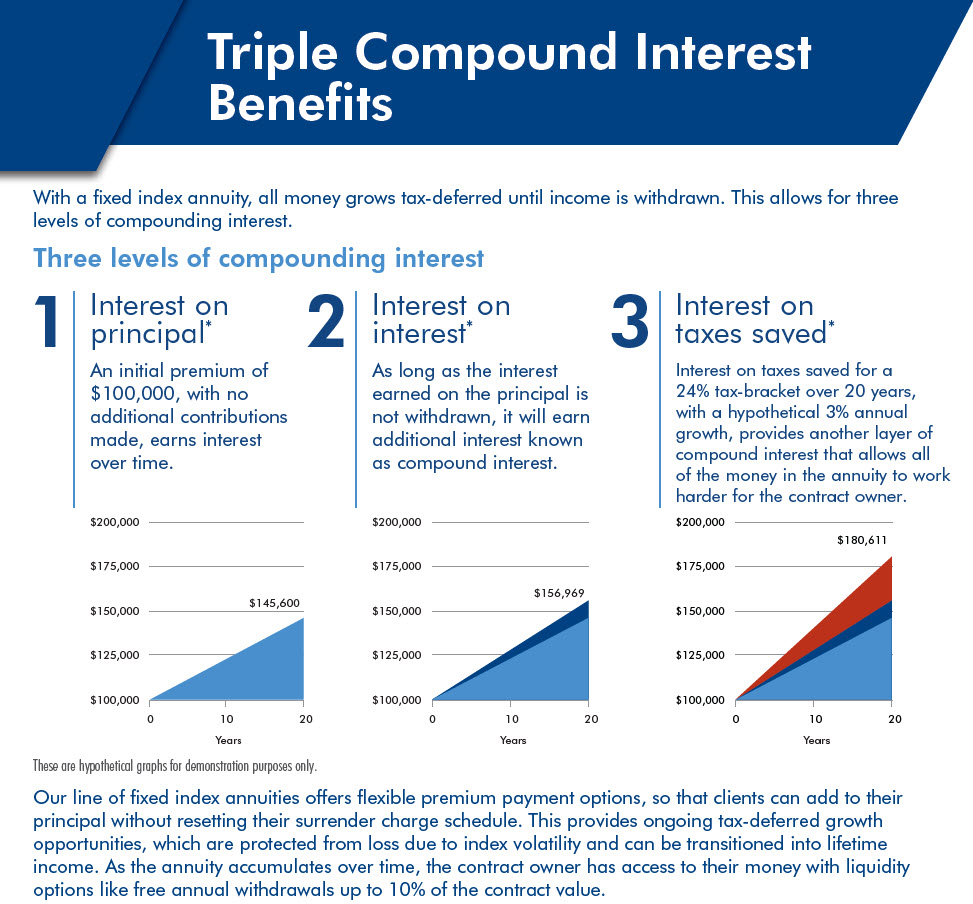

The concept of compound interest is often heralded as the “eighth wonder of the world.” Most investors are familiar with the basic premise: your money earns interest, and then that interest earns interest, creating a snowball effect over time. However, in the sophisticated world of high-level finance and strategic wealth management, standard compounding is merely the baseline. To truly accelerate the path toward financial independence, one must master the art of triple compounding.

Triple compounding is not a single financial product, but rather a synergistic framework that combines three distinct layers of growth: capital appreciation, income reinvestment, and tax efficiency. By aligning these three forces, an investor can minimize “friction”—the fees and taxes that typically slow down growth—and maximize the velocity of their capital. This article explores the mechanics of triple compounding and how you can apply it to your personal investment strategy.

The Mechanics of the Triple Compound Effect

To understand triple compounding, we must first break down the three engines that drive it. While a traditional savings account or a basic stock portfolio might utilize one or two of these engines, the triple compounder ensures all three are firing simultaneously.

Pillar 1: Capital Appreciation (The Growth Engine)

The first layer is the most recognizable: the increase in the market value of an asset. Whether it is a share of a technology company, a piece of commercial real estate, or a diversified index fund, capital appreciation represents the market’s recognition of an asset’s increasing value. In a triple compounding model, you prioritize assets that have the structural capacity to grow their intrinsic value over decades. This isn’t about “timing the market” for a quick flip; it is about “time in the market” with assets that possess high return on equity (ROE).

Pillar 2: Yield and Reinvestment (The Cash Flow Engine)

The second layer involves the dividends, interest, or rental income generated by the asset. In a standard investment scenario, many people use this income to fund their lifestyle. However, in the triple compounding framework, this income is immediately redirected back into the principal. This creates a “secondary snowball.” You are not just waiting for your original shares to go up in price; you are using the “rent” those shares pay you to buy more shares, which in turn will pay more dividends.

Pillar 3: Tax-Efficiency and Friction Reduction (The Optimization Engine)

The third, and often overlooked, layer is the mitigation of tax drag and management fees. Taxes are the single greatest “leak” in a compounding bucket. If an investor earns a 10% return but loses 2% to capital gains taxes and 1% to management fees every year, their effective compounding rate is slashed significantly. Triple compounding utilizes tax-advantaged accounts (like IRAs, 401ks, or ISAs) and low-cost instruments to ensure that 100% of the gains stay within the ecosystem to be reinvested.

Mastering the Growth Engine: Selecting the Right Assets

Triple compounding requires a specific type of underlying asset. Not every investment is capable of sustaining the “triple” effect. For instance, a high-yield bond might offer great income (Pillar 2) but lacks capital appreciation (Pillar 1). Conversely, a speculative “meme stock” might have price volatility but offers no yield and carries high risk.

Seeking “Compounding Machines”

In professional investing circles, a “compounding machine” is a company that can reinvest its own profits at high rates of return. When a company earns a profit and, instead of just sitting on the cash, uses it to build a new factory or acquire a competitor that also generates profit, the company itself is “triple compounding” internally. By owning shares in such companies, you are essentially piggybacking on their internal efficiency.

The Role of Diversified Indexing

For the individual investor, low-cost index funds often serve as the best foundation for triple compounding. These funds capture the growth of the entire market (Pillar 1). When set to “DRIP” (Dividend Reinvestment Plan), they automatically handle Pillar 2. Finally, because index funds have low turnover, they generate fewer “taxable events,” supporting Pillar 3.

Real Estate as a Triple Compounder

Real estate is a classic example of this niche. Property values tend to rise over time (Appreciation), tenants pay rent which can be used to buy more property (Reinvestment), and various tax laws (such as depreciation and 1031 exchanges) allow investors to defer or eliminate taxes (Tax-Efficiency).

The Power of the Reinvestment Snowball

The “Yield and Reinvestment” pillar is where the math of triple compounding truly begins to deviate from linear growth. This is the difference between a portfolio that grows and a portfolio that multiplies.

The Mathematics of DRIPs

A Dividend Reinvestment Plan (DRIP) allows you to use your dividends to purchase more shares of the stock that paid them, often without commission. Over a 30-year horizon, the difference between “taking the cash” and “reinvesting the cash” is staggering. Historical data on the S&P 500 shows that a significant portion of the total returns over the last century came not from price increases, but from the compounding of reinvested dividends.

Compounding in Private Business and Side Hustles

Triple compounding is not limited to the stock market. If you run an online business or a side hustle, you can apply these principles.

- Appreciation: You build the brand and the customer list (the asset value increases).

- Reinvestment: You take the monthly profit and reinvest it into better software or marketing rather than spending it.

- Efficiency: You structure the business to take advantage of deductible expenses, reducing your taxable income.

Psychological Momentum

There is also a behavioral benefit to the reinvestment pillar. Seeing your “share count” increase every quarter, regardless of whether the market price is up or down, provides a psychological cushion. It encourages the investor to stay the course during market downturns, which is essential for the long-term success of any compounding strategy.

Eliminating Friction: The Silent Multiplier

You can have the best growth assets and a perfect reinvestment strategy, but if you ignore the “Optimization Engine,” you are effectively running a race with a weight tied to your ankle. In the world of money, this weight is known as “Tax Drag.”

The “Tax Drag” Phenomenon

Consider two investors, both starting with $100,000 and earning a 8% annual return over 30 years.

- Investor A invests in a taxable account and pays a 20% tax on gains and dividends every year.

- Investor B invests in a tax-sheltered account where growth is protected.

After 30 years, Investor B will have significantly more wealth—potentially hundreds of thousands of dollars more—simply because they didn’t have to pay the “government’s share” annually. By deferring the tax, the money that would have gone to taxes remains in the account to earn more interest the following year. This is the essence of the “third” compound.

Minimizing Management Fees

In the Money niche, we often talk about Expense Ratios. A fee of 1.5% might seem small, but when compounded over 40 years, it can consume nearly one-third of your total potential wealth. Triple compounding demands a ruthless commitment to low-cost investing. Every dollar saved in fees is a dollar that can be put to work in the growth and reinvestment engines.

Asset Location Strategy

Sophisticated investors use “Asset Location” to enhance triple compounding. This involves placing high-yield, tax-heavy assets (like REITs or high-turnover funds) in tax-advantaged accounts, while keeping tax-efficient assets (like low-dividend growth stocks) in taxable brokerage accounts. This strategic placement ensures that the “Tax Shield” is protecting the most vulnerable parts of your portfolio.

Implementing Triple Compounding in Your Portfolio

Transitioning from a basic investment mindset to a triple compounding strategy requires a shift in how you view every dollar that enters your ecosystem. It requires discipline, a long-term horizon, and a focus on “Total Return” rather than just “Price Growth.”

Step 1: Audit Your Current Leakage

The first step is to identify where you are losing money to friction. Are you paying high commissions? Are you holding inefficient funds in taxable accounts? By plugging these holes, you immediately increase your compounding rate without needing the market to perform any better than it already is.

Step 2: Automate the Reinvestment

Human error is the enemy of compounding. Set up your brokerage accounts to automatically reinvest dividends. If you are running a business, set a fixed percentage of profits that must be “re-acquired” by the business before you take a draw. This ensures that the second pillar of triple compounding is always active.

Step 3: Extend Your Time Horizon

The most powerful variable in the compounding equation is Time. Triple compounding looks unimpressive in years one through five. It looks interesting in years ten through fifteen. But in years twenty through forty, it becomes a force of nature. The “Triple” effect creates a vertical move in the wealth curve that standard saving simply cannot match.

Conclusion

Triple compounding is the ultimate “Money” strategy because it addresses the three major factors of wealth: what you earn (Growth), what you do with what you earn (Reinvestment), and what you keep (Tax Efficiency). By mastering these three pillars, you stop working for your money and start ensuring that every cent you own is working three times as hard for you. In an era of economic uncertainty, the ability to build a self-sustaining, friction-free wealth engine is the surest path to long-term financial sovereignty.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.