In the intricate world of corporate finance and accounting, transparency is the cornerstone of trust. Stakeholders, from internal management to external investors, require a clear picture of a company’s financial health. To achieve this clarity, accountants use a specialized tool known as a “contra account.” While the term might sound like complex jargon, it is a fundamental concept that allows businesses to maintain accurate records without losing historical data.

A contra account is essentially an account that reduces the balance of another related account. In the double-entry bookkeeping system, every account has a “normal balance”—either a debit or a credit. A contra account carries a normal balance that is the opposite of its companion account. For example, if an asset account typically has a debit balance, its contra asset account will have a credit balance.

Understanding contra accounts is vital for anyone involved in business finance, as they provide the bridge between “gross” figures and “net” figures. This article explores the mechanics, types, and strategic importance of contra accounts in modern financial management.

1. Understanding the Mechanics of Contra Accounts

To grasp how a contra account works, one must first understand the “normal balance” of standard accounts. In accounting, assets and expenses normally have debit balances, while liabilities, equity, and revenue normally have credit balances. A contra account intentionally defies this logic to act as a corrective or adjusting force.

The Relationship with Normal Balances

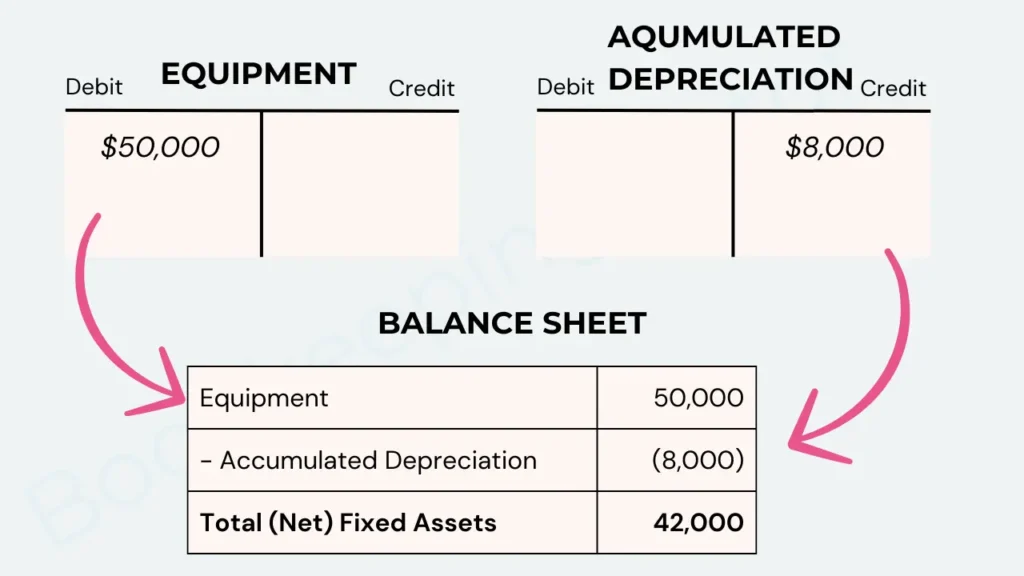

The primary purpose of a contra account is to keep the “gross” amount of a transaction visible while reporting the “net” amount. For instance, if a company buys a piece of machinery for $100,000, that historical cost remains on the books in the Asset account. Over time, as the machine wears down, the company doesn’t simply erase the $100,000. Instead, it uses a contra asset account called “Accumulated Depreciation” to record the loss in value. On the balance sheet, the machinery is listed at its full price, the accumulated depreciation is subtracted, and the “Book Value” (the net amount) is presented to the reader.

How Contra Accounts Maintain the Accounting Equation

The fundamental accounting equation—Assets = Liabilities + Equity—must always stay in balance. Contra accounts help maintain this balance during complex adjustments. By using a contra account instead of directly credit-adjusting an asset, accountants preserve an audit trail. If a business simply reduced the asset account every time it lost value, it would eventually lose track of the original purchase price, making it difficult to calculate taxes, insurance premiums, or replacement costs.

2. Common Types of Contra Accounts in Business Finance

Contra accounts appear across almost every section of the financial statements. They are categorized based on the specific account they offset.

Contra Asset Accounts

This is the most common category. Contra asset accounts carry a credit balance and reduce the total value of a company’s assets.

- Accumulated Depreciation: Used for fixed assets like vehicles, buildings, and equipment. It represents the total amount of depreciation taken on an asset since it was put into service.

- Allowance for Doubtful Accounts: This offsets “Accounts Receivable.” When a company sells goods on credit, it acknowledges that some customers may never pay. Rather than guessing which specific customer will default, the company creates an allowance to estimate potential losses, ensuring the balance sheet doesn’t overstate the cash the company expects to collect.

Contra Revenue Accounts

Found on the income statement, these accounts carry a debit balance and reduce “Gross Sales” to arrive at “Net Sales.”

- Sales Returns and Allowances: When a customer returns a product, the company debits this contra revenue account rather than reducing the Sales account directly. This allows management to track the volume of returns, which can be a vital indicator of product quality issues.

- Sales Discounts: If a business offers a “2/10, n/30” discount (a 2% discount if paid within ten days), the amount of the discount is recorded here. High balances in this account may indicate that a company’s early-payment incentives are highly effective.

Contra Liability and Equity Accounts

- Discount on Bonds Payable: A contra liability account that reduces the face value of a bond. This occurs when a bond is sold for less than its par value because the market interest rate is higher than the bond’s coupon rate.

- Treasury Stock: This is a contra equity account. It represents shares that the company once issued but has since bought back from the open market. Since equity represents ownership, buying back shares reduces the total equity available to outside shareholders.

3. Why Contra Accounts are Vital for Financial Reporting

The use of contra accounts is not just a matter of bookkeeping preference; it is a requirement for following Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS).

Enhancing Transparency and Detail

If a company reported only the “net” value of its assets, an investor might see $50,000 in equipment and assume it is a new, high-functioning machine. However, if the balance sheet shows $500,000 in equipment with $450,000 in Accumulated Depreciation, the investor gains a completely different insight: the company is using very old equipment that will likely need a massive capital injection for replacement very soon. Contra accounts provide this historical context that “netting” lacks.

The Matching Principle and Conservative Accounting

Contra accounts are essential for the “Matching Principle,” which dictates that expenses should be recognized in the same period as the revenues they help generate. For example, by using the “Allowance for Doubtful Accounts,” a company recognizes the potential expense of a bad debt in the same month the sale was made, rather than waiting months or years for the customer to officially go bankrupt. This “conservative” approach prevents businesses from artificially inflating their profits and asset values.

Tax Implications and Asset Valuation

For tax purposes, the distinction between the historical cost of an asset and its accumulated depreciation is crucial. Governments often offer tax breaks based on depreciation schedules. By maintaining a clean contra account for depreciation, a business can easily justify its tax deductions during an audit. Similarly, during a business valuation or sale, having a clear record of “Gross vs. Net” helps buyers understand the age and lifecycle of the company’s infrastructure.

4. Practical Application: Managing Contra Accounts in Modern Business

In the digital age, manual ledger entries for contra accounts are becoming a thing of the past, but the logic remains the same. Effective management requires a blend of software precision and human oversight.

Best Practices for Small Businesses and Side Hustles

Even for small businesses or those earning online income, contra accounts are relevant. If you sell products on platforms like Amazon or Shopify, you shouldn’t just record your “take-home” pay. You should record the “Gross Sales” and then use contra accounts (or expense categories acting as offsets) for “Refunds” and “Platform Fees.” This allows you to see the true cost of doing business and identify if your return rate is eating too much of your margin.

Software and Automation in Tracking Adjustments

Modern accounting software like QuickBooks, Xero, or Sage automates much of the contra account process. When you record a “Return Merchandise Authorization” (RMA), the software automatically hits the Sales Returns account. When you set up a depreciation schedule for a new vehicle, the software creates monthly journal entries that debit Depreciation Expense and credit the Accumulated Depreciation contra account.

However, automation is not foolproof. Business owners must perform regular reconciliations. For instance, the “Allowance for Doubtful Accounts” must be adjusted periodically based on an “Aging of Accounts Receivable” report. If a company finds that its customers are paying more reliably than expected, it may need to reduce the contra account balance to reflect the more optimistic reality.

Conclusion: The Strategic Value of the Negative

In the realm of personal and business finance, we are often taught to avoid negatives. However, the contra account proves that “negative” entries are essential for a positive understanding of financial health. By separating the original cost of an asset or the total volume of sales from their respective adjustments, contra accounts provide a high-definition view of a company’s operational efficiency.

Whether you are an entrepreneur looking to clean up your balance sheet, an investor analyzing a company’s equipment lifecycle, or a student of finance, mastering the contra account is a prerequisite for financial literacy. It ensures that the stories told by financial statements are not just snapshots of the present, but comprehensive narratives of the past and realistic projections for the future. In short, contra accounts turn a simple list of numbers into a powerful strategic tool for long-term business success.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.