In the sophisticated world of personal finance and investment, clarity is the ultimate currency. While we often rely on digital dashboards and automated spreadsheets to manage our wealth, the fundamental mathematics underlying these tools remain the bedrock of sound financial decision-making. One of the most basic yet essential mathematical conversions is the transition from a decimal to a fraction.

While a decimal provides a clean, linear look at a number—often seen in interest rates like 4.5% or stock prices like $150.25—a fraction represents a relationship between parts and a whole. Understanding how to convert a decimal to a fraction is not just an academic exercise; it is a vital skill for anyone looking to master asset allocation, understand dividend yields, or navigate the nuances of fractional share investing.

The Role of Mathematical Precision in Personal Finance

To the uninitiated, the difference between 0.125 and 1/8 might seem purely cosmetic. However, in the context of money, these two representations serve different psychological and analytical purposes. Decimals are the language of transactions, but fractions are the language of proportion.

Understanding the “Language of Money”

Most financial instruments are quoted in decimals because they are easier for computers to process and for consumers to read quickly. When you look at your savings account’s Annual Percentage Yield (APY), you see a decimal. When you look at the expense ratio of an Exchange-Traded Fund (ETF), you see a decimal.

However, professional investors often think in ratios. A decimal tells you “how much,” but a fraction tells you “how much of the whole.” For instance, knowing that a specific commodity represents 0.05 of your portfolio is one thing, but realizing that it is exactly 1/20th of your total net worth provides a clearer picture of your risk exposure.

Why Decimals Often Mask the Reality of Debt

In the world of consumer credit, decimals are often used to make costs seem smaller than they are. An interest rate of 0.015% per day sounds negligible. However, when converted into a fractional understanding of your annual income or your total debt load, the weight of that number becomes more apparent. Converting these decimals back into fractions allows a person to see the “slice” of their financial pie that is being consumed by interest, rather than just viewing it as a minor numerical fluctuation.

Step-by-Step Guide to Converting Decimals to Fractions

Converting a decimal to a fraction is a straightforward process that involves three primary steps: identifying the place value, creating a ratio, and simplifying that ratio. In financial terms, this is the equivalent of breaking down a complex percentage into its component parts to see the underlying value.

Identifying the Place Value (Tenths, Hundredths, and Thousandths)

Every digit to the right of the decimal point has a specific place value. In finance, we most commonly deal with “hundredths,” which we call cents or basis points.

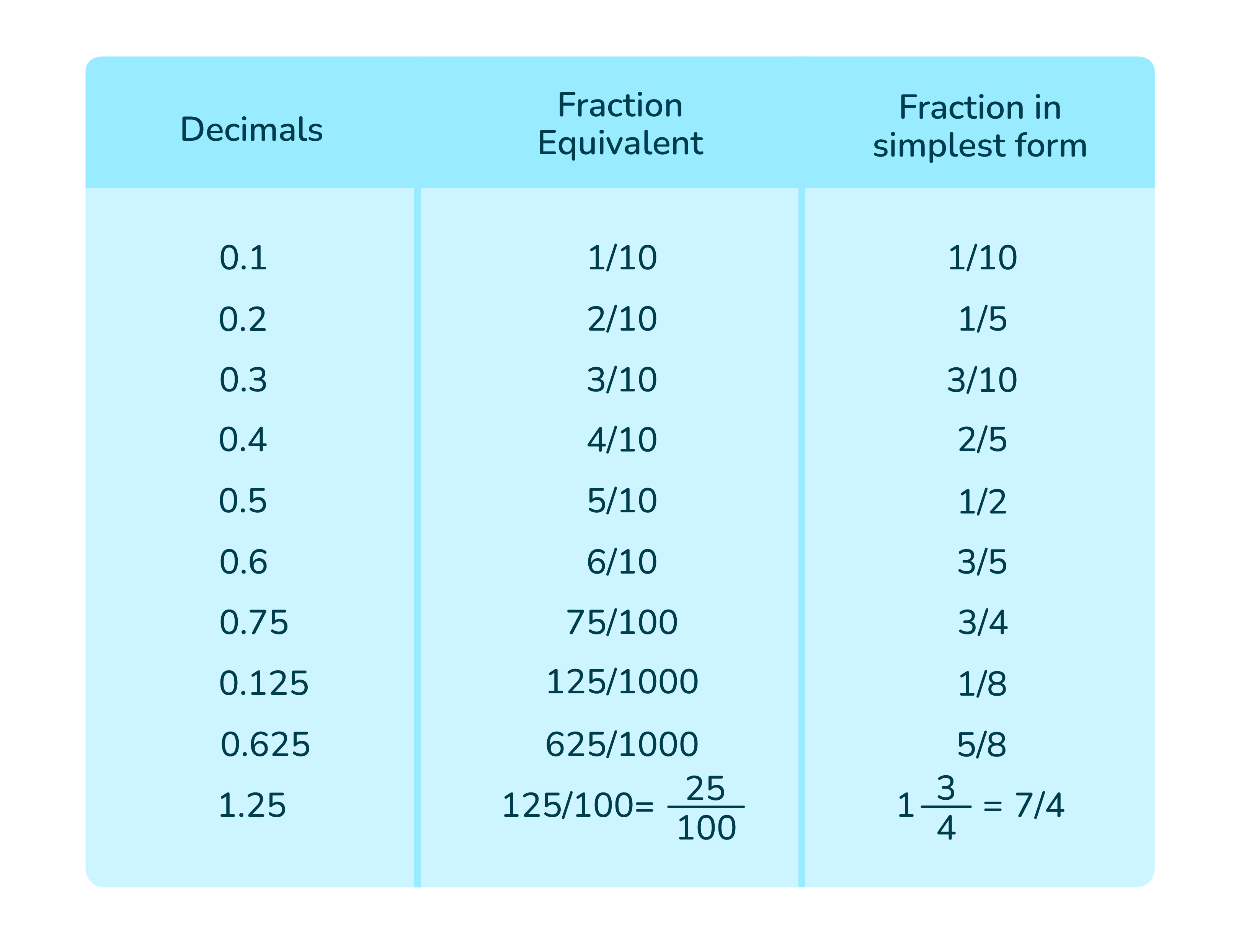

- The first decimal place (0.x) is the tenths place.

- The second decimal place (0.xx) is the hundredths place.

- The third decimal place (0.xxx) is the thousandths place.

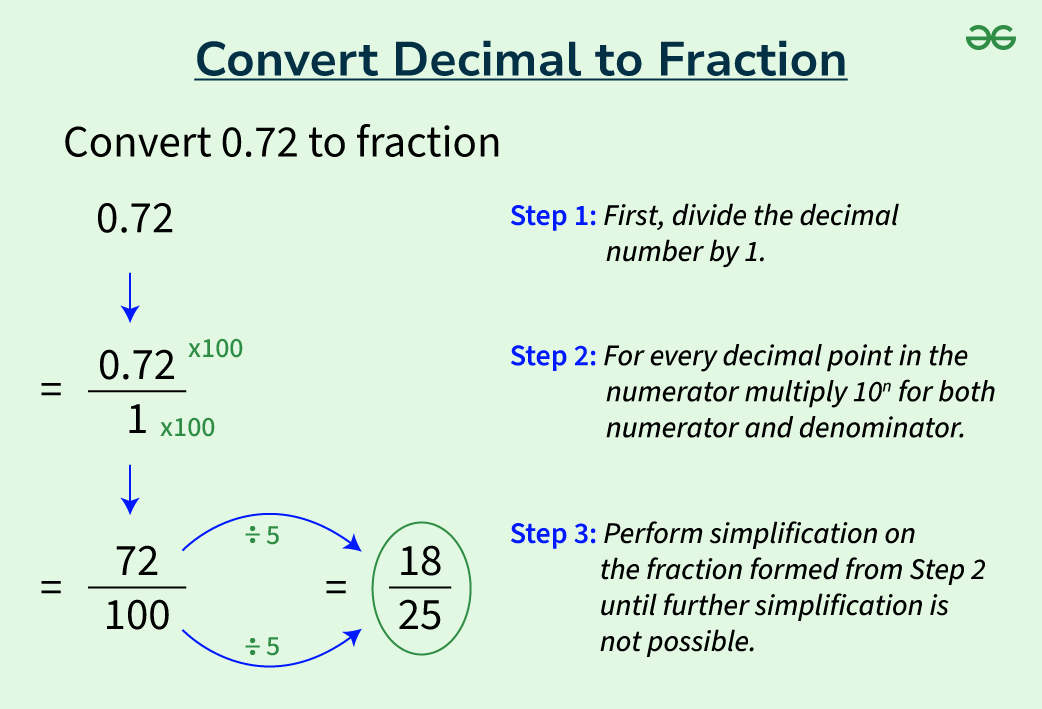

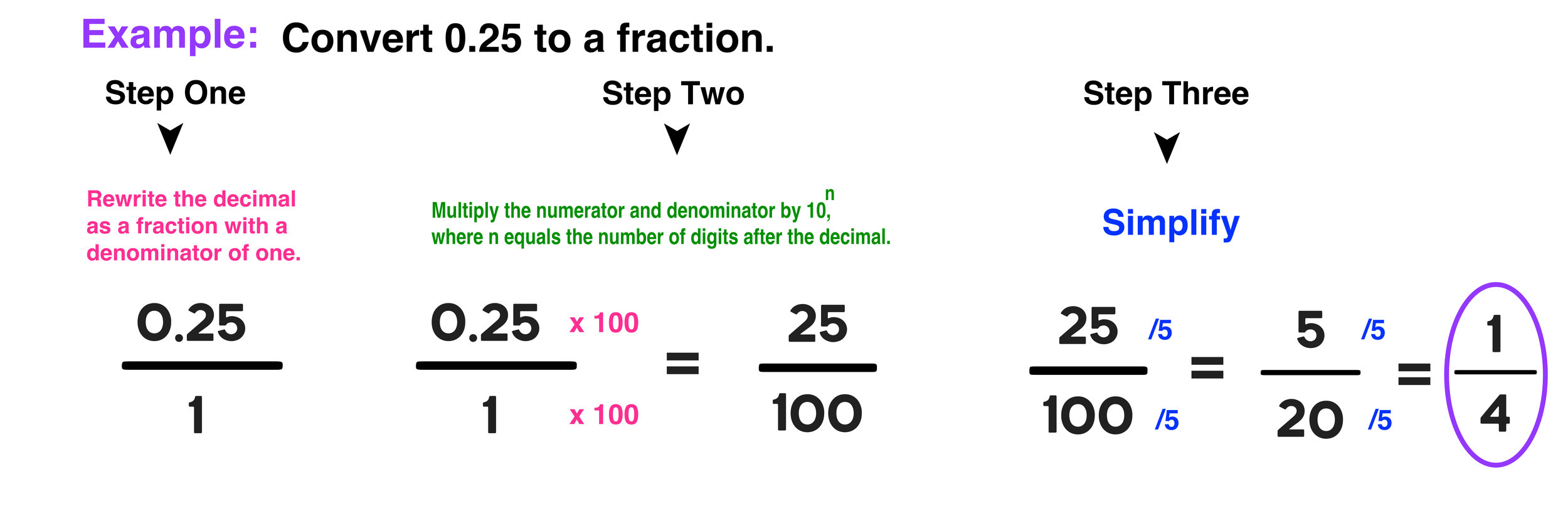

To begin the conversion, you take the numbers to the right of the decimal and place them over the value of the last digit’s place. For example, if you are looking at a dividend of 0.75, the “5” is in the hundredths place. Therefore, the initial fraction is 75/100.

Simplifying the Ratio: The Key to Identifying Yield

A fraction like 75/100 is accurate, but it isn’t “useful” for quick mental comparisons. This is where simplification comes in. To simplify a fraction, you find the Greatest Common Divisor (GCD)—the largest number that goes into both the numerator (top) and the denominator (bottom).

Using our 75/100 example:

- Both 75 and 100 are divisible by 25.

- 75 divided by 25 is 3.

- 100 divided by 25 is 4.

- The simplified fraction is 3/4.

In a financial context, seeing 3/4 tells you immediately that for every four dollars of value, three dollars are being represented by this specific metric.

Real-World Example: Converting 0.125 to an Investment Ratio

In historical stock trading, prices were often quoted in eighths. If a stock was trading at a decimal of 0.125 above its base price, an experienced trader knew this was 125/1000. By dividing both the top and bottom by 125, you arrive at 1/8. Understanding this conversion allows you to see the “tick” movements in a market that still, in many ways, respects these traditional fractional divisions.

Applying Fractional Thinking to Investment Strategies

As we move deeper into the digital age of finance, the “fraction” has seen a massive resurgence in popularity, specifically through the rise of fractional shares and micro-investing.

Fractional Shares: The New Frontier of Accessibility

Until recently, if a single share of a high-performing tech company cost $3,000, it was inaccessible to the average retail investor. Today, fintech apps allow you to buy “0.005” of a share. While the app displays a decimal, the underlying concept is a fraction. By converting that 0.005 back into a fraction (5/1000, which simplifies to 1/200), you can better understand your position. You own one two-hundredth of a share. This perspective is vital for calculating how many more “parts” you need to acquire to own a full unit of that asset.

Dividend Yields and the Power of Ratios

Dividend yields are almost always expressed as decimals or percentages (e.g., 0.04 or 4%). For a dividend growth investor, converting this to a fraction helps in visualizing the “reinvestment” power. A 0.05 (1/20) yield means that for every 20 shares you own, the company is effectively giving you one “free” share every year through its payout. This fractional visualization makes the concept of compound interest much more tangible than a simple decimal string.

Asset Allocation: Visualizing Your Portfolio as a Whole

Modern portfolio theory suggests diversifying your assets across various classes (stocks, bonds, real estate, cash). If your dashboard shows you have 0.40 in stocks, 0.30 in bonds, 0.20 in real estate, and 0.10 in cash, converting these to fractions (2/5, 3/10, 1/5, and 1/10) allows for a more intuitive “pie chart” mental model. It becomes easier to see that your bond holdings are three times the size of your cash reserves, a comparison that is sometimes less intuitive when looking only at decimals.

Digital Tools vs. Mental Math in Financial Literacy

While we have access to calculators that can handle these conversions in milliseconds, the reliance on technology can sometimes dull our financial intuition. There is a profound difference between a tool giving you an answer and you understanding the relationship between the numbers.

The Best Financial Calculators and Apps for Conversions

For those dealing with complex tax calculations or currency conversions, digital tools are indispensable. Professional-grade financial calculators like the HP 12C or modern apps like Bloomberg and Reuters Eikon have built-in functions to toggle between decimals and fractions. These tools are essential for precision when dealing with basis points (bps), where a movement of 0.01% (1/100th of a percent) can mean millions of dollars in institutional trading.

Why Mastering the Math Mentally Improves Financial Decision-Making

Despite the availability of tools, the ability to perform these conversions mentally provides a “sanity check” against errors. If an investment salesperson tells you that a fee is “only 0.5,” and you can instantly recognize that as 1/2 (or 50% in some contexts) or 1/200 of your total capital, you can immediately assess the impact on your long-term wealth.

Mathematical literacy is a defense mechanism against predatory lending and confusing marketing. When you can convert decimals to fractions on the fly, you are no longer just a consumer of financial data; you are an analyst of it.

Conclusion: Precision as a Path to Wealth

The journey to financial independence is paved with numbers. While the conversion of a decimal to a fraction—moving from 0.5 to 1/2—may seem like a rudimentary skill from a middle-school classroom, its application in the boardroom and the brokerage account is profound.

By mastering this conversion, you gain a deeper insight into the proportions of your investments, the true cost of your debts, and the mechanics of market movements. Precision in math leads to precision in strategy. Whether you are calculating the “slice” of a company you own through fractional shares or determining the simplified yield of a bond, the ability to see the ratio behind the decimal is a hallmark of a sophisticated and successful investor. In the end, wealth is not just about how much money you have, but how clearly you understand the numbers that define it.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.