In the world of corporate finance and investing, profitability is often the headline act. However, savvy investors and business owners know that looking at a company’s bottom line is only half the story. To truly understand the health and operational excellence of an organization, one must look at how effectively the company utilizes its resources to generate revenue. This is where the asset turnover ratio comes into play.

The asset turnover ratio is an efficiency metric that reveals how well a company uses its assets to produce sales. It is a fundamental tool for fundamental analysis, offering a window into management’s ability to squeeze the maximum value out of every dollar invested in property, equipment, inventory, and intellectual property. In this guide, we will explore the nuances of this ratio, how to calculate it, and why it is a critical pillar of business finance.

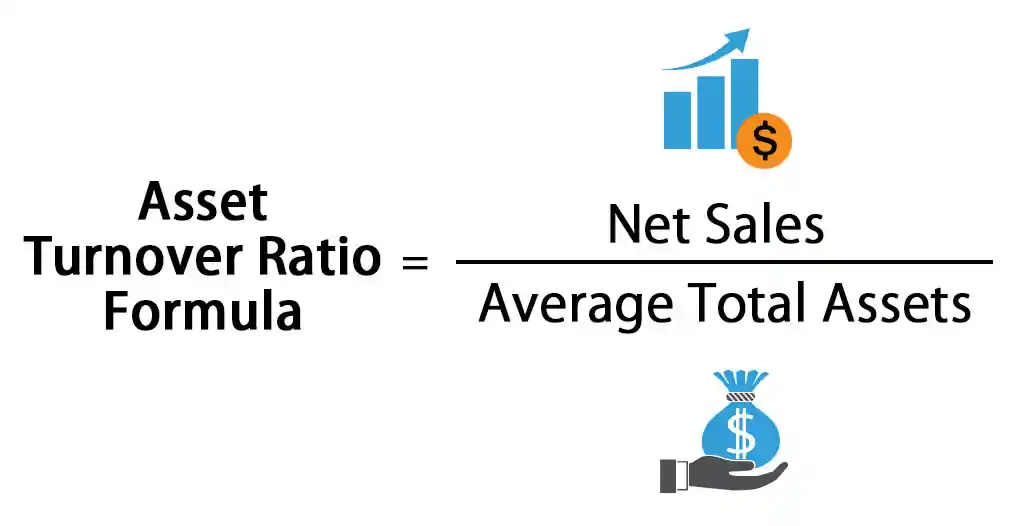

Understanding the Asset Turnover Ratio: Formula and Calculation

At its core, the asset turnover ratio measures the value of a company’s sales or revenues relative to the value of its assets. It is a “turnover” metric, meaning it tells you how many times a company “turns over” its assets in the form of sales during a given period—usually a fiscal year.

The Components: Net Sales and Average Total Assets

To calculate the ratio, you need two primary figures from a company’s financial statements: Net Sales (from the Income Statement) and Total Assets (from the Balance Sheet).

- Net Sales: This represents the total revenue generated by the company minus any returns, allowances, or discounts. It is the “top line” figure that reflects actual realized income from business operations.

- Average Total Assets: Because the Income Statement covers a period of time and the Balance Sheet is a snapshot of a single moment, we use the average of the total assets to ensure accuracy. To find this, you add the total assets at the beginning of the year to the total assets at the end of the year and divide by two.

The Step-by-Step Calculation

The formula is expressed as follows:

Asset Turnover Ratio = Net Sales / Average Total Assets

For example, if a retail company has net sales of $1,000,000 and began the year with $400,000 in assets and ended with $600,000, the average total assets would be $500,000. Dividing $1,000,000 by $500,000 yields an asset turnover ratio of 2.0. This means that for every dollar the company has invested in assets, it generated two dollars in revenue.

Interpreting the Ratio: What the Numbers Tell You

The resulting figure from the calculation is a decimal or a whole number that serves as a benchmark for efficiency. However, a “good” ratio is highly dependent on the industry in which the company operates.

High vs. Low Asset Turnover Ratios

A high asset turnover ratio generally implies that the company is highly efficient at using its assets to generate revenue. Companies with high ratios typically operate in industries with low profit margins but high volume. Retailers like Walmart or Costco, for instance, have very high asset turnover ratios because they move inventory quickly and utilize their physical space aggressively to drive sales.

Conversely, a low asset turnover ratio suggests that a company is not using its assets efficiently or that it operates in a capital-intensive industry. If a company’s ratio is declining over several years, it may indicate that the business is over-invested in unproductive assets, such as outdated machinery or excess inventory that isn’t selling.

Industry Benchmarks and Context

It is vital to compare companies within the same sector. For example, a technology software company (which has few physical assets) will naturally have a much higher turnover ratio than a utility company or a telecommunications giant that must invest billions in power plants or fiber-optic cables.

In capital-intensive industries, a lower asset turnover ratio is expected because the assets (like a Boeing manufacturing plant) take a long time to build and even longer to pay off through sales. Therefore, when evaluating a stock or a business’s performance, always use peer-group averages as your yardstick.

Why Asset Turnover Matters for Investors and Business Owners

The asset turnover ratio is more than just a math exercise; it is a vital indicator of management performance and financial sustainability.

Measuring Operational Efficiency

For a business owner, the asset turnover ratio is a report card on operations. It answers the question: “Are we buying too much equipment for the amount of sales we are making?” High efficiency often leads to better cash flow. If a company can generate the same amount of sales with fewer assets, it frees up capital that can be reinvested in growth, used to pay down debt, or returned to shareholders as dividends.

Identifying Potential Red Flags

For investors, the asset turnover ratio is an early warning system. If a company reports increasing profits but a declining asset turnover ratio, it could be a sign that the “quality” of those profits is low. It may mean the company is achieving growth only by throwing massive amounts of capital at the problem, rather than by improving its core business processes.

Furthermore, the asset turnover ratio is a key component of the DuPont Analysis, a framework that breaks down Return on Equity (ROE). The DuPont model shows that ROE is driven by three things: profit margin, financial leverage, and—crucially—asset turnover. This highlights that a company can be highly profitable not just by having high margins, but by being exceptionally efficient with its assets.

Strategies to Improve the Asset Turnover Ratio

If a business identifies that its asset turnover ratio is lagging behind its competitors, there are several strategic levers management can pull to improve the metric.

Optimizing Inventory Management

Inventory is often the largest component of current assets for manufacturing and retail firms. If inventory sits in a warehouse for months, it is a “lazy” asset. By implementing Just-In-Time (JIT) inventory systems or using data analytics to better predict consumer demand, a company can reduce the amount of inventory it holds while maintaining the same level of sales. This lowers the denominator (Average Total Assets) and boosts the ratio.

Accelerating Accounts Receivable

Accounts receivable—money owed to the company by customers—is also an asset. While it counts as value on the balance sheet, it isn’t “working” for the company until the cash is collected. By tightening credit policies, offering small discounts for early payment, or being more aggressive with collections, a company can convert these receivables into cash faster. This reduces the total asset base and improves the turnover efficiency.

Strategic Asset Divestment

Sometimes, a low ratio is the result of “bloat.” Companies may hold onto real estate, old machinery, or underperforming business units that no longer contribute significantly to the top line. Selling off these unproductive assets—often called “slimming down”—can dramatically improve the asset turnover ratio. This lean approach ensures that every asset remaining on the balance sheet is a high-performer contributing to revenue.

Limitations of the Asset Turnover Ratio

While powerful, the asset turnover ratio should not be viewed in a vacuum. There are specific nuances that can skew the data if not properly understood.

The Impact of Asset Age and Depreciation

Because the ratio uses the “book value” of assets (the purchase price minus accumulated depreciation), older assets can make a company look more efficient than it actually is. A company with very old, fully depreciated machinery will have a very small denominator, resulting in an artificially high asset turnover ratio. A competitor who just invested in a brand-new, state-of-the-art factory will have a much lower ratio initially, even though their long-term competitive advantage might be much stronger.

Seasonal Fluctuations and Timing

The timing of asset purchases can also distort the ratio. If a company buys a massive amount of equipment right at the end of the fiscal year, its “Average Total Assets” will spike, but those assets haven’t had time to contribute to “Net Sales” yet. This results in a temporary dip in the ratio that doesn’t necessarily reflect poor management. This is why it is essential to look at the trend of the ratio over three to five years rather than focusing on a single point in time.

Conclusion

The asset turnover ratio is a cornerstone of financial analysis, offering deep insights into how a company converts its investments into revenue. For the investor, it is a tool to distinguish between companies that are truly efficient and those that are simply asset-heavy. For the business owner, it serves as a vital diagnostic tool to ensure that capital is being deployed effectively.

By understanding the relationship between sales and assets, and by considering the specific context of the industry and asset life cycles, you can gain a much clearer picture of a company’s financial health. In the quest for financial success, remember that it isn’t just about how much you make; it’s about how hard your assets are working to make it.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.