In the complex landscape of personal finance, the credentials behind a professional’s name serve as a roadmap for their expertise and ethical commitments. Among the most prestigious and rigorous of these designations is the Chartered Financial Consultant (ChFC). While many investors are familiar with the “Certified Financial Planner” (CFP) mark, the ChFC represents a deep, specialized dive into the mechanics of financial planning, insurance, and wealth management.

Established in 1982 by The American College of Financial Services, the ChFC was designed to provide financial professionals with a comprehensive education that goes beyond generalities. Today, it stands as a hallmark of excellence for those who wish to master the intricacies of the tax code, estate planning, and risk management. This article explores the depth of the ChFC designation, its curriculum, and how it compares to other industry standards.

The Anatomy of the ChFC Designation

The ChFC is not a certification one can obtain through a weekend seminar or a simple multiple-choice test. It is a professional credential that requires a significant investment of time, intellect, and practical experience. It is specifically tailored for those who want to provide holistic financial advice, moving beyond simple product sales into the realm of true financial strategy.

Educational Rigor and Requirements

To earn the ChFC, a candidate must complete a minimum of eight college-level courses. These are not mere introductions; they are deep dives into the technical aspects of financial planning. Each course concludes with a proctored examination. On average, professionals spend over 400 hours of study to master the material.

The curriculum is designed to be cumulative. It begins with the fundamentals of financial planning—understanding the economic environment and the time value of money—and scales up to complex applications of tax law and asset protection. Because the courses are administered by an accredited non-profit educational institution (The American College of Financial Services), the academic standards are consistently high.

Professional Experience and Ethics

Education alone does not make a ChFC. The American College requires candidates to demonstrate a significant track record of professional experience. Specifically, applicants must have three years of full-time, relevant business experience within the five years preceding the awarding of the designation. This ensures that the consultant has not only the theoretical knowledge but also the practical “in-the-trenches” experience of working with clients.

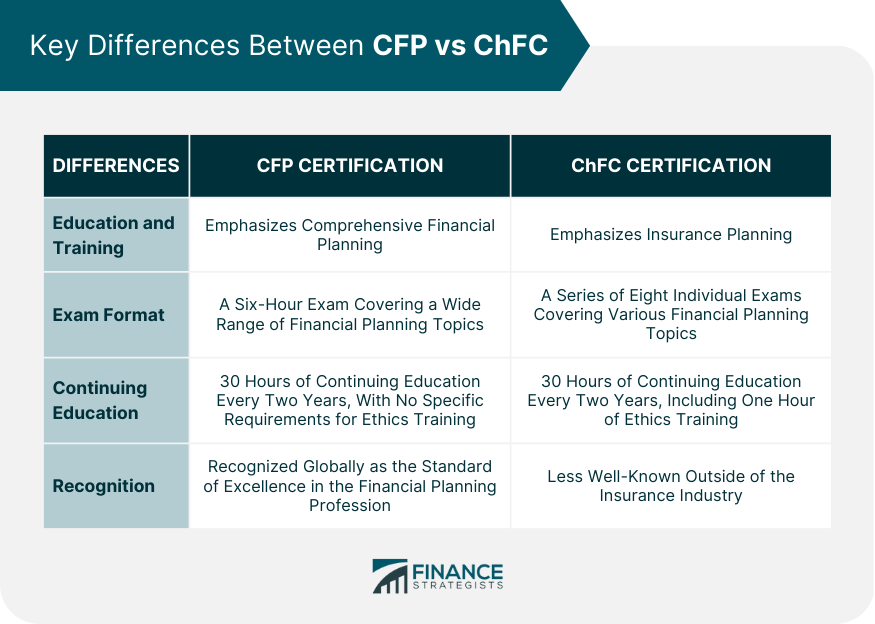

Furthermore, every ChFC must adhere to a strict Code of Ethics. This includes a commitment to the fiduciary standard—acting in the client’s best interest at all times. Professionals must also meet continuing education (CE) requirements, typically completing 30 hours of credit every two years to maintain their status and stay current with changing laws and financial trends.

Comprehensive Curriculum: What a ChFC Learns

The true value of a Chartered Financial Consultant lies in the breadth and depth of their knowledge. While some designations focus heavily on investment selection, the ChFC curriculum is built on the philosophy that all areas of a person’s financial life are interconnected.

Financial Planning Fundamentals and Risk Management

The journey begins with an exhaustive look at risk management and insurance. A ChFC is trained to identify potential “financial leaks”—areas where an individual or business is exposed to catastrophic loss. This includes analyzing life insurance, disability income insurance, and long-term care needs. Unlike a salesperson, a ChFC looks at insurance as a tool for wealth preservation rather than just a product.

Following risk management, the curriculum focuses on income tax planning. In the world of money, it’s not just about what you earn; it’s about what you keep. ChFCs study the nuances of the tax code to help clients minimize their tax liabilities through strategic investments, charitable giving, and retirement account selection.

Advanced Estate and Tax Planning

One of the distinguishing features of the ChFC is its emphasis on estate planning. Many financial professionals have a surface-level understanding of wills and trusts, but the ChFC curriculum dives into the technicalities of the federal estate tax, gift taxes, and the instruments used to transfer wealth across generations efficiently.

This includes learning how to structure Irrevocable Life Insurance Trusts (ILITs), Family Limited Partnerships, and various charitable trusts. For high-net-worth individuals, this expertise is invaluable, as it ensures that their legacy is preserved and that heirs are not burdened with unnecessary tax hurdles or legal complications.

Specialized Planning for Modern Needs

Perhaps the most unique aspect of the ChFC designation is its focus on specialized planning niches. The curriculum often includes electives or specific modules on:

- Retirement Planning: Calculating sustainable withdrawal rates and managing Social Security integration.

- Small Business Planning: Addressing succession planning, buy-sell agreements, and executive compensation.

- Divorce and Special Needs Planning: Managing the unique financial traumas and long-term requirements of specialized family situations.

- Behavioral Finance: Understanding the psychology behind why clients make poor financial decisions and learning how to coach them toward better habits.

ChFC vs. CFP: Choosing the Right Path

The question most often asked by both aspiring professionals and savvy clients is: “What is the difference between a ChFC and a CFP?” Both are highly respected and share a significant amount of overlapping content, but their structures and focus areas differ.

Structural Differences in Examination

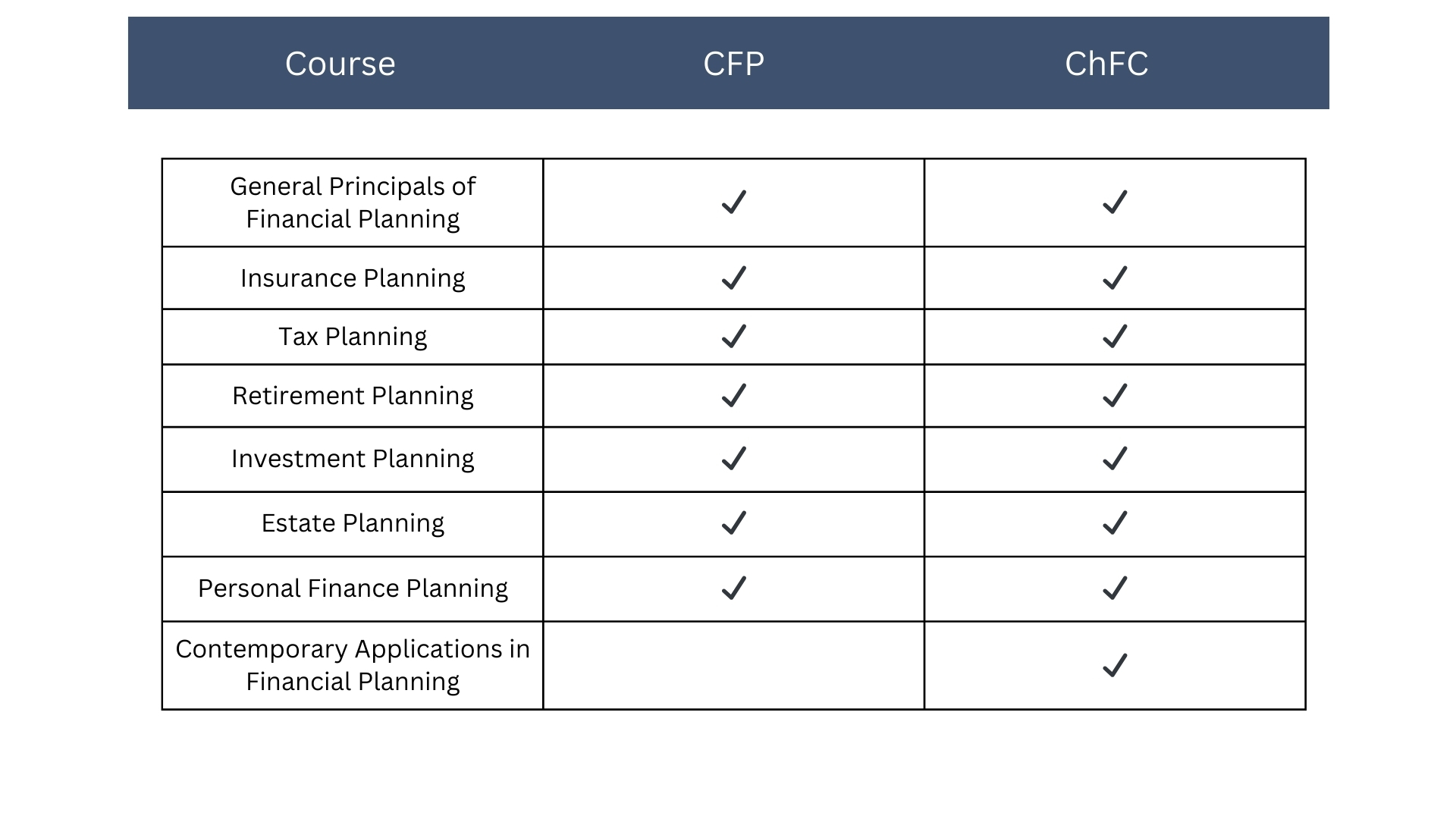

The Certified Financial Planner (CFP) designation is famous for its “Board Exam”—a grueling, comprehensive ten-hour test that covers all topics at once. It is a generalist’s marathon. In contrast, the ChFC takes a modular approach. While the total number of study hours is often higher for the ChFC (eight courses versus the CFP’s six-course equivalent), the ChFC tests students at the end of each specific subject.

This modularity allows for more depth in specific areas. Because the ChFC requires two additional courses beyond what is typically required for the CFP, many professionals argue that the ChFC provides a more specialized level of knowledge in areas like insurance and employee benefits.

Focus Areas and Philosophical Nuance

The CFP is widely recognized as the “gold standard” for general financial planning and is highly marketed to the public. However, the ChFC is often favored by those coming from the insurance or institutional planning side of the industry.

The ChFC curriculum is slightly more technical regarding applications for business owners and high-net-worth estate planning. Because of the overlap, it is very common to see professionals carry both sets of initials. In these cases, the CFP provides the foundational broad-based planning framework, while the ChFC provides the specialized technical “finishing” in niche areas of the tax code and risk management.

Which One Should You Hire?

For a consumer, the choice between a ChFC and a CFP is less about which is “better” and more about the specific needs of the client. If you are looking for a general retirement plan and investment oversight, both are excellently qualified. However, if your situation involves complex business ownership, intricate estate tax issues, or a need for deep insurance analysis, a ChFC may have a slight edge in specialized training.

The Value Proposition for Clients and Professionals

In an era of “robo-advisors” and DIY investing apps, the human element of financial consulting remains indispensable. The ChFC designation represents a commitment to that human element, backed by rigorous data and academic discipline.

Why Expertise Matters in a Volatile Economy

Markets are inherently volatile, and tax laws are constantly in flux. A ChFC acts as a stabilizing force. Because their training includes a heavy emphasis on macroeconomics and the history of financial markets, they are less likely to react impulsively to short-term market swings.

For the client, this expertise translates into peace of mind. Knowing that your consultant has mastered the intricacies of “Capital Gains” vs. “Ordinary Income” or understands how to pivot an estate plan after a new piece of legislation is passed (such as the SECURE Act) provides a level of security that an uncredentialed advisor simply cannot offer.

Career Trajectory and Industry Standing

For the financial professional, the ChFC is a career catalyst. It signals to employers and clients alike that the individual has the discipline to complete a multi-year program. In the competitive world of wealth management, having “ChFC” after your name can lead to higher trust scores, better client retention, and the ability to command higher fees due to the specialized nature of the advice provided.

Furthermore, the ChFC community is a robust network of some of the most educated minds in finance. Being part of this cohort allows for peer-to-peer learning and access to the latest research coming out of The American College.

Conclusion: The Gold Standard of Specialized Planning

The Chartered Financial Consultant (ChFC) is more than just a title; it is a testament to a professional’s dedication to the craft of financial planning. By covering the entire spectrum of a client’s financial life—from the basics of budgeting to the complexities of multi-generational wealth transfer—the ChFC ensures that no stone is left unturned.

For the investor, a ChFC offers a holistic partner who looks beyond the portfolio to the person. For the professional, it offers a path to mastery in an industry that demands nothing less. Whether you are seeking to build a legacy or protect your family’s future, understanding the depth of the ChFC designation is the first step toward sophisticated financial health. In the world of money, knowledge is power, and the ChFC is one of the most powerful tools available.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.