

Your physical location and your stage in life are two of the most powerful “uncontrollable” factors in insurance pricing. Understanding these can help you set realistic expectations for your insurance budget.

Age, Gender, and Driving Experience

From a financial perspective, young drivers are high-liability assets. Statistics show that drivers under the age of 25 are involved in more accidents, leading to the highest premiums in the market. Conversely, as you move into your 30s, 40s, and 50s, your rates typically decline as your experience increases. Gender also plays a role in many states, with young men often paying more than young women due to higher risk-taking behaviors documented in actuarial data.

State-by-State Variations and Regulation

The “cheapest” company changes based on state lines. This is due to different state laws regarding “no-fault” insurance, minimum coverage requirements, and the level of litigation in a given area. For example, drivers in Michigan often pay some of the highest rates in the nation due to unique personal injury protection requirements, while drivers in Maine or Idaho enjoy some of the lowest. When looking for the cheapest insurance, always use tools that provide localized quotes rather than national averages.

Beyond the Price Tag: Balancing Cost with Financial Security

The quest for the cheapest car insurance should never come at the expense of your overall financial health. The goal of insurance is to protect your assets from a catastrophic loss.

Evaluating Claims Processes and Customer Service

Cheap insurance is only a bargain until you need to use it. A company that offers a rock-bottom rate but makes the claims process a nightmare can end up costing you more in lost time, stress, and out-of-pocket expenses. Before signing with the cheapest provider, consult the J.D. Power claims satisfaction rankings. A company with a slightly higher premium but a stellar reputation for paying claims fairly and quickly is often the better long-term financial investment.

Ensuring Adequate Coverage Limits

In the world of personal finance, being “under-insured” is a major risk. Opting for “state minimum” coverage might give you the cheapest monthly payment, but it leaves your personal assets—your home, your savings, and your future earnings—vulnerable to lawsuits if you are at fault in a major accident. The smartest way to find the “cheapest” insurance is to determine the level of coverage you actually need to protect your net worth, and then find the lowest price for that specific amount of coverage.

In conclusion, finding the cheapest car insurance is an exercise in both shopping and self-optimization. By maintaining a strong credit score, utilizing telematics, bundling your policies, and selecting a carrier that favors your specific demographic, you can significantly reduce your cost of ownership. Remember that the “cheapest” policy is the one that provides the maximum amount of necessary protection for the minimum amount of capital, ensuring your financial stability remains intact even when the road gets bumpy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.