In the world of finance, precision is not just a preference; it is a necessity. When dealing with billions of dollars in trade volume or decades-long mortgage agreements, a mere fraction of a percentage point can represent a monumental shift in value. This is where the concept of “basis points” comes into play. Often abbreviated as “bps” and pronounced as “bips,” basis points are the universal language used by central bankers, investors, and lenders to describe changes in interest rates, bond yields, and financial percentages without the risk of ambiguity.

To the uninitiated, hearing that the Federal Reserve raised rates by “25 basis points” might sound like technical jargon. However, understanding this unit of measurement is fundamental for anyone looking to master their personal finances, evaluate investment portfolios, or navigate the complexities of business lending.

Understanding the Fundamentals: What Is a Basis Point?

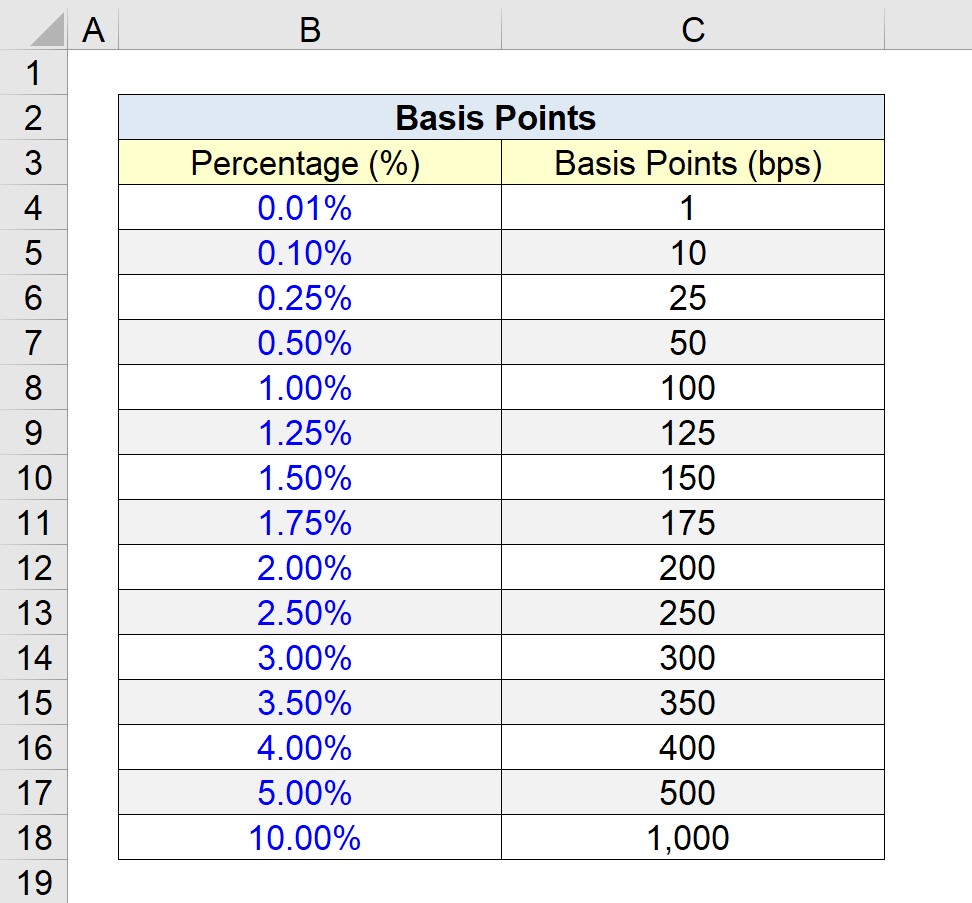

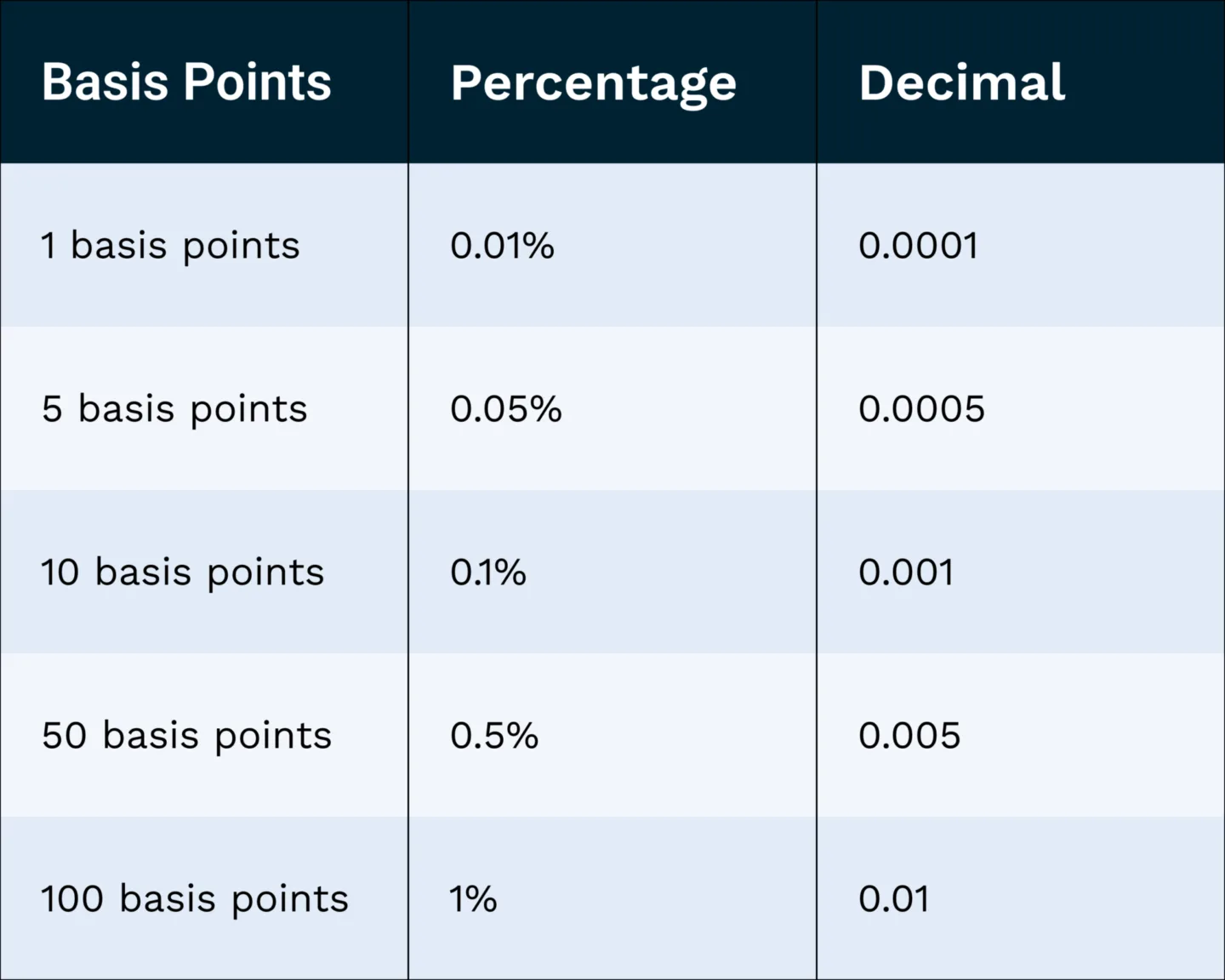

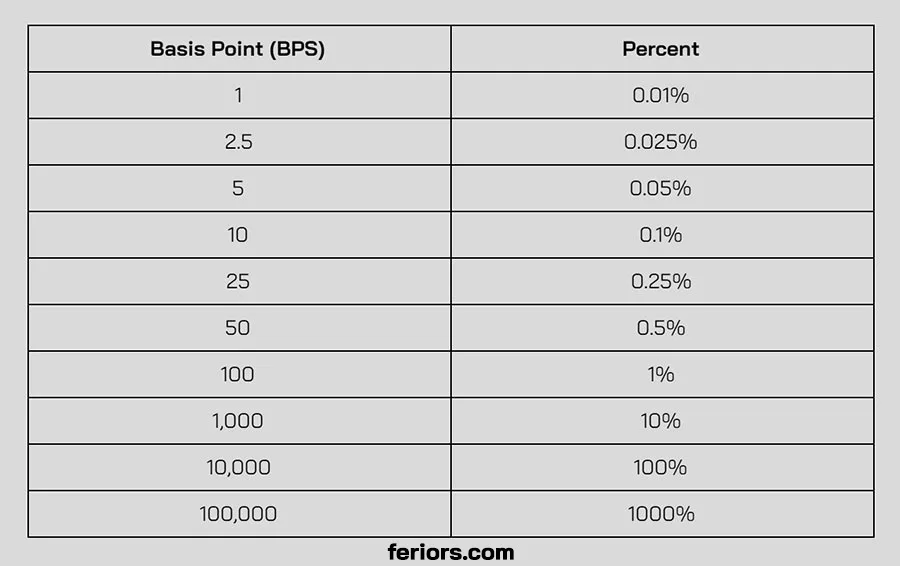

At its simplest level, a basis point is a unit of measure equal to 1/100th of 1%. In decimal form, one basis point is represented as 0.01%, or 0.0001.

The Mathematical Conversion

To visualize how basis points translate to percentages, consider the following scale:

- 1 basis point = 0.01%

- 10 basis points = 0.1%

- 50 basis points = 0.5%

- 100 basis points = 1.0%

- 1,000 basis points = 10.0%

The primary reason finance professionals use this metric is to avoid the inherent ambiguity of “percentage” talk. For example, if an interest rate of 5% “increases by 1%,” does that mean the new rate is 6% (an additive increase) or 5.05% (a relative increase of 1% of the original 5%)? By stating the rate increased by “100 basis points,” there is no room for error: the new rate is definitively 6%.

The Etymology of “Basis”

The term “basis” stems from the “base” or the spread between two interest rates. In the bond market, the “basis” refers to the difference between the price of a cash commodity and its future price. Over time, as financial markets became more sophisticated, the “basis point” became the standardized smallest increment for measuring these changes, ensuring that traders in New York, London, and Tokyo were all speaking the same mathematical language.

The Role of Basis Points in Banking and Monetary Policy

Basis points are perhaps most visible in the headlines following a meeting of a central bank, such as the Federal Reserve in the United States or the European Central Bank. These institutions use basis points to signal subtle yet powerful shifts in economic policy.

Federal Reserve Policy and Interest Rate Hikes

When the economy is overheating and inflation is rising, the Federal Reserve may decide to raise the federal funds rate. They rarely move in full percentage points. Instead, they typically move in increments of 25, 50, or 75 basis points.

A 25-basis-point hike is often viewed as a “standard” or “dovish” adjustment, signaling a cautious approach to cooling the economy. Conversely, a 75-basis-point hike is considered aggressive or “hawkish,” usually reserved for periods of high inflation where the central bank needs to dampen consumer spending and borrowing quickly. Because consumer loans—like auto loans and credit cards—are often tied to these benchmark rates, a shift of just 50 basis points can result in hundreds of dollars of additional interest expenses for the average household annually.

Impact on Mortgages and Long-Term Lending

In the mortgage industry, basis points are the difference between an affordable monthly payment and a financial burden. Lenders use basis points to “price” loans based on the borrower’s creditworthiness.

For instance, a borrower with a 750 credit score might be offered a mortgage at a specific rate, while a borrower with a 650 score might be offered the same loan but with an “add-on” of 50 basis points. On a $400,000 mortgage, a 50-basis-point difference (0.5%) can result in approximately $2,000 of extra interest per year. Over the life of a 30-year loan, that “tiny” measurement of basis points results in $60,000 of additional cost.

Basis Points in Investment Management and Bond Markets

For the serious investor, basis points are most frequently encountered when discussing yields and expense ratios. In the world of high-stakes investing, these small numbers determine the winners and losers of the market.

Bond Yield Spreads and Performance

In fixed-income investing, the “spread” is the difference in yield between two different debt instruments. Investors often compare corporate bonds to “risk-free” government Treasuries. If a corporate bond yields 5% and a 10-year Treasury yields 3%, the spread is 200 basis points.

Monitoring this spread is vital for assessing economic health. When the spread “widens” (increases in basis points), it suggests that investors perceive higher risk in the corporate sector. When it “narrows,” it suggests increasing confidence in the economy. Traders use these fluctuations to make split-second decisions on buying or selling debt.

The Hidden Cost: Expense Ratios

One of the most critical applications of basis points for the average person is in the context of Mutual Funds and Exchange-Traded Funds (ETFs). Every fund charges an “expense ratio” to cover management costs.

It is common to see an actively managed fund charge an expense ratio of 0.75% (75 bps), while a passive index fund might charge 0.05% (5 bps). At first glance, 70 basis points might seem negligible. However, for a retirement account with a balance of $500,000, that 70-basis-point difference represents $3,500 in lost gains every single year. Compounded over 20 or 30 years, those basis points can eat away nearly a third of a portfolio’s potential value.

Practical Applications for Personal Finance and Business

Beyond the ivory towers of Wall Street, basis points have practical applications that affect the “Money” niche on a daily basis, from side hustles to corporate balance sheets.

Comparing Credit Card APRs and Savings Accounts

When shopping for a High-Yield Savings Account (HYSA), consumers often see rates like 4.25% versus 4.50%. While it is easy to say “the second one is better,” thinking in basis points helps quantify the advantage. The second account offers a “25-basis-point premium.”

For a business owner managing cash flow, knowing the basis point difference between various lines of credit is essential for maintaining liquidity. If a business can refinance its debt from an 8.5% interest rate to an 8.1% rate, they have saved 40 basis points. For a company with $1 million in debt, those 40 basis points translate to $4,000 in annual profit that stays in the business rather than going to the bank.

Basis Points in Merchant Processing Fees

For those involved in e-commerce or retail side hustles, merchant processing fees are a constant concern. Credit card processors often charge a percentage of the transaction plus a flat fee (e.g., 2.9% + $0.30). However, many “interchange-plus” pricing models for businesses are quoted in basis points above the wholesale cost.

A processor might offer a rate of “Interchange + 20 basis points.” Understanding this allows a business owner to compare providers effectively. If a competitor offers “Interchange + 15 basis points,” the owner knows they are saving 5 basis points per transaction. In a high-volume business, this understanding of basis points directly correlates to the company’s bottom line and scalability.

Conclusion: Why Precision Matters in Your Financial Journey

The concept of basis points serves as a reminder that in the world of money, the details are where the real wealth is built or lost. Whether it is the Federal Reserve adjusting the sails of the global economy or an individual investor choosing a low-cost index fund, basis points provide the necessary precision to make informed decisions.

By shifting your perspective from broad percentages to the granular accuracy of basis points, you gain a more sophisticated understanding of your financial environment. You begin to see that a 10-basis-point reduction in your mortgage rate, a 20-basis-point increase in your savings yield, and a 50-basis-point drop in investment fees are not just “small numbers.” They are the building blocks of long-term financial security and business success. In the language of finance, every point counts.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.