In the realm of personal finance, few topics are as critical yet as frequently overlooked as estate planning. While many individuals focus their energy on wealth accumulation, portfolio diversification, and tax optimization, the ultimate distribution of those assets remains a secondary thought. This brings us to a pivotal legal and financial concept: intestate succession.

At its core, intestate succession is the statutory process that dictates how a person’s assets are distributed when they pass away without a valid last will and testament. In financial circles, dying “intestate” is often viewed as a significant failure of financial management, as it strips the individual of their agency and places the fate of their life’s work in the hands of rigid state laws. Understanding the nuances of this process is essential for anyone looking to secure their financial legacy and protect their heirs from unnecessary hardship.

The Financial Mechanics of Intestate Succession

When an individual dies without a will, they are said to have died “intestate.” In such cases, the local probate court steps in to oversee the distribution of the estate. This is not an arbitrary process; it is governed by specific state or regional laws designed to provide a default framework for the transfer of property. However, “default” rarely means “optimal” in a financial context.

The Hierarchy of Asset Distribution

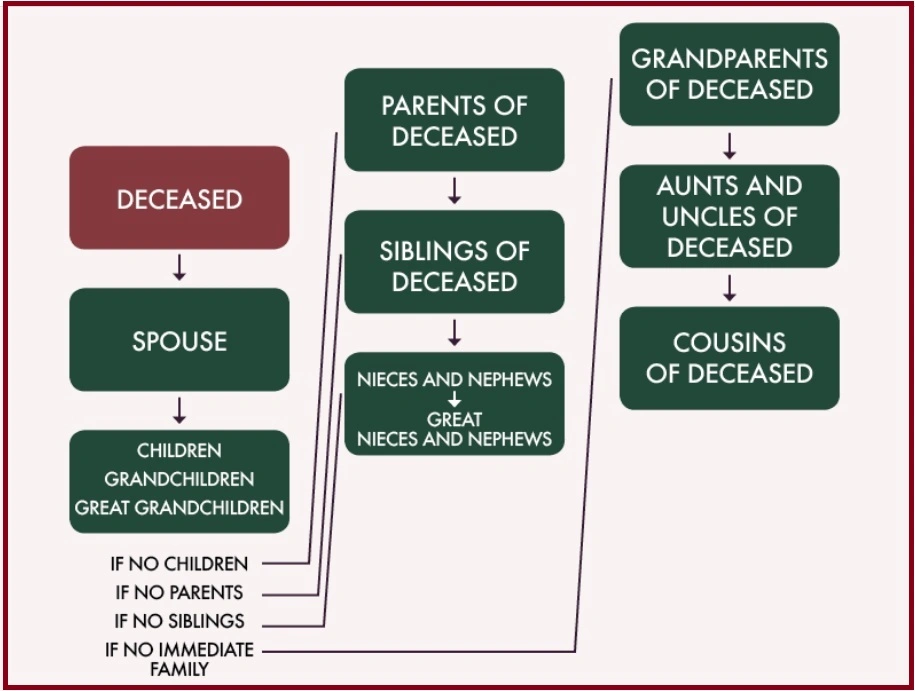

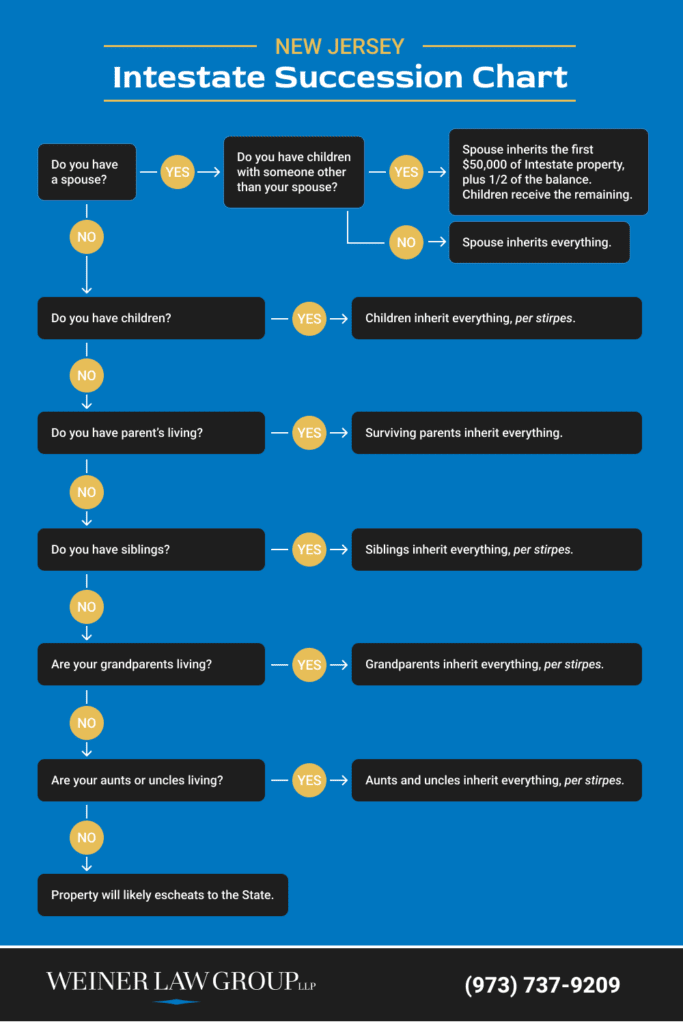

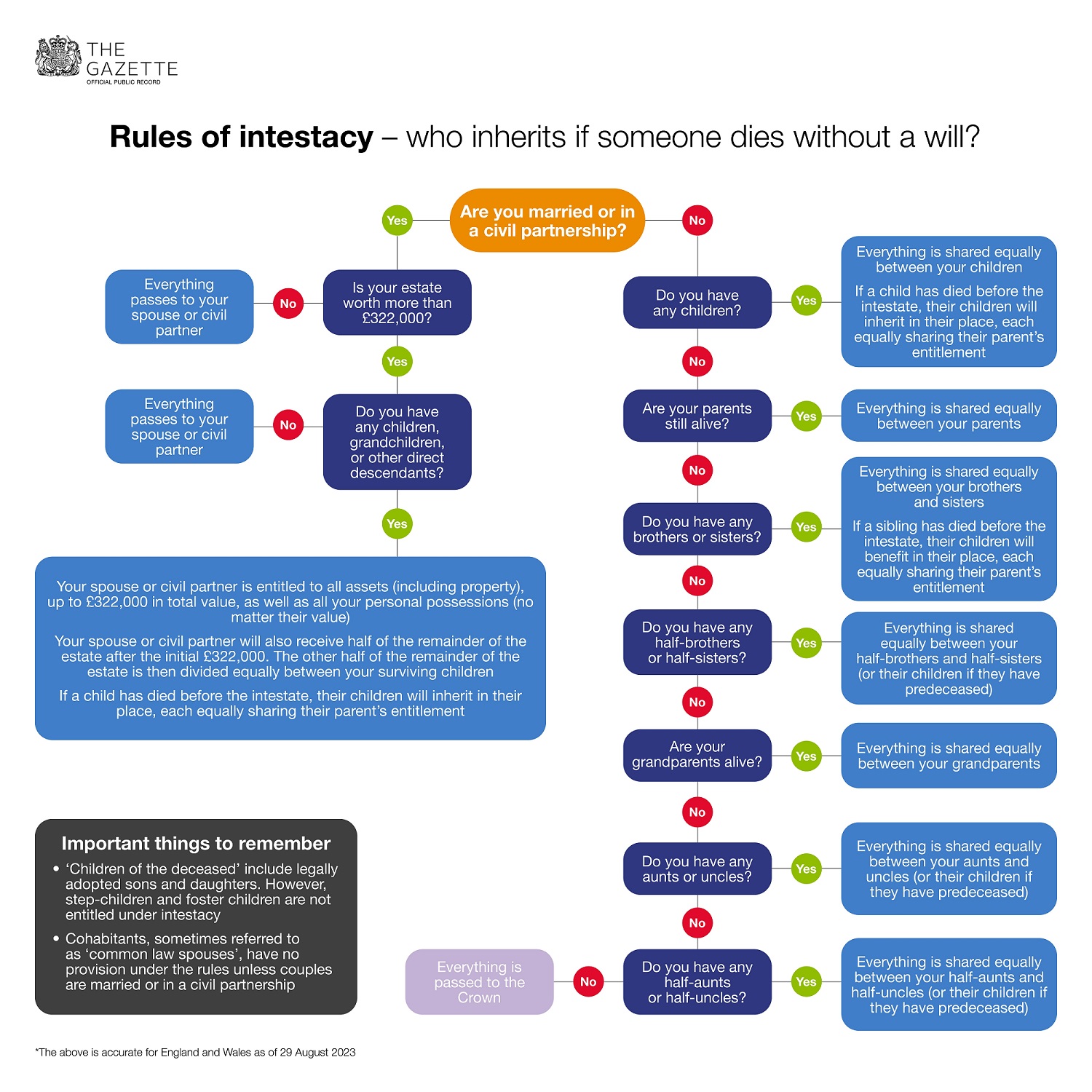

Intestacy laws follow a strict hierarchy of beneficiaries, often referred to as “degrees of kinship.” The primary goal of these statutes is to pass assets to the closest living relatives. Generally, the spouse and children are the first in line. If a decedent is survived by a spouse but no children, the spouse typically inherits the entire estate. If there are children but no spouse, the children share the estate equally.

Complexity arises when there are both a surviving spouse and children from different marriages, or when the deceased leaves behind only distant relatives like cousins or nieces. From a personal finance perspective, this rigid hierarchy can lead to unintended outcomes. For instance, a long-term domestic partner who was not legally married to the deceased may be left with zero financial support, as intestacy laws rarely recognize non-legal partnerships.

The Probate Process and Financial Oversight

Intestate succession is facilitated through the probate court. Because there is no will to name an executor, the court must appoint an “administrator” to manage the estate’s financial affairs. This administrator is responsible for identifying assets, paying off debts, and distributing the remaining funds to the legal heirs.

This process is notoriously slow and transparent to the public. For those with significant financial holdings, the lack of privacy in probate can be a major disadvantage. Furthermore, the administrator appointed by the court may not be the person the deceased would have trusted to manage complex investment portfolios or sensitive business interests, potentially leading to the mismanagement of assets during the transition period.

The Financial Consequences of Lacking an Estate Plan

The decision to forgo a will is rarely a conscious choice; it is usually the result of procrastination. However, the financial implications of this procrastination are profound. Lacking an estate plan often results in the “erosion of the estate,” where a significant portion of the decedent’s wealth is consumed by avoidable costs.

Probate Costs and Administrative Delays

One of the most immediate impacts of intestate succession is the high cost of probate. Legal fees, court costs, and administrative expenses can quickly eat into the principal of an estate. In many jurisdictions, these fees are calculated as a percentage of the total estate value, meaning the more successful you are, the more the state and legal system take from your heirs.

Beyond the monetary cost, there is the “time value of money” to consider. Intestate estates often linger in probate for twelve to twenty-four months. During this time, assets may be frozen. Heirs who were dependent on the deceased for financial support may find themselves in a liquidity crisis, unable to access funds for daily living expenses or mortgage payments while the court navigates the complexities of kinship verification.

Tax Implications and Wealth Transfer Inefficiency

A well-crafted estate plan is a primary tool for tax mitigation. By using trusts and strategic gifting, individuals can minimize the impact of inheritance and estate taxes. When a person falls into intestate succession, these opportunities are lost.

In an intestate scenario, the transfer of wealth is blunt. There is no opportunity for “tax-loss harvesting” or the strategic distribution of high-basis versus low-basis assets to different heirs. For high-net-worth individuals, this lack of planning can result in a much larger tax bill for the estate, effectively gifting a portion of their hard-earned wealth to the government rather than their loved ones. Furthermore, many states have different tax rules for assets passing to spouses versus distant relatives; without a will to direct these flows, the tax outcome is left entirely to chance.

Strategic Asset Management and Protection

Intestate succession is particularly disruptive when the deceased owned complex assets, such as a family business, commercial real estate, or a diverse portfolio of alternative investments. In these cases, the financial damage extends beyond mere administrative fees; it can threaten the viability of the assets themselves.

Disruption of Business Continuity

For entrepreneurs and small business owners, their business is often their most valuable asset. If a business owner dies intestate, their shares or ownership interest are distributed according to the same rigid hierarchy as their personal bank accounts. This can lead to a disastrous situation where multiple family members—some of whom may have no interest or expertise in the industry—suddenly become co-owners of a functioning company.

Without a buy-sell agreement or a clear succession plan in a will, the business may face operational paralysis. Creditors may become wary, key employees might leave due to uncertainty, and the court-appointed administrator may lack the authority or knowledge to make critical management decisions. In many cases, the only way to resolve the conflict among heirs is to liquidate the business, often at a fire-sale price that fails to reflect its true market value.

Protecting Real Estate and Non-Liquid Assets

Real estate represents another challenge in intestate succession. If the deceased owned property in multiple states, a separate probate process (known as “ancillary probate”) may be required in each jurisdiction. This multiplies the legal fees and complicates the management of the property.

Furthermore, if an estate is divided among several heirs, they become “tenants in common” for any real estate involved. This means no single heir can sell or mortgage the property without the consent of the others. If the heirs disagree on the management of the property—one wants to rent it while another wants to sell—the asset can become a source of legal conflict and financial drain rather than a source of generational wealth.

Building a Robust Financial Legacy: Moving Beyond Intestacy

The risks associated with intestate succession highlight the necessity of proactive financial planning. A will is the foundation of an estate plan, but for those serious about wealth preservation, it is only the beginning.

Practical Steps to Formalizing Your Will

To avoid the pitfalls of intestacy, the first step is the creation of a legally binding will. This document should do more than just list heirs; it should name a competent executor who understands financial matters and can navigate the probate process efficiently. It should also include “simultaneous death” clauses and “contingent beneficiary” designations to ensure that the plan remains functional even in tragic or unforeseen circumstances.

From a financial perspective, a will allows for “specific bequests”—the ability to leave specific assets (like a family heirloom or a particular brokerage account) to specific people. This precision prevents the “selling off” of assets to facilitate an equal split, allowing the family to retain valuable or sentimental property.

The Role of Trusts and Beneficiary Designations

In modern financial planning, the goal is often to avoid probate—and thus intestate succession—altogether. This is achieved through the use of trusts and direct beneficiary designations.

A Revocable Living Trust is a powerful financial tool that allows assets to pass directly to beneficiaries upon death, bypassing the probate court entirely. This ensures privacy, reduces costs, and allows for much faster distribution of funds. Additionally, many financial accounts (such as 401(k)s, IRAs, and life insurance policies) allow for “Transfer on Death” (TOD) or “Payable on Death” (POD) designations. These designations override whatever is written in a will and certainly take precedence over intestate laws. Regularly reviewing and updating these designations is a crucial, yet simple, way to ensure that your financial engine keeps running smoothly for the next generation.

Conclusion: Securing Your Financial Legacy

Intestate succession is a reminder that in the world of personal finance, silence is a choice—and usually a costly one. By failing to document your wishes, you are effectively opting into a government-mandated financial plan that may not align with your values, your family’s needs, or the efficient management of your assets.

True financial success is measured not just by the wealth you accumulate, but by how well that wealth is protected and transitioned. Taking the time to understand the risks of intestacy and implementing a robust estate plan ensures that your life’s work serves its intended purpose: providing security, opportunity, and a lasting legacy for those you leave behind. Don’t let the state’s default laws be the final word on your financial history.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.