In the landscape of personal finance, your relationship with a banking institution is one of the most fundamental pillars of your economic life. However, as financial goals evolve, many individuals find that their current bank no longer serves their needs. Whether you are moving toward a high-yield online bank, consolidating your accounts for better visibility, or simply looking to avoid monthly maintenance fees, knowing how to close a Chase checking account properly is essential.

Closing a bank account is more than just withdrawing your cash and walking away. It is a strategic process that requires attention to detail to ensure your financial health remains intact. In this guide, we will explore the nuances of closing a Chase account, the preparation required to avoid common pitfalls, and the broader implications of account management within your personal finance ecosystem.

Preparation: Essential Steps Before Closing Your Account

Before you initiate the closure of your Chase checking account, you must conduct a thorough audit of your financial activity. Jumping into a closure without a plan can lead to failed payments, overdraft fees, and unnecessary stress.

Auditing Your Automatic Transactions

The modern financial life is built on automation. From monthly subscriptions like Netflix and Spotify to essential bills like your mortgage or car insurance, your checking account likely serves as a hub for numerous recurring payments. Before closing the account, download at least six months of bank statements. Look for every recurring “ACH” (Automated Clearing House) transfer. You will need to manually move each of these to your new financial institution. Failing to do so could result in missed payments, which might negatively impact your credit score or lead to service interruptions.

Redirecting Your Direct Deposits

Perhaps the most critical step in the preparation phase is notifying your employer’s payroll department. Direct deposits can take one to two pay cycles to update. If a paycheck is sent to a closed Chase account, it will typically be bounced back to the employer, causing a significant delay in you receiving your funds. Ensure your new account is fully active and that your employer has confirmed the change before you pull the trigger on the Chase closure.

Establishing Your “Landing Pad” Account

Never close a bank account before your new one is fully operational. You need a “landing pad” for your capital. Open your new account, order your new debit cards, and ensure the mobile app is functional. This overlap period, where both accounts are open simultaneously, is the safest way to transition without a gap in your liquid cash access.

Choosing Your Method: The Best Ways to Close a Chase Account

Chase is one of the largest financial institutions in the world, and they provide several avenues for account closure. Depending on your preference for digital convenience or face-to-face interaction, you can choose the method that best fits your schedule.

Closing In-Person at a Branch

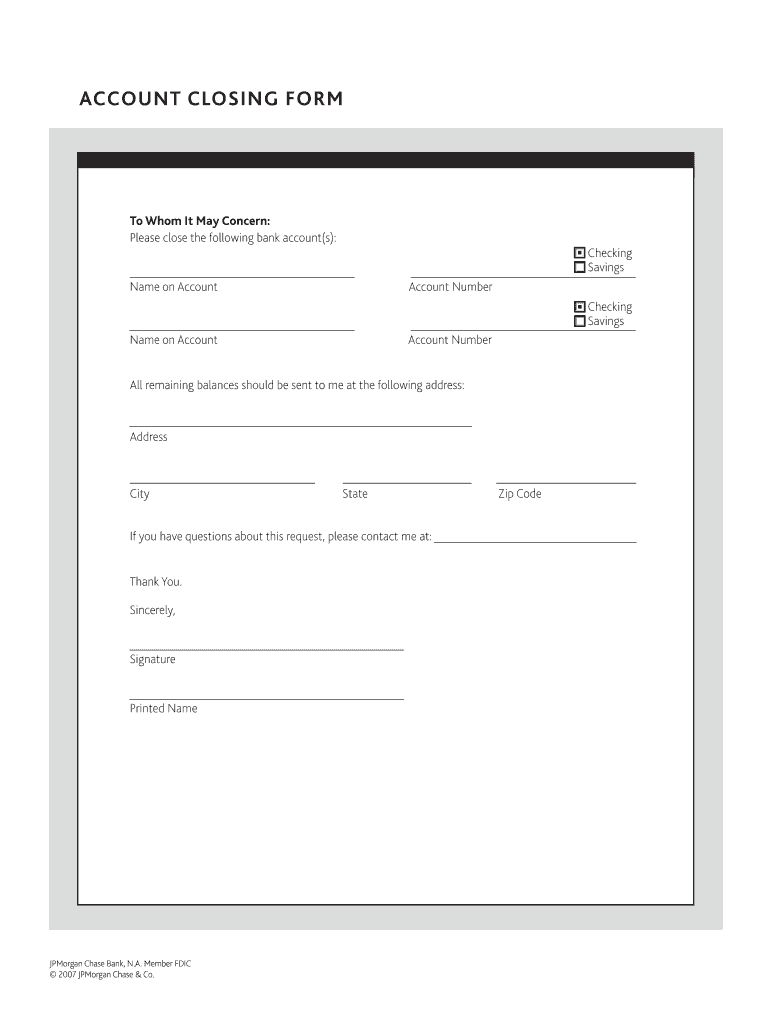

For many, the most secure way to close an account is to visit a local Chase branch. This allows you to speak directly with a personal banker, sign the necessary paperwork, and receive immediate physical documentation that the account is closed. If you have a significant balance remaining, the banker can often cut you a cashier’s check on the spot, providing a clean break from the institution.

Utilizing the Secure Message Center

If you prefer a digital approach and do not want to spend time on the phone, Chase offers a “Secure Message Center” through their online banking portal. You can send a formal request to close your account. However, keep in mind that Chase may require your account balance to be exactly zero before they can process this request. This method is efficient but may take a few business days for a representative to respond and finalize the action.

Closing via Telephone

You can call Chase’s customer service line to request a closure. This is a middle-ground option that provides human interaction without the need to travel to a branch. During the call, the representative will likely attempt to “retain” you as a customer by offering to waive fees or suggesting different account types. If your mind is made up, remain firm but professional. Ensure you ask for a reference number for the call and a written confirmation of the closure to be sent via mail or email.

Avoiding Fees and Pitfalls During the Process

The transition between banks is a high-risk period for “hidden” costs. Banks operate on strict sets of rules, and Chase is no exception. Understanding these rules will save you money and protect your financial reputation.

The 90-Day Early Closure Rule

Like many major banks, Chase may charge an “early account closure fee” if you close your checking account within 90 days of opening it. Typically, this fee is around $25. This is designed to prevent “churning”—the practice of opening accounts just to collect sign-up bonuses and then immediately closing them. If you recently opened the account, it is often financially prudent to wait until the 91st day to close it.

The Danger of the “Zombie Account”

A “zombie account” occurs when a closed account is inadvertently reopened. This usually happens because a stray automatic payment (like a gym membership) hits the account after you thought it was closed. Chase might honor the payment, resulting in a negative balance and subsequent overdraft fees. Because you are no longer monitoring the account, these fees can compound. To avoid this, ensure you receive a formal “Account Closed” letter and monitor your mail for any unexpected statements.

Maintaining the Minimum Balance

If your Chase account requires a minimum daily balance to waive the monthly service fee (commonly $12 for a Total Checking account), you must be careful when withdrawing your funds. If you move your money to your new bank but leave the Chase account open for a week while the closure processes, the balance may dip below the minimum. This could trigger a final monthly fee right before the account closes. To mitigate this, consider keeping the minimum required balance in the account until the very day you speak with a banker to finalize the closure.

Post-Closure Best Practices: Securing Your Financial Future

Once the account is officially closed, your job isn’t quite finished. There are a few administrative tasks that will ensure this move contributes positively to your overall financial strategy.

Document Retention

In the world of personal finance, documentation is your best defense. Keep your final Chase statement and the closure confirmation letter for at least seven years. This is important for tax purposes, as well as for resolving any future disputes regarding unpaid bills or identity theft. If a creditor claims you didn’t pay a bill three years from now, having your final bank records can prove exactly where your money was at that time.

Updating Your Financial Tools

If you use budgeting software or aggregators like Mint, YNAB, or Empower, you will need to disconnect your Chase account and link your new one. This ensures your net worth calculations and spending trends remain accurate. This is also a great time to reassess your overall financial goals. Does your new bank offer better interest rates? Does it provide the “buckets” or “folders” you need to organize your savings? Use this transition as a catalyst for broader financial improvement.

Monitoring Your Credit Report

While closing a checking account does not directly affect your FICO score (unlike closing a credit card), it can have indirect effects. If an account is closed with a negative balance due to unpaid fees, Chase may report this to ChexSystems—a consumer reporting agency that tracks banking history. A negative mark on ChexSystems can make it very difficult to open a bank account at any other institution for several years. Always ensure your balance is zero or positive at the time of closure.

Why Closing a Bank Account Matters for Your Financial Health

In a professional financial strategy, every tool you use should serve a purpose. Keeping an unused or “expensive” checking account open is a form of financial clutter. By closing a Chase account that no longer fits your needs, you are practicing “financial hygiene.”

This process forces you to look closely at your cash flow, identify forgotten subscriptions, and take an active role in where your money lives. It is a move from passive banking to active wealth management. Choosing a financial partner that aligns with your values—whether that means lower fees, better technology, or higher interest rates—is a vital step in the journey toward financial independence.

By following the structured approach outlined above, you turn a potentially tedious administrative task into a streamlined, professional transition. You protect your capital, avoid unnecessary fees, and set the stage for a more efficient and productive relationship with your money.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.