In the landscape of modern business finance and corporate governance, risk management is often viewed through the lens of market volatility, credit defaults, or cybersecurity breaches. However, one of the most significant financial liabilities a company faces resides within a single, broadly interpreted sentence of the Occupational Safety and Health Act of 1970: the General Duty Clause. For business owners, financial officers, and risk managers, understanding the General Duty Clause is not merely a matter of regulatory compliance; it is a critical component of protecting the organization’s bottom line, managing insurance premiums, and safeguarding corporate valuation.

The Financial Stakes of Safety Compliance

The General Duty Clause, specifically Section 5(a)(1) of the OSHA Act, states that each employer “shall furnish to each of his employees employment and a place of employment which are free from recognized hazards that are causing or are likely to cause death or serious physical harm.” While this sounds straightforward, its breadth creates a unique financial challenge. Unlike specific standards that dictate the height of a guardrail or the concentration of a chemical, the General Duty Clause is a “catch-all” provision. From a financial perspective, this represents an “unquantified liability”—a risk that exists even when all specific regulations are met.

Understanding the Mechanics of Section 5(a)(1)

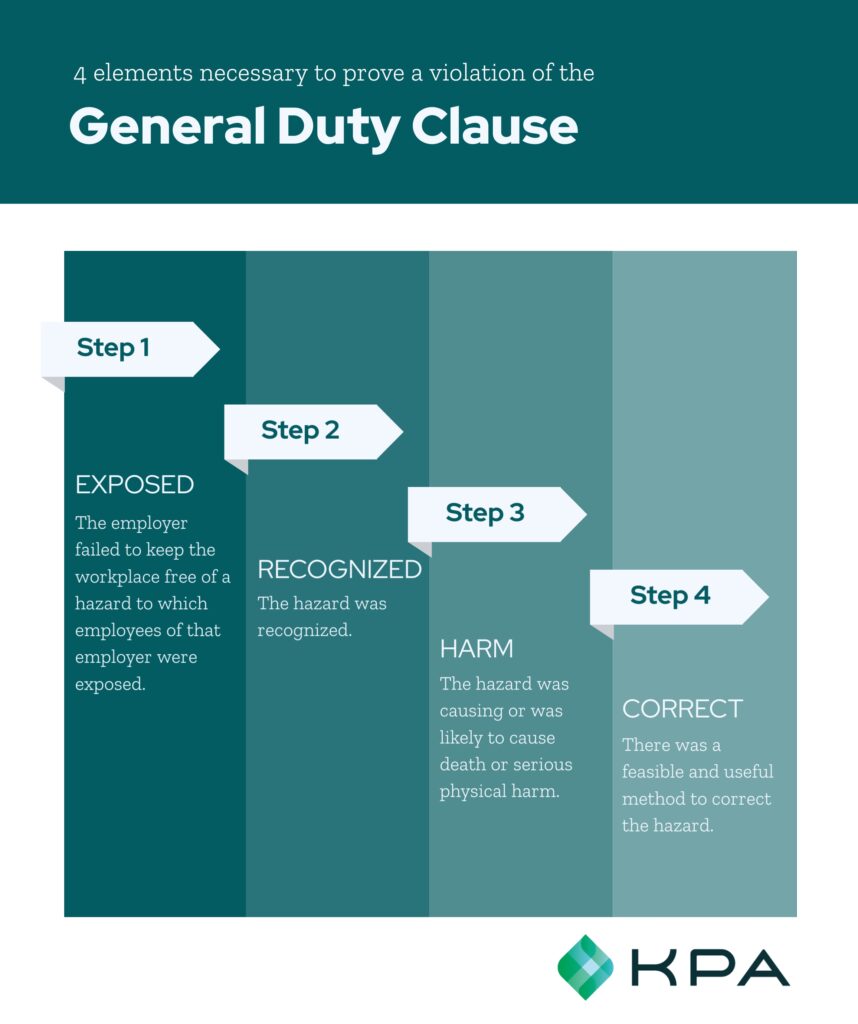

To appreciate the fiscal impact, one must understand when the clause is invoked. For a violation to occur, four elements must be present: the employer failed to keep the workplace free of a hazard to which employees were exposed; the hazard was recognized; the hazard was causing or likely to cause death or serious physical harm; and there was a feasible and useful method to correct the hazard.

For a business, the ambiguity of “recognized hazards” is where the financial risk lies. Hazards can be recognized through industry standards, internal company memos, or even common knowledge. If an emerging threat—such as ergonomic strain or extreme heat—is recognized by the industry but not yet codified into a specific regulation, the General Duty Clause allows regulators to issue citations. These citations carry heavy fines, but the secondary costs of litigation and remedial measures often dwarf the initial penalty.

The Hidden Costs of Workplace Incidents

When a company is cited under the General Duty Clause, the immediate financial penalty is often just the beginning. The “iceberg effect” of workplace safety costs suggests that for every dollar spent on direct costs (fines and medical expenses), there are several dollars in indirect costs. These include:

- Operational Downtime: Investigations can halt production lines for days or weeks.

- Administrative Overhead: The time spent by management and legal teams to address the citation and implement a “feasible” abatement plan.

- Employee Replacement: Recruiting and training new staff if an incident leads to turnover or long-term disability.

Risk Management as a Financial Asset

Proactive management of the General Duty Clause should be viewed as an investment rather than an expense. By treating safety as a core financial metric, organizations can transform a potential liability into a competitive advantage. The goal of a CFO or risk officer is to move from reactive spending (paying fines) to proactive capital allocation (preventative measures).

Identifying “Recognized Hazards” Through Financial Audits

The first step in mitigating the financial exposure of the General Duty Clause is a rigorous hazard assessment. In the world of business finance, this is akin to a due diligence process. Companies must look beyond existing OSHA checklists and analyze industry trends. For example, workplace violence and heat-related illnesses have recently become high-priority areas for General Duty Clause enforcement.

Investing in a professional safety audit may require upfront capital, but it provides a roadmap for “feasible” corrections. By documenting these hazards and the steps taken to mitigate them, a company builds a “good faith” defense. In the eyes of both regulators and insurers, a company that demonstrates a proactive approach to uncodified hazards is a much lower risk profile, directly influencing the company’s cost of capital.

Budgeting for Proactive Safety Systems

Effective financial planning requires a dedicated budget for safety technology and training. This is not just about “buying gear”; it is about implementing systems that provide data. Modern safety software can track “near-miss” incidents, providing a predictive look at where a General Duty Clause violation might occur.

From a financial standpoint, these investments are highly ROI-positive. Reducing the frequency of incidents directly lowers the Total Cost of Risk (TCOR). Furthermore, capital improvements aimed at safety—such as improved ventilation systems or automated machinery—often have the side effect of increasing operational efficiency, providing a double benefit to the corporate ledger.

The Impact on Corporate Valuation and Insurance

In the modern economy, a company’s value is increasingly tied to its ESG (Environmental, Social, and Governance) performance. The “Social” and “Governance” components are deeply intertwined with how a company manages its general duty to its workforce. Investors and insurers use these metrics to determine the long-term viability and risk level of a business.

Workers’ Compensation and Insurance Premiums

One of the most direct financial links to the General Duty Clause is the Experience Modification Rate (EMR). The EMR is a multiplier used by insurance companies to calculate workers’ compensation premiums. A company with a history of safety incidents—even those not covered by specific regulations but fall under the General Duty Clause—will see their EMR rise.

An EMR above 1.0 signifies a higher-than-average risk, leading to significantly higher premiums. Conversely, an EMR below 1.0 can save a company hundreds of thousands of dollars annually. For businesses in high-risk industries like construction or manufacturing, a high EMR can even prevent them from bidding on lucrative contracts, directly impacting revenue growth and market share.

Brand Equity and Investor Relations

Beyond the balance sheet, a General Duty Clause citation can cause irreparable harm to a brand’s reputation. In an era of instant information, news of “unsafe working conditions” can lead to consumer boycotts, difficulty in talent acquisition, and a drop in stock price.

Institutional investors are increasingly scrutinizing safety records as part of their risk assessment. A pattern of relying on the “lack of specific regulations” to avoid safety investments is seen as a sign of poor management. On the other hand, a robust safety culture protected by a deep understanding of general duties signals to the market that the company is stable, ethically managed, and prepared for the future.

Navigating the Legal and Financial Labyrinth

The General Duty Clause is often the center of complex legal disputes. When a company is cited, the financial decision-makers must weigh the cost of a settlement against the cost of a legal challenge. This requires a nuanced understanding of “economic feasibility.”

Feasibility and Economic Burden

One of the defenses against a General Duty Clause citation is that the proposed abatement method is not “feasible.” In legal and financial terms, feasibility is split into two categories: technological and economic.

Economic feasibility does not mean the company simply doesn’t want to pay; it means that the cost of the safety measure would threaten the very survival of the company or the industry. However, courts rarely accept this defense unless the financial burden is truly catastrophic. Therefore, businesses must prepare for the reality that if a hazard is recognized, the financial system must find a way to fund the remedy. Integrating these potential costs into long-term financial forecasting is essential for maintaining liquidity.

Future-Proofing the Business Against Regulatory Shifts

The General Duty Clause is a dynamic instrument. As technology evolves and new health data emerges, the definition of a “recognized hazard” shifts. For example, as we enter the era of AI and advanced robotics in the workplace, new hazards regarding human-machine interaction are surfacing. These are not yet codified in specific OSHA standards, but they fall squarely under the General Duty Clause.

To future-proof the organization’s finances, leaders must stay ahead of the regulatory curve. This involves:

- Engagement with Industry Associations: Understanding what peers are recognizing as hazards to avoid being the “outlier” in a legal case.

- Continuous Training: Allocating funds for ongoing education so that the workforce is the first line of defense against emerging risks.

- Legal Reserves: Maintaining a contingency fund for regulatory shifts and potential compliance upgrades.

In conclusion, the General Duty Clause is far more than a safety guideline; it is a fundamental pillar of business finance and risk management. By acknowledging the broad reach of this clause, executives can better protect their organizations from unforeseen liabilities, optimize their insurance costs, and build a resilient brand that attracts both investors and top-tier talent. In the modern business world, the safest companies are often the most profitable ones.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.