For most individuals, a home is the most significant financial asset they will ever own. In the realm of personal finance and wealth management, understanding the legal instruments that govern this asset is paramount. While many homeowners use the terms “title” and “deed” interchangeably, they represent two distinct concepts in the world of finance and property law. A deed is the physical, legal document that transfers ownership of real estate from a seller to a buyer, serving as the ultimate proof of an investment’s security.

Understanding what a deed is, how it functions, and the various types available is essential for any savvy investor or homeowner looking to protect their equity and ensure a smooth transfer of wealth.

Understanding the Deed as a Primary Financial Instrument

At its core, a deed is a written legal instrument that conveys the ownership of real property from the grantor (the seller or transferor) to the grantee (the buyer or recipient). In the context of personal finance, the deed is the vehicle through which your largest investment is secured. Without a properly executed and recorded deed, your financial claim to a property is tenuous at best.

The Critical Distinction Between Title and Deed

To master real estate finance, one must distinguish between “title” and a “deed.” Title is a conceptual term representing the bundle of rights associated with property ownership—the right to use the land, the right to sell it, and the right to exclude others. A deed, conversely, is the physical document that proves you hold that title.

Think of it in terms of a vehicle: the “title” is your legal right to own the car, while the “deed” is analogous to the physical registration papers you must produce to prove that right. In financial planning, ensuring that the deed is correctly drafted and recorded is what prevents “clouds” on a title, which can diminish the property’s value or prevent a future sale.

The Legal Requirements for a Valid Deed

From a business and financial perspective, a deed must meet specific criteria to be considered legally binding. If these elements are missing, the financial transfer can be voided, leading to catastrophic loss of capital. A valid deed must:

- Be in writing.

- Clearly identify the grantor and grantee.

- Contain a legal description of the property (not just a street address, but precise metes and bounds).

- State the “consideration” (the financial value or purchase price exchanged).

- Be signed by a grantor who is of sound mind and legal age.

- Be delivered to and accepted by the grantee.

Types of Deeds and Their Implications for Financial Risk

Not all deeds are created equal. The type of deed used in a transaction dictates the level of financial protection the buyer receives. For investors and homeowners, choosing the wrong deed type can expose them to undisclosed liens, third-party claims, or legal disputes that can drain a bank account.

General Warranty Deeds: The Gold Standard for Buyers

In a standard residential purchase, the General Warranty Deed is the preferred instrument. This deed offers the highest level of financial protection. The grantor “warrants” that they own the property free and clear and that they will defend the title against any and all claims, even those arising from before they owned the property. For a buyer, this is a form of financial insurance provided by the seller, guaranteeing that the investment is sound and unencumbered.

Special Warranty Deeds and Commercial Finance

Commonly used in commercial real estate and foreclosure sales, a Special Warranty Deed offers more limited protection. The grantor only warrants that they haven’t done anything to encumber the title during their period of ownership. They do not provide guarantees for anything that happened prior to their acquisition. From a financial analysis perspective, a Special Warranty Deed requires a much more rigorous title search and more robust title insurance to mitigate the increased risk of historical claims.

Quitclaim Deeds: High Risk and Specific Utility

A Quitclaim Deed offers the least amount of protection. It transfers whatever interest the grantor has in the property “as is,” without any warranties. If the grantor actually owns nothing, the grantee receives nothing. These are rarely used in traditional sales but are common in personal finance strategies such as transferring property into a living trust, moving assets between family members, or resolving a divorce settlement. Using a Quitclaim Deed in a high-value investment transaction is generally considered a significant financial risk.

The Role of Deeds in Real Estate Investing and Equity Protection

For those viewing real estate as a component of a diversified investment portfolio, the deed is more than just paperwork; it is the foundation of equity. Maintaining a “clear” deed is essential for leveraging the property for future wealth-building activities, such as securing a Home Equity Line of Credit (HELOC) or refinancing at lower interest rates.

Protecting Your Equity from Liens and Encumbrances

A deed represents your financial stake in a property, but that stake can be eroded by encumbrances. When a homeowner fails to pay taxes, contractors, or child support, a lien can be placed against the property’s title. These liens are legally attached to the deed. If you attempt to sell the property, these financial obligations must be satisfied out of the proceeds before you receive a dime of your equity. Understanding the status of your deed allows you to proactively manage these liabilities and protect your net worth.

The Necessity of Title Insurance in Financial Planning

Because deeds can sometimes be fraudulent or contain errors (such as a missing signature from a previous spouse), the financial industry utilizes title insurance. When you purchase a property, a one-time premium protects you against financial loss resulting from defects in the deed. This is a crucial risk management tool; it ensures that if a long-lost heir emerges with a claim to your land, the insurance company covers the legal costs and the potential loss of value, rather than you having to liquidate other assets to cover the cost.

Transferring Deeds: Strategic Wealth Management and Tax Considerations

The manner in which a deed is held and transferred has profound implications for estate planning, tax liability, and the preservation of generational wealth. Strategic decisions made today regarding the deed can save your heirs thousands of dollars in legal fees and taxes.

Probate vs. Living Trusts: Streamlining Asset Transfer

In many jurisdictions, if a deed is held in the name of an individual, the property must go through the probate process upon their death. Probate is often expensive, time-consuming, and can erode the total value of the estate. By using a “Transfer on Death Deed” or deeding the property into a Revocable Living Trust, investors can ensure the property bypasses probate. This allows for an immediate transfer of the financial asset to beneficiaries, maintaining liquidity within the family.

Joint Tenancy and Rights of Survivorship

For couples and business partners, how the names appear on the deed is a vital financial decision. “Joint Tenancy with Right of Survivorship” ensures that if one owner dies, their share automatically transfers to the survivor. Conversely, “Tenancy in Common” allows owners to bequeath their portion to whoever they choose. Choosing the correct vesting on a deed is a foundational step in business partnership agreements and marital financial planning.

Tax Implications: Capital Gains and Gift Taxes

Transferring a deed isn’t just a legal move; it’s a taxable event. If you “gift” a house to a child via a Quitclaim Deed, you may trigger gift tax implications or forfeit the “stepped-up basis” that occurs when an asset is inherited after death. A stepped-up basis can save beneficiaries tens of thousands of dollars in capital gains taxes. Consulting with a financial advisor before altering a deed is essential to ensure that a well-intentioned transfer doesn’t result in an unnecessary tax burden.

The Modern Landscape of Property Documentation

As we move further into a digital-first economy, the way deeds are recorded and managed is evolving. However, the fundamental financial principles remain the same: the deed is the ultimate arbiter of ownership and value.

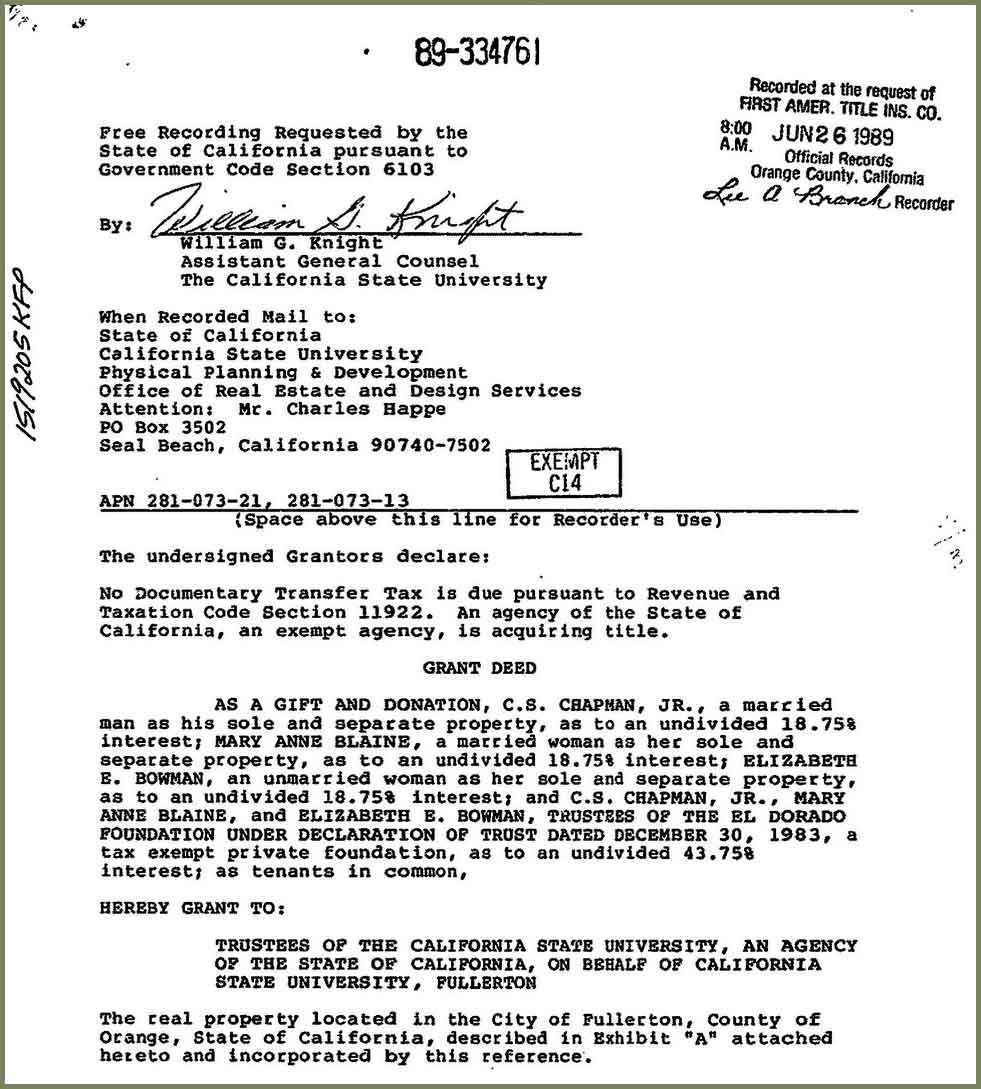

Public Records and the Recording Process

Once a deed is signed and notarized, it must be recorded with the local county recorder or registrar of deeds. This “public notice” is what protects your financial interest against subsequent claims. In the eyes of the law and the financial system, an unrecorded deed may as well not exist. Recording the deed creates a chain of title that allows lenders to verify your ownership, which is a prerequisite for any form of asset-backed lending.

Conclusion: Deed Literacy as a Pillar of Financial Success

In conclusion, a deed on a house is far more than a simple document; it is the bedrock of real estate ownership and a critical component of personal finance. By understanding the nuances between different types of deeds, the importance of title insurance, and the strategic implications of deed transfers, you can protect your most valuable asset from legal and financial volatility. Whether you are a first-time homebuyer or a seasoned real estate investor, mastering the complexities of the deed is an essential step in securing your financial future and building lasting wealth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.