In the sophisticated landscape of modern finance, the pharmaceutical industry stands as one of the most resilient yet volatile sectors for investors. To the average consumer, asking “what class of drug is tramadol” is a matter of health and safety. However, to the institutional investor, the hedge fund analyst, or the retail trader, the answer to that question serves as a foundational data point for assessing market viability, regulatory risk, and revenue longevity.

Tramadol, a synthetic opioid analgesic, represents a unique intersection of medical necessity and financial complexity. Its classification—not just pharmacologically, but legally and economically—dictates the lifecycle of the product and the profit margins of the companies that manufacture it. This article explores the business of tramadol, analyzing how drug classification influences investment strategies, market competition, and the broader economic landscape of the healthcare industry.

The Financial Significance of Drug Classification

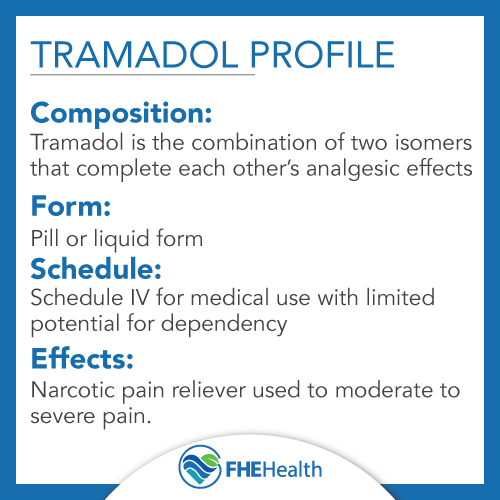

When we categorize a drug like tramadol, we are essentially defining its regulatory overhead. In the United States, the Drug Enforcement Administration (DEA) classifies tramadol as a Schedule IV controlled substance. This classification is the “DNA” of the drug’s financial profile.

Scheduled Substances and Market Barriers

For a business, the classification of a drug determines the height of the “moat” and the cost of entry. Schedule IV substances are defined as drugs with a lower potential for abuse relative to Schedule III drugs, but they still require stringent oversight. From a business finance perspective, this means that any company involved in the production, distribution, or sale of tramadol must invest heavily in compliance infrastructure.

These costs include specialized auditing, secure logistics, and rigorous reporting requirements. For smaller pharmaceutical firms, these compliance costs can be a barrier to entry, whereas for diversified giants, they represent a manageable “cost of doing business” that keeps smaller competitors at bay.

Regulatory Impacts on Revenue Streams

The classification also dictates the ease of prescription. Unlike Schedule II drugs (like oxycodone), which face extreme restrictions and limited refills, Schedule IV drugs like tramadol offer more flexibility for physicians. In the world of pharmaceutical sales, higher prescription flexibility often correlates with higher volume. Investors look at the “Schedule IV” tag as a signal of a “sweet spot”: it is regulated enough to maintain high barriers to entry, yet accessible enough to sustain high-volume sales in the chronic pain management market.

Tramadol as a Case Study in Generic vs. Branded Assets

In the pharmaceutical economy, the transition from a branded drug to a generic one is known as the “patent cliff.” Tramadol provides a quintessential example of how an asset evolves through its lifecycle and what that means for a portfolio’s bottom line.

The Patent Cliff and Generic Competition

Originally marketed under brand names like Ultram, tramadol was once a high-margin proprietary asset. When a drug is under patent protection, the manufacturer enjoys a monopoly, allowing for premium pricing that covers the astronomical costs of Research and Development (R&D).

However, once the patent expires and the drug’s classification remains stable, generic manufacturers flood the market. For investors, this is a pivot point. The “Money” story of tramadol shifted from one of high-margin exclusivity to one of high-volume efficiency. Today, the market for tramadol is dominated by generic players who compete on supply chain optimization and manufacturing scale. Investing in tramadol today is an investment in the “Value” category of stocks—companies that can produce millions of units with razor-thin margins and impeccable distribution.

Profit Margins in Synthetic Opioids

While the margins on generic tramadol are lower than branded alternatives, the sheer scale of the global pain management market—valued at over $70 billion—ensures that it remains a significant revenue driver. Synthetic opioids like tramadol are cheaper to produce than plant-derived opiates (like morphine or codeine), which are subject to agricultural volatility and complex extraction processes. The “synthetic” nature of tramadol allows for a more predictable cost of goods sold (COGS), a metric that CFOs and analysts watch closely when projecting quarterly earnings.

Risk Management and Liability in the Pharma Portfolio

No analysis of a drug’s financial standing is complete without addressing the “risk” side of the ledger. The classification of tramadol as an opioid places it within the broader context of the global opioid crisis, which has become a massive liability for the pharmaceutical industry.

Legal Contingencies and ESG Investing

In recent years, the “Social” component of ESG (Environmental, Social, and Governance) investing has become a primary driver of capital allocation. Companies heavily reliant on opioid sales have faced multi-billion dollar settlements. Even though tramadol is considered a “milder” opioid, it is not immune to litigation risk.

Institutional investors now conduct deep “litigation audits” before taking positions in companies that manufacture analgesics. They look at how a company classifies its risk and whether it has set aside adequate reserves for potential legal settlements. The financial health of a company is no longer just about its balance sheet; it’s about its “contingent liabilities.”

The Economic Cost of the Opioid Crisis

Beyond individual companies, the classification of drugs like tramadol has a macro-economic impact. The societal cost of addiction—including lost productivity, healthcare expenses, and law enforcement—is estimated in the trillions of dollars. For the “Money” conscious reader, this translates to potential tax increases, shifts in government healthcare spending (Medicare/Medicaid), and increased insurance premiums. Understanding the class of drug tramadol belongs to is therefore a prerequisite for understanding the systemic risks within the healthcare sector of the economy.

Future Trends: Investing in Non-Opioid Alternatives

The ultimate goal of pharmaceutical investing is to identify the “next big thing” before it reaches the market. As the risks associated with the opioid class of drugs increase, capital is aggressively flowing toward alternatives.

Biotech Innovation and R&D Capital

There is a massive “Greenfield” opportunity in non-opioid pain relief. Venture capital firms and biotech-focused ETFs are pouring billions into startups developing nerve growth factor (NGF) inhibitors and specialized ion channel blockers. The goal is to create a drug that has the efficacy of a Schedule IV analgesic like tramadol but without the “controlled substance” classification.

From a business perspective, the first company to successfully de-classify pain management—moving it from “controlled” to “non-addictive”—will likely see a market capitalization explosion similar to the early days of biotech pioneers.

Diversifying Your Healthcare Portfolio

For the individual investor, the story of tramadol suggests a need for diversification. Relying solely on “legacy” analgesics is risky. A balanced healthcare portfolio should include:

- Value Plays: Established generic manufacturers with high-volume distribution.

- Growth Plays: Biotech firms focused on non-addictive pain solutions.

- Hedge Plays: Healthcare providers and insurers that benefit from a shift toward lower-cost, lower-risk treatment modalities.

Conclusion: The Bottom Line on Drug Classification

What class of drug is tramadol? In the pharmacy, it is a Schedule IV opioid. In the world of money and finance, it is a high-volume, low-margin commodity that carries significant regulatory and litigation risk.

For the astute investor, tramadol serves as a reminder that pharmaceutical assets are governed by more than just clinical trials; they are shaped by the invisible hand of government regulation, the legal system, and the shifting tides of social responsibility. Whether you are analyzing a pharmaceutical stock for a retirement account or evaluating the business model of a medical startup, understanding the classification of the products involved is the first step toward making an informed, profitable decision in the complex world of healthcare finance.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.