In the complex ecosystem of global finance, stability is maintained through a series of checks and balances designed to prevent a single failure from triggering a systemic collapse. Among the most critical, yet often misunderstood, mechanisms in this framework is variation margin. While the term might sound like technical jargon relegated to the back offices of investment banks, it is actually a fundamental concept in the world of derivatives, investing, and corporate finance.

Variation margin serves as the “pay-as-you-go” system for financial contracts. It ensures that as market prices fluctuate, the parties involved in a trade stay current with their obligations. In an era defined by market volatility and rapid-fire digital trading, understanding variation margin is essential for any professional navigating the landscape of business finance and institutional investing.

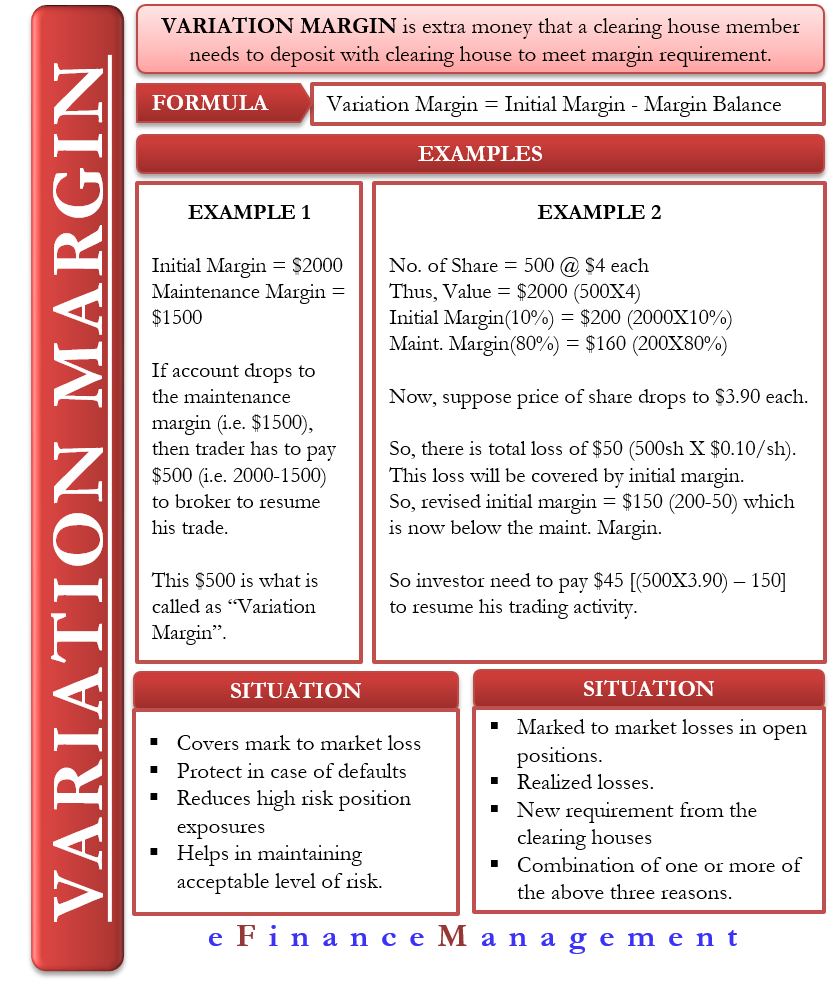

The Fundamentals of Variation Margin

At its core, variation margin is a collateral payment made by one party to another to account for changes in the market value of a financial instrument. This process is most common in the derivatives market, including futures, options, and swaps.

Definition and Core Mechanics

Variation margin is the amount of cash or high-quality collateral that must be transferred between two parties—typically a buyer and a seller or a trader and a clearinghouse—to reflect the daily price movements of a contract. Unlike a one-time fee, variation margin is a continuous requirement. If the value of your position drops, you must pay the variation margin to cover that loss in real-time. Conversely, if the position gains value, you receive a variation margin payment.

The primary objective is simple: to ensure that at the end of every trading day, no party owes a significant, uncollateralized debt to the other. By squaring the books daily, the financial system prevents the buildup of massive, hidden losses that could lead to a default.

The “Mark-to-Market” Process

The engine behind variation margin is a practice known as “marking-to-market.” This is the act of recording the price or value of a security, portfolio, or account to reflect the current market level rather than its book value.

For example, if an investor enters a futures contract to buy oil at $70 a barrel and the price drops to $68 by the end of the day, the investor has an unrealized loss of $2 per barrel. Through the mark-to-market process, the clearinghouse will require the investor to pay a variation margin of $2 per barrel immediately. This payment “marks” the contract to its new market reality.

Variation Margin vs. Initial Margin

To fully grasp variation margin, one must distinguish it from its counterpart: initial margin.

- Initial Margin is the “entry fee” or the collateral required to open a position. It acts as a safety buffer against potential future losses.

- Variation Margin is the “maintenance fee.” It does not sit idle; it moves back and forth daily based on actual price performance.

Think of initial margin as a security deposit on a rental property, while variation margin is the fluctuating utility bill you pay based on your actual usage throughout the month.

How Variation Margin Operates in the Derivatives Market

The mechanics of variation margin are highly standardized to ensure speed and reliability. In the modern financial era, this process is largely managed by central entities to remove the guesswork and bilateral friction between individual traders.

The Role of Central Counterparties (CCPs)

In most regulated markets, variation margin is managed by a Central Counterparty (CCP) or a clearinghouse. The CCP sits in the middle of every trade; it becomes the buyer to every seller and the seller to every buyer. By acting as the central hub, the CCP can calculate exactly how much variation margin is owed across the entire market.

When a trader loses money on a position, they pay the CCP. The CCP then immediately passes that money to the trader who gained on the opposing side of the contract. This centralized oversight significantly reduces the risk that a default by one small firm will snowball into a larger crisis.

The Calculation Cycle: Daily Settlements

One of the defining features of variation margin is its frequency. In most liquid markets, variation margin is calculated and settled at least once a day, often after the market closes. However, during periods of extreme volatility, clearinghouses may issue “intraday margin calls,” requiring payments within hours or even minutes.

This high-frequency settlement ensures that the financial exposure between parties is rarely older than 24 hours. By keeping the “debt” fresh and paid up, the system remains lean and transparent.

Eligible Collateral for Variation Margin

Because variation margin must be settled quickly to keep up with market moves, the type of collateral accepted is strictly regulated. For variation margin, cash is the king of collateral. Unlike initial margin, which might allow for government bonds or high-grade corporate debt, variation margin is almost exclusively paid in cash (specifically in the currency of the underlying contract).

The reason for this is liquidity. If a clearinghouse needs to pay out a winner, it cannot wait for a bond to be sold or a treasury bill to mature. It needs liquid funds to maintain the seamless flow of the “mark-to-market” cycle.

Why Variation Margin is Critical for Financial Stability

The importance of variation margin extends far beyond individual profit and loss. It is a macro-prudential tool that protects the entire global economy from systemic shocks.

Mitigating Counterparty Credit Risk

Counterparty credit risk is the danger that the person or institution on the other side of your trade will go bankrupt before they can fulfill their obligation. Before the widespread adoption of strict variation margin rules, a company could accumulate massive losses on paper without actually having to pay them out until the contract expired. If that company went bust in the interim, their counterparties would be left with nothing.

Variation margin eliminates this “buildup” of risk. Because losses are paid daily, the most a counterparty can lose is typically one day’s worth of market movement.

Preventing Systemic Contagion

History has shown that the failure of one large financial institution can lead to a “domino effect.” During the 2008 financial crisis, the lack of transparency and collateralization in the over-the-counter (OTC) derivatives market was a primary driver of panic.

Today, variation margin acts as a firebreak. If a firm fails today, they have already paid their losses up to yesterday’s closing prices. This prevents their failure from automatically bankrupting their trading partners, thereby containing the damage to a single entity rather than the whole network.

Regulatory Evolution Since 2008

Post-2008 regulations, such as the Dodd-Frank Act in the United States and the European Market Infrastructure Regulation (EMIR) in Europe, have made variation margin mandatory for a much wider range of products. Even “uncleared” swaps—those not traded on an exchange—are now subject to Uncleared Margin Rules (UMR). These global standards have forced transparency onto what was once a “shadow” banking sector, making the financial world significantly more resilient.

Practical Implications for Investors and Institutions

For hedge funds, pension funds, and corporate treasurers, variation margin is not just a regulatory requirement; it is a major operational and liquidity consideration.

Liquidity Management Challenges

The biggest challenge posed by variation margin is the “liquidity drain.” Because variation margin must be paid in cash, firms must keep significant cash buffers on hand. During a market crash, a firm might be fundamentally solvent (owning billions in real estate or stocks), but if they don’t have the immediate cash to meet a variation margin call on their hedges, they can be forced into a “fire sale” or technical default.

Effective liquidity management involves stress-testing portfolios to ensure that even in a “black swan” event, the firm has enough cash to cover a massive spike in variation margin requirements.

Margin Calls and Operational Risks

A “margin call” occurs when a broker or clearinghouse notifies a client that they must deposit more funds to cover losses. Failing to meet a margin call can lead to the immediate liquidation of the position, often at the worst possible price.

From an operational standpoint, this requires robust back-office systems. Large institutions must be able to move millions of dollars across borders in hours. Any glitch in the payment system or a delay in wire transfers can lead to catastrophic consequences, highlighting the need for sophisticated financial tools and infrastructure.

Best Practices for Corporate Treasurers

Corporate treasurers use derivatives to hedge against interest rate changes or currency fluctuations. For these professionals, variation margin represents a “basis risk.” To manage this, many firms use:

- Collateral Optimization: Using software to determine the most efficient way to allocate cash across different margin accounts.

- Credit Lines: Maintaining pre-arranged lines of credit with banks specifically to fund margin calls during periods of volatility.

- Threshold Agreements: Negotiating specific amounts (thresholds) below which no margin needs to be moved, though these are becoming rarer under modern regulations.

The Future of Margin Requirements in a Digital Economy

As technology continues to reshape the financial sector, the way we calculate and move variation margin is undergoing a digital transformation.

Automation and T+0 Settlement

Currently, most markets operate on a “T+1” (trade plus one day) or “T+2” settlement cycle. However, the rise of blockchain and distributed ledger technology (DLT) is pushing the industry toward “T+0″—instantaneous settlement. In a T+0 world, variation margin would be calculated and moved in real-time as prices change. This would virtually eliminate counterparty risk but would place an even higher premium on instant liquidity.

The Impact of Rising Interest Rates

In a low-interest-rate environment, the “opportunity cost” of holding cash for variation margin is low. However, as interest rates rise, the cost of keeping large sums of cash idle increases. This is driving innovation in the “tokenization” of assets, where firms might eventually use digital versions of bonds that can be transferred as instantly as cash, allowing them to earn interest while still meeting margin requirements.

In conclusion, variation margin is the heartbeat of the financial markets. It is a relentless, daily process that ensures the integrity of trades and the stability of the global economy. By understanding its mechanics, its regulatory importance, and its impact on liquidity, investors and business leaders can better navigate the risks and rewards of the modern financial landscape. Regardless of market direction, the discipline of the variation margin ensures that everyone pays their share, keeping the wheels of global commerce turning safely.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.