In the modern financial landscape, managing multiple streams of debt is a common challenge for many individuals. From credit card balances and medical bills to student loans and personal lines of credit, the sheer volume of monthly due dates and varying interest rates can become overwhelming. This is where loan consolidation enters the conversation as a powerful financial tool. At its core, loan consolidation is the process of taking out a new loan to pay off several smaller debts, effectively merging them into a single monthly payment with a single interest rate.

While the concept sounds simple, the strategic execution of loan consolidation requires a deep understanding of interest structures, credit implications, and long-term financial planning. When done correctly, it can be the first step toward debt freedom; when misunderstood, it can lead to a cycle of deeper financial strain. This guide explores the mechanics, strategies, and psychological impacts of loan consolidation to help you determine if it is the right path for your personal finance journey.

The Mechanics of Loan Consolidation: How It Works

Loan consolidation is not debt “forgiveness”—it is debt restructuring. The fundamental goal is to simplify your liability portfolio. Instead of owing five different creditors at five different interest rates, you owe one lender a fixed amount.

The Aggregation Process

When you apply for a consolidation loan, the lender evaluates your total outstanding high-interest debt. If approved, the lender typically pays off your existing creditors directly, or provides you with the funds to do so yourself. Your previous accounts are brought to a zero balance, and you are left with one new loan. This new loan usually carries a fixed term (such as three or five years) and a fixed interest rate, providing a clear “light at the end of the tunnel.”

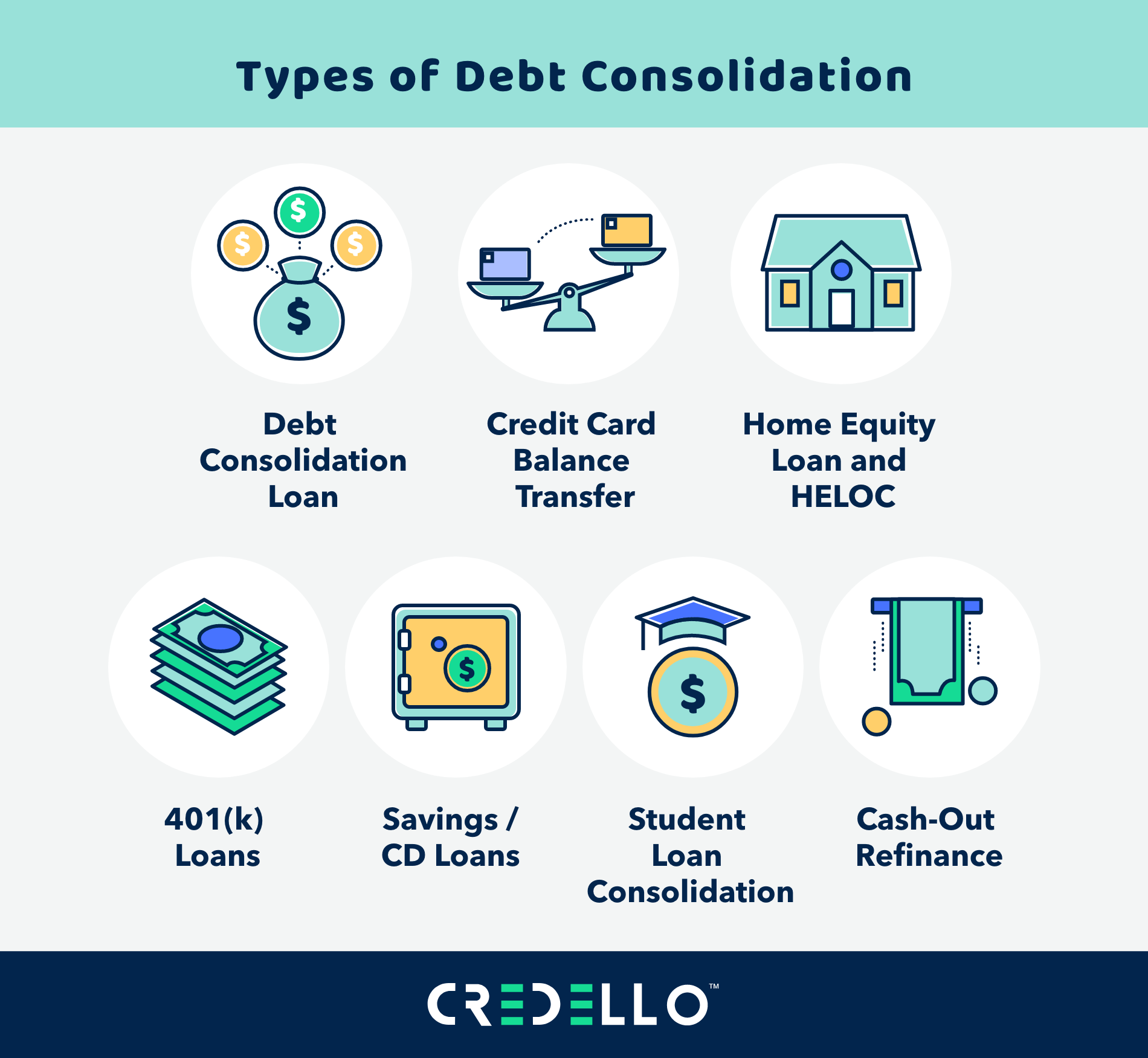

Types of Debt Eligible for Consolidation

Most unsecured debts can be consolidated. This includes:

- Credit Card Balances: Typically the primary target due to high APRs.

- Medical Bills: Often interest-free initially but can become burdensome if sent to collections.

- Personal Loans: Older loans with higher rates than what you might qualify for today.

- Payday Loans: High-interest short-term loans that benefit significantly from restructuring.

- Student Loans: Though federal and private student loans have specific consolidation programs separate from general personal finance tools.

Impact on Credit Scores

Initially, applying for a consolidation loan may cause a minor, temporary dip in your credit score due to a “hard inquiry.” However, in the medium to long term, consolidation often boosts credit scores. By paying off several credit cards, you significantly lower your credit utilization ratio—a key factor in credit scoring. Furthermore, replacing revolving debt (credit cards) with installment debt (a loan) can improve your “credit mix,” signaling to lenders that you can manage different types of credit responsibly.

Strategic Methods for Debt Consolidation

Choosing the right vehicle for consolidation is just as important as the decision to consolidate itself. Depending on your credit score and assets, different financial products offer varying levels of efficiency.

Unsecured Personal Loans

The most common method is obtaining an unsecured personal loan from a bank, credit union, or online lender. These do not require collateral (like a house or car). The interest rate is primarily determined by your creditworthiness. If you have a “Good” to “Excellent” credit score, you can often secure a rate significantly lower than the 20-25% APR typically found on credit cards.

Balance Transfer Credit Cards

For those with smaller amounts of debt and high credit scores, a balance transfer card can be an elite strategy. These cards offer a 0% introductory APR for a set period, usually 12 to 21 months. By transferring high-interest balances to this new card, 100% of your monthly payment goes toward the principal. However, caution is required: if the balance isn’t paid off before the intro period ends, the interest rate usually spikes to a high standard APR.

Home Equity Loans and HELOCs

Homeowners may choose to leverage their home’s equity to pay off high-interest debt. Because these loans are secured by real estate, they offer some of the lowest interest rates available. While this can save thousands in interest, it carries the highest risk: if you fail to make payments, you could face foreclosure. This method should only be used by those with a stable income and a disciplined budget.

The Financial Benefits vs. Potential Pitfalls

Evaluating loan consolidation requires a balanced look at how it changes your cash flow versus how it might impact your total interest paid over time.

Lowering Interest Rates and Monthly Payments

The primary financial driver for consolidation is the “Weighted Average Interest Rate.” If you have $10,000 in debt at 24% APR and you consolidate it into a loan at 10% APR, you are drastically reducing the “cost of money.” This often results in a lower monthly payment, which frees up cash flow for daily living expenses or an emergency fund.

The Psychological Benefits of a Single Payment

Financial stress is often exacerbated by complexity. Managing multiple logins, passwords, and due dates increases the risk of a missed payment and subsequent late fees. Consolidation provides psychological relief by reducing the mental load to one single transaction per month. This simplicity helps many individuals stay committed to their debt-repayment plan.

Hidden Costs: Fees and Extended Terms

One must be wary of “loan term extension.” If you consolidate a debt that was set to be paid off in two years into a new five-year loan, you might end up paying more in total interest over the life of the loan, even if the interest rate is lower. Additionally, many consolidation loans come with “origination fees” ranging from 1% to 8% of the loan amount. It is essential to calculate the “effective APR,” which includes these fees, to ensure the consolidation is truly saving you money.

When is the Right Time to Consolidate?

Consolidation is a tool, not a cure. Its effectiveness depends entirely on your financial behavior and the current economic climate.

Evaluating Your Credit Profile

The best time to consolidate is when your credit score has improved since you originally took out your debts. If your score has jumped from 600 to 720, you are now eligible for “prime” rates that were previously unavailable. If your credit score is currently poor, you might only qualify for consolidation loans with high interest rates, which defeats the purpose of the strategy.

Calculating the Break-Even Point

Before signing a loan agreement, perform a break-even analysis. Total the interest you would pay on your current debts over their remaining lifespans. Then, compare that to the total interest and fees of the new consolidation loan. If the new loan doesn’t save you a significant amount of money or provide necessary breathing room in your monthly budget, it may be better to stick with your current repayment plan.

Avoiding the “Debt Cycle” Trap

The most dangerous pitfall of loan consolidation is the “empty card” syndrome. Once a consolidation loan pays off your credit cards, those cards now have zero balances. Many people make the mistake of using those cards again for new purchases while still paying off the consolidation loan. This leads to “double debt.” Successful consolidation requires a lifestyle change where credit cards are either hidden away or used only for small, trackable expenses that are paid off in full every month.

Conclusion: A Path Toward Financial Sovereignty

Loan consolidation is a sophisticated financial maneuver that can streamline your path to debt freedom. By converting high-interest, chaotic debt into a structured, lower-interest installment plan, you gain both a mathematical advantage and emotional peace of mind. However, the tool is only as effective as the person using it.

To truly succeed with consolidation, one must address the underlying habits that led to the debt in the first place. When paired with a strict budget and a commitment to avoid new high-interest liabilities, loan consolidation acts as a powerful catalyst for wealth building. It clears the administrative and financial hurdles, allowing you to focus your energy on what truly matters: building an emergency fund, investing for the future, and achieving long-term financial sovereignty.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.