In the landscape of American personal finance, few events carry as much weight—or as much risk—as a change in marital status. While the question “what’s the divorce rate in the US?” is often posed as a sociological inquiry, it is increasingly becoming a critical metric for financial planners, wealth managers, and individual investors. Statistically, the narrative that “half of all marriages end in divorce” has evolved into a more nuanced reality, shaped heavily by socioeconomic standing, education, and financial literacy.

Understanding the current divorce rate is no longer just about tracking social trends; it is about understanding the economic volatility that defines modern American life. When a legal union dissolves, it is essentially the liquidation of a joint venture. For the individuals involved, the stakes include the division of 401(k) plans, the forced sale of real estate, and the potential disruption of long-term investment strategies.

The Economics of the Modern Marriage Contract

The traditional view of marriage has shifted from a social necessity to what economists often call an “aspirational good.” This shift has a direct impact on the divorce rate. Today, marriage is frequently delayed until both partners have reached a level of financial stability, which has, paradoxically, led to a decline in divorce rates among younger generations compared to their predecessors.

Shifting Demographics and Financial Independence

The “divorce gap” is a phenomenon where the rate of marital dissolution is significantly lower for those with higher levels of education and higher income brackets. From a money perspective, this suggests that financial security acts as a shock absorber for marital stress. When a household possesses a robust emergency fund and diversified income streams, the external pressures of inflation or job loss are less likely to fracture the partnership. Conversely, in lower-income brackets, the divorce rate remains higher, often exacerbated by the “debt-stress” cycle.

The Cost of “I Do” vs. the Price of “I Don’t”

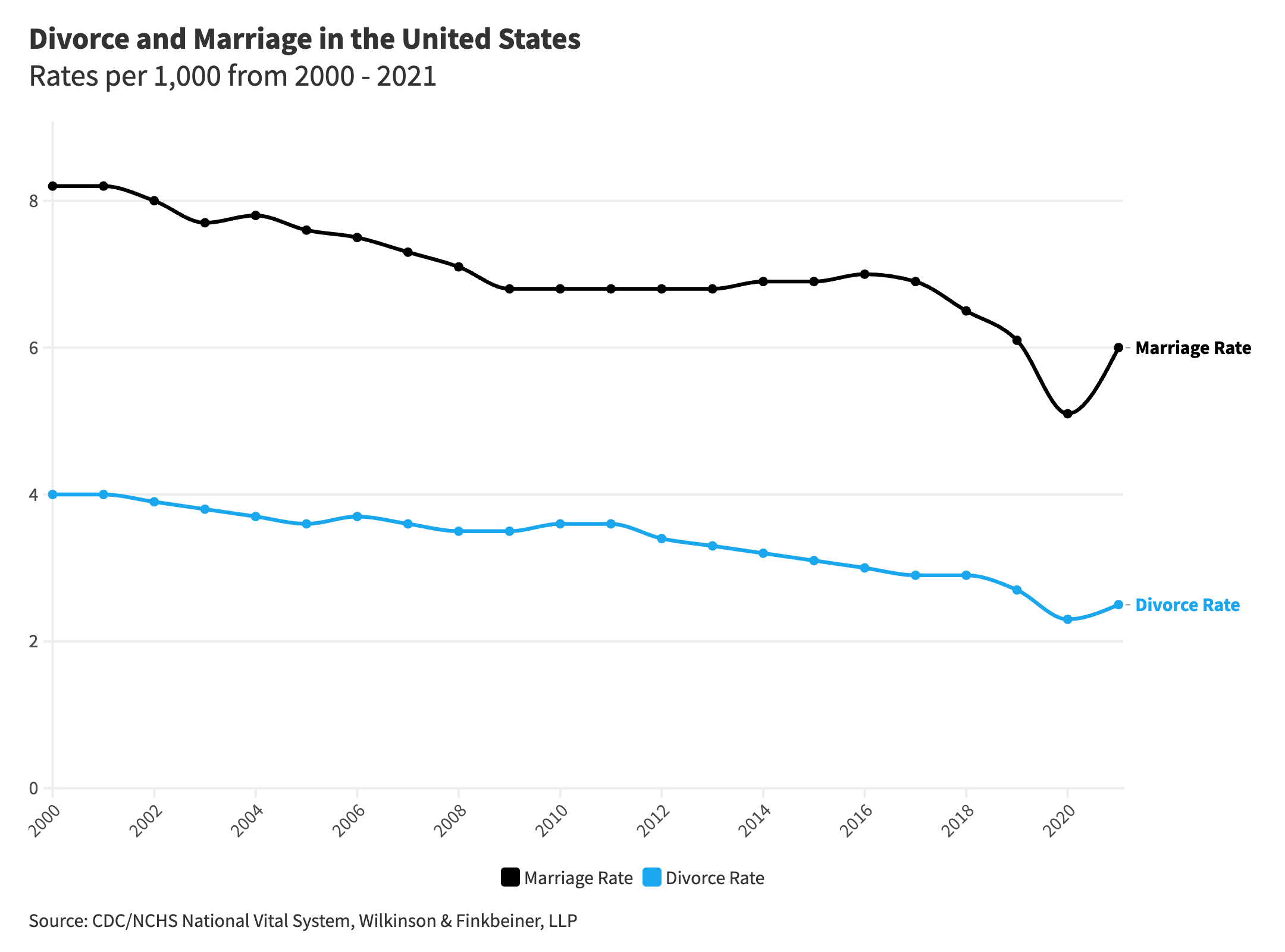

We must look at marriage as a financial merger. The current US divorce rate, which hovers around 14 to 15 divorces per 1,000 married women, represents a significant volume of capital reallocation. The cost of the average divorce in the United States ranges from $15,000 to $20,000 in legal fees alone, but the true “price” is the lost opportunity cost of compounded interest on divided assets. When a $500,000 retirement portfolio is split in two, both parties lose the logarithmic growth potential of the original sum, often setting their retirement clocks back by a decade or more.

Analyzing the 50% Myth: Data-Driven Financial Realities

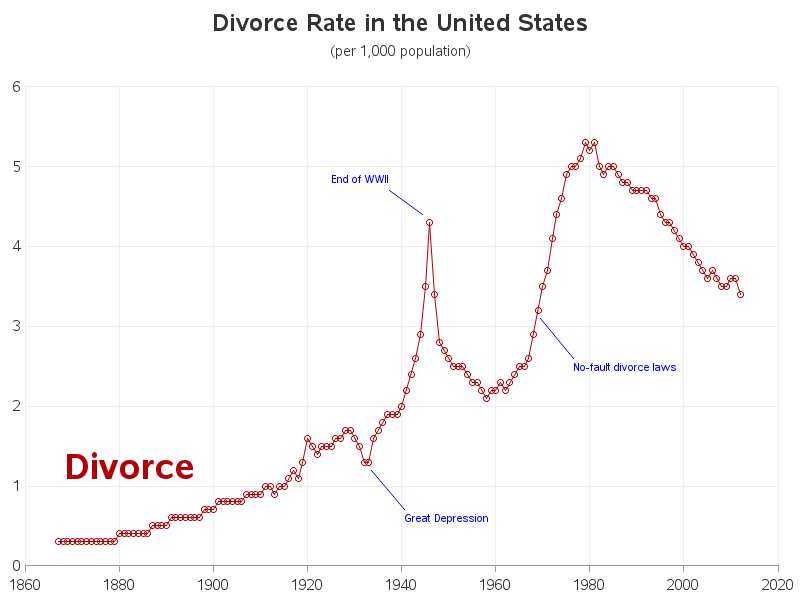

The pervasive statistic that 50% of marriages end in divorce is a relic of the late 1970s and early 1980s. In the current economic climate, the rate has actually been on a steady decline for over two decades. However, this macro-level decline masks micro-level financial vulnerabilities that every investor should understand.

Socioeconomic Status as a Predictor of Stability

Data from the U.S. Census Bureau suggests that wealth is one of the strongest predictors of marital longevity. Households with an annual income of over $75,000 are statistically less likely to divorce than those earning under the median. This creates a “wealth-stability feedback loop”: wealth leads to more stable marriages, and stable marriages allow for the long-term accumulation of wealth through dual-income advantages and shared tax liabilities.

The Impact of Financial Literacy on Marital Longevity

A significant portion of marital friction stems from “financial infidelity” or divergent spending habits. The divorce rate is notably lower among couples who engage in transparent financial planning. When we analyze the reasons for the current divorce rate, “money fights” consistently rank in the top three. Therefore, the divorce rate is not just a social statistic; it is a reflection of the national state of financial literacy. Couples who understand the mechanics of budgeting, investing, and debt management are effectively “hedging” against the risk of divorce.

The “Gray Divorce” Phenomenon and Retirement Security

While the overall divorce rate in the US is declining, there is one demographic where it is surging: adults over the age of 50. Often referred to as “Gray Divorce,” this trend has devastating implications for personal finance and retirement security.

Splitting the Nest Egg: Retirement Accounts and Pensions

In a gray divorce, there is less time to recover from the financial hit. The division of a 401(k) or a traditional pension plan via a Qualified Domestic Relations Order (QDRO) is a complex process that can trigger unforeseen taxes and penalties if not handled with precision. For those nearing retirement, the divorce rate represents a literal halving of their expected lifestyle. The economy of scale—where two people live more cheaply together than apart—evaporates, leading to a “doubling” of cost-of-living expenses during years when income is typically fixed.

Real Estate Liquidation in a High-Interest Market

For most American couples, the primary residence is their largest asset. In the context of a divorce, the home must either be sold or one partner must “buy out” the other. In the current high-interest-rate environment, refinancing a mortgage to remove a spouse’s name can mean jumping from a 3% rate to a 7% rate. This financial friction is currently acting as a “lock-in” effect, where the high cost of debt is actually suppressing the divorce rate in certain markets because couples simply cannot afford to live separately.

Strategies for Financial Preservation Amidst Marital Transitions

Given that the divorce rate remains a statistically significant risk factor for any financial plan, proactive wealth management is essential. Approaching marriage with a “business mindset” does not diminish the emotional bond; rather, it protects both parties’ financial futures.

The Role of Prenuptial and Postnuptial Agreements

Once stigmatized, prenuptial agreements are now viewed as essential financial tools, particularly for individuals with pre-existing assets, business interests, or expected inheritances. A prenup acts as a “financial insurance policy,” dictating the terms of asset division and potentially avoiding the ruinous legal fees that drive the average cost of divorce so high. By defining “separate” vs. “marital” property early on, individuals can maintain the integrity of their investment portfolios regardless of the national divorce rate.

Navigating Tax Implications and Alimony

The Tax Cuts and Jobs Act of 2017 fundamentally changed the math of divorce. Alimony payments are no longer tax-deductible for the payer, nor are they considered taxable income for the recipient. This shift has made “buying out” a spouse more expensive for the higher earner. Understanding these tax tranches is vital for anyone looking at the divorce rate as part of their personal risk assessment. The goal of modern financial planning is to ensure that if a decoupling occurs, it is done with “tax efficiency,” minimizing the amount of wealth lost to the IRS during the transition.

The Long-Term ROI of Marital Stability

While much of the discussion around the divorce rate focuses on the cost of the split, it is equally important to highlight the “return on investment” (ROI) of a stable, long-term marriage. From a purely financial perspective, a successful marriage is one of the most effective wealth-building vehicles available.

Building Multi-Generational Wealth

The ability to pool resources, maximize tax-advantaged accounts (such as Spousal IRAs), and share the costs of child-rearing creates a massive tailwind for wealth accumulation. Couples who stay together benefit from “compounded stability.” They avoid the 15–30% “wealth haircut” that typically accompanies the legal dissolution of a household. When we look at the divorce rate, we are looking at the percentage of the population that loses this tailwind.

The Human Capital Factor

Finally, marriage provides a form of “internal insurance” against the loss of human capital. If one spouse becomes ill or loses a job, the other’s income provides a safety net that prevents the liquidation of long-term investments. This synergy is why, statistically, married individuals tend to have higher net worths than their single or divorced counterparts.

In conclusion, while the question “what’s the divorce rate in the US?” may seem like a simple data point, it is actually a complex indicator of economic health and personal financial risk. By treating marriage as a significant financial commitment and planning for the possibility of its dissolution with professional rigor, individuals can protect their path to financial independence. Whether the rate goes up or down, the strategy remains the same: transparency, literacy, and the proactive protection of assets.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.