The statistic that “50% of marriages end in divorce” has become a staple of American cultural shorthand. While often quoted in casual conversation, this figure carries profound weight within the realm of personal finance and wealth management. In the United States, marriage is not only a social contract but a significant financial partnership. Consequently, the dissolution of that partnership represents one of the most volatile economic events an individual can experience.

Understanding the current percentage of marriages that end in divorce is the first step in assessing the broader landscape of American financial stability. Current data suggests that while the 50% mark remains a general benchmark, the reality is more nuanced, influenced heavily by age, education, and socioeconomic status. Regardless of the exact percentage, the financial implications—ranging from the division of complex investment portfolios to the restructuring of retirement plans—necessitate a rigorous examination of divorce through a purely economic lens.

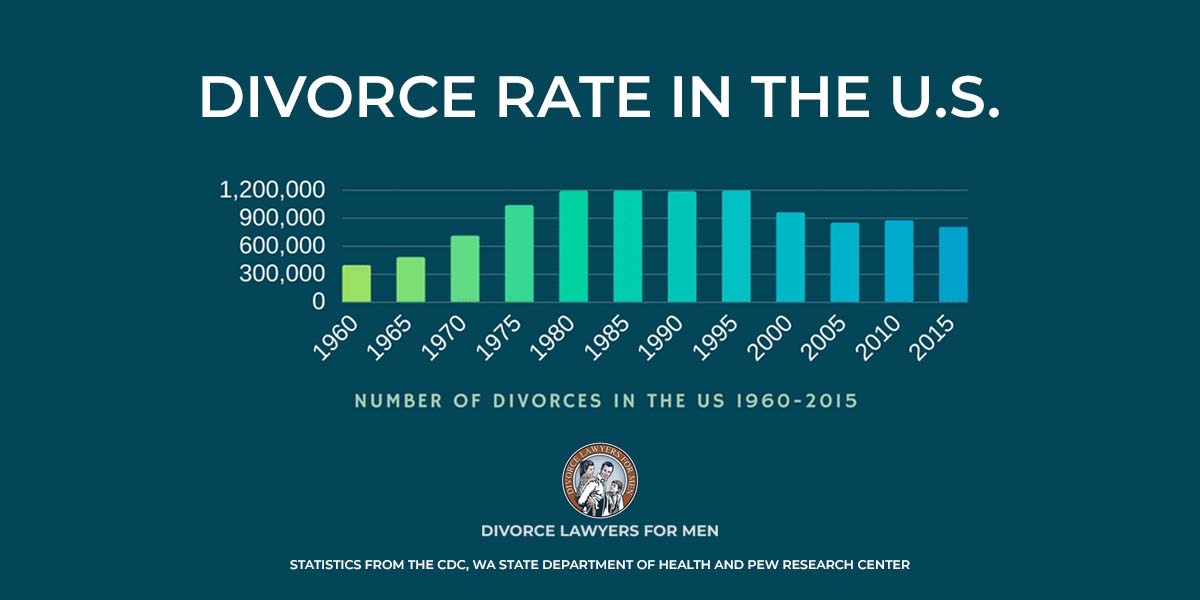

Understanding the “50% Myth”: Current Divorce Trends and Demographics

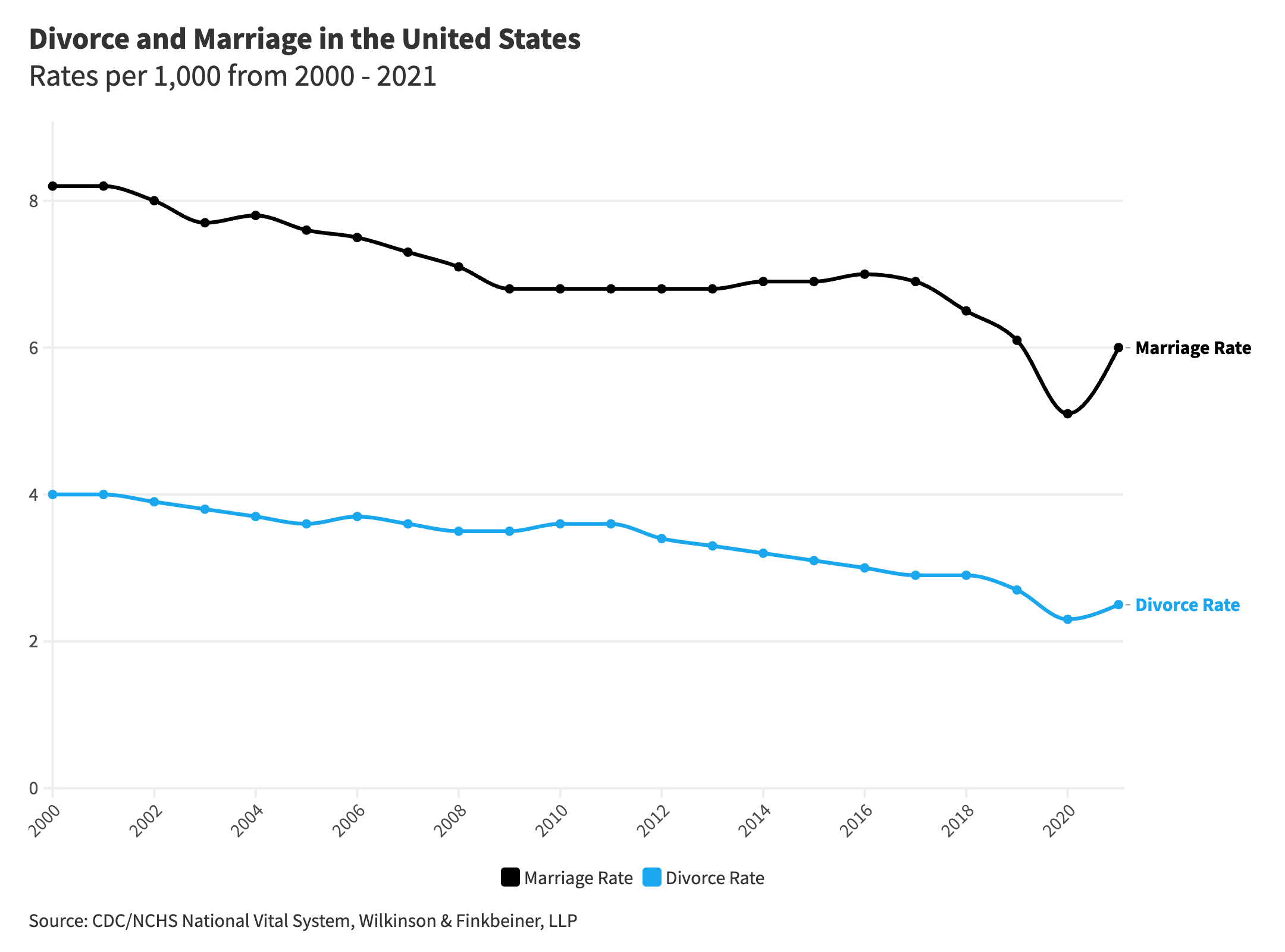

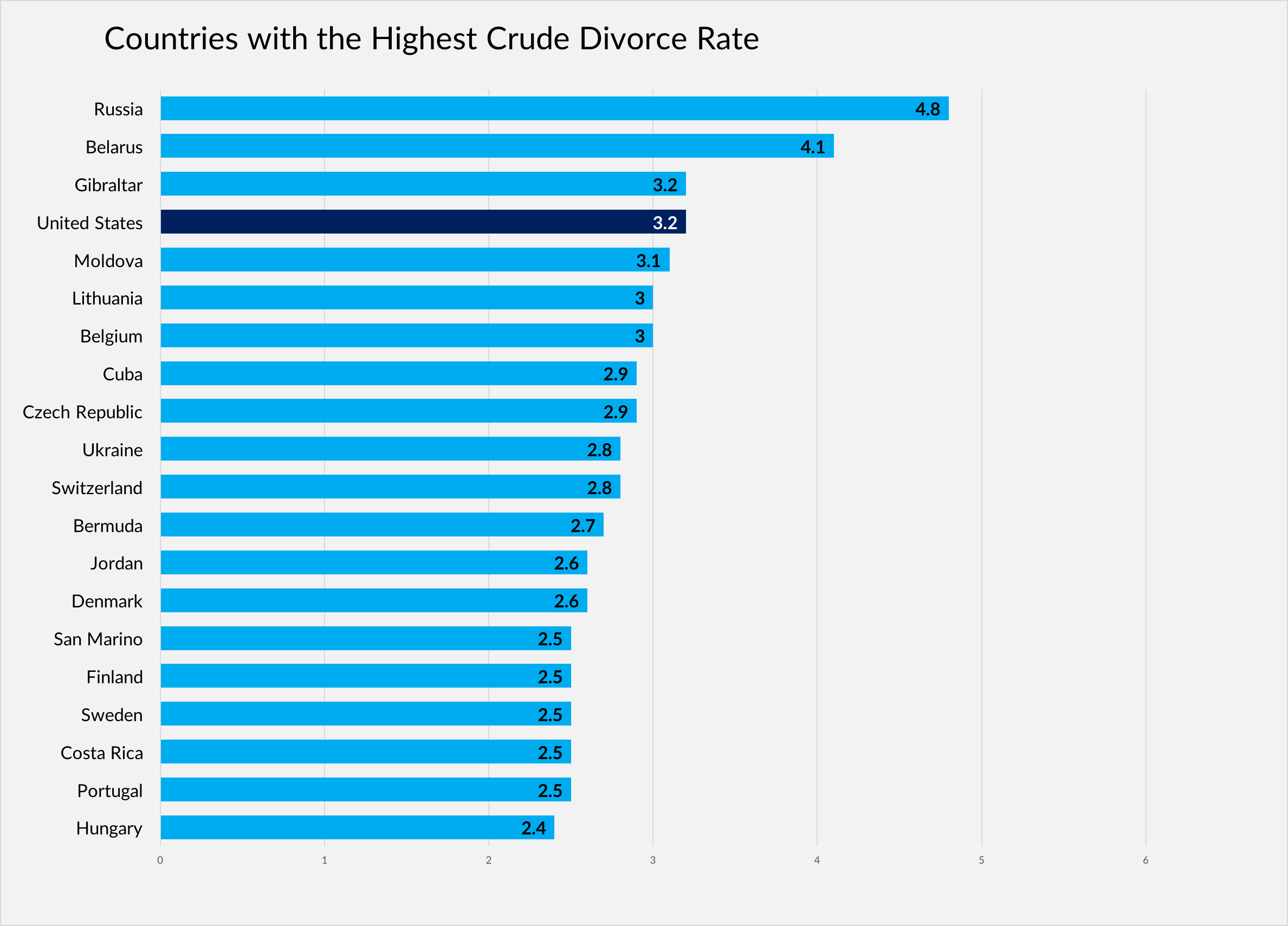

To analyze the financial impact of divorce, one must first understand the current statistical landscape. While the oft-cited 50% divorce rate was largely accurate for those married in the 1970s and 80s, the trajectory for modern marriages has shifted. For first-time marriages occurring today, the projected divorce rate is actually closer to 39% to 43%. However, this downward trend is not uniform across all demographics, and the financial stakes have never been higher.

The Statistical Reality of Modern Marriage

Demographers note that divorce rates in America have been steadily declining since their peak in the early 1980s. This decline is largely attributed to “delayed marriage”—the trend of younger generations, specifically Millennials, waiting until they are more financially established to wed. From a money perspective, this means that when marriages do occur, they often involve more significant pre-existing assets and higher levels of debt, such as student loans. The “success rate” of marriage is increasingly correlated with educational attainment and income levels, suggesting that financial security is a primary stabilizer of the marital unit.

The Rise of the “Gray Divorce”

While divorce rates are falling among younger cohorts, they are doubling for those over the age of 50. This phenomenon, known as “Gray Divorce,” presents a unique and harrowing financial challenge. Unlike younger couples who have decades to recoup their losses, older Americans facing divorce must navigate the division of a lifetime’s worth of accumulated wealth—including pensions, 401(k)s, and primary residences—at a time when their earning potential is typically declining. This shift has significant implications for the American economy, as it creates a surge in single-person households among a demographic that was previously benefiting from the economies of scale inherent in a dual-income retirement.

The Economic Consequences of Dissolution

Divorce is frequently cited as one of the most effective ways to erode personal net worth. Beyond the immediate legal costs, the transition from a single household to two separate households creates a massive surge in cost-of-living expenses. For many Americans, the end of a marriage marks the end of financial upward mobility for several years, as assets are liquidated and recurring expenses double.

Immediate Impact on Liquidity and Cash Flow

The most immediate financial shock of a divorce is the disruption of cash flow. In a dual-income household, fixed costs such as mortgages, utilities, and insurance are shared. Upon separation, each individual must suddenly cover these costs independently. Research indicates that women, in particular, often experience a significant drop in their standard of living—sometimes as much as 30% to 45%—immediately following a divorce. Men also see a decline, though often less severe in the long term, primarily due to the loss of shared expenses and the potential imposition of alimony or child support payments.

Long-term Wealth Erosion and the “Divorce Penalty”

The “divorce penalty” refers to the long-term reduction in wealth accumulation compared to those who remain married. When a couple divorces, they are not simply splitting an egg in half; they are often cracking it. The liquidation of assets to satisfy a settlement often triggers capital gains taxes and early withdrawal penalties for retirement accounts. Furthermore, the loss of “economies of scale”—the ability to buy in bulk, share a single high-speed internet plan, or utilize a single family health insurance policy—adds up to hundreds of thousands of dollars over a lifetime. This erosion of capital makes it significantly harder for divorced individuals to reach the same retirement milestones as their married counterparts.

The Business of Divorce: Legal Fees and Asset Division

From a financial standpoint, a divorce is essentially the court-supervised liquidation of a small-to-medium-sized enterprise. The process of untangling years of co-mingled finances is both complex and expensive. The percentage of wealth lost to the “process” of divorce itself is a critical variable that many fail to account for when looking at the initial 50% statistic.

Evaluating Marital vs. Separate Property

One of the most contentious and financially significant aspects of divorce is the classification of assets. In “Community Property” states, all assets acquired during the marriage are generally split 50/50. In “Equitable Distribution” states, the split is based on what the court deems fair, which may not necessarily be equal. The financial complexity arises when separate property (assets owned before the marriage) becomes “transmuted” into marital property. For example, if an individual uses an inheritance to pay down the mortgage on a shared home, that “separate” money may suddenly be subject to a 50% claim by the spouse. High-net-worth individuals must employ forensic accountants to trace the flow of funds, adding further to the professional fees associated with the split.

Mediation vs. Litigation Costs

The method chosen to settle a divorce has a direct impact on the final balance sheet. A contested divorce involving litigation can easily cost each party between $15,000 and $100,000 in legal fees, effectively incinerating a large portion of the marital estate. Conversely, mediation and collaborative divorce models focus on preserving the “pie” rather than fighting over the crumbs. From a purely financial management perspective, mediation is the preferred route, as it minimizes the “leakage” of assets to third-party professionals (lawyers, expert witnesses, and court fees).

Financial Planning Strategies for Post-Divorce Recovery

Once the divorce is finalized and the percentage of assets has been distributed, the focus must shift to rebuilding. A post-divorce financial plan is not merely a revision of a previous plan; it is a total overhaul of one’s economic identity.

Retirement Accounts and the Power of the QDRO

One of the most critical tools in the financial aftermath of a divorce is the Qualified Domestic Relations Order (QDRO). This legal instrument allows for the tax-free transfer of retirement assets from one spouse to another. Without a QDRO, withdrawing funds from a 401(k) to pay a settlement would result in immediate income tax and a 10% early withdrawal penalty. Understanding the nuances of the QDRO is essential for preserving the “time value of money” and ensuring that the recipient spouse has a viable path to retirement.

Budgeting for a Single-Income Household

Rebuilding wealth requires a rigorous return to budgeting basics. The first step is often a “lifestyle audit” to align current spending with a single-income reality. This often involves downsizing the primary residence—a move that, while emotionally difficult, can unlock significant equity and reduce monthly overhead. Additionally, divorced individuals must re-evaluate their risk tolerance and insurance needs. Without a spouse to provide a “safety net” in the event of job loss or illness, increasing an emergency fund to cover 6–12 months of expenses becomes a financial priority.

Strategic Investing in the “Second Act”

As the statistics show, a significant percentage of Americans will experience divorce at least once. While the financial toll is undeniable, it also offers an opportunity for a “financial reset.” Freed from the constraints of a partner’s differing risk tolerance or spending habits, many individuals find they are able to manage their portfolios more aggressively or efficiently.

Strategic investing post-divorce involves a thorough review of beneficiary designations on all accounts, a re-assessment of tax-advantaged investment vehicles, and a renewed focus on individual financial goals. For many, the “business of being single” allows for a more streamlined approach to wealth building. By understanding the data behind divorce and the economic mechanics of asset division, individuals can navigate this transition not as a financial ending, but as a complex restructuring of their personal balance sheet. In the landscape of American finance, divorce is a risk that must be managed with the same professional rigor as any other market volatility.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.