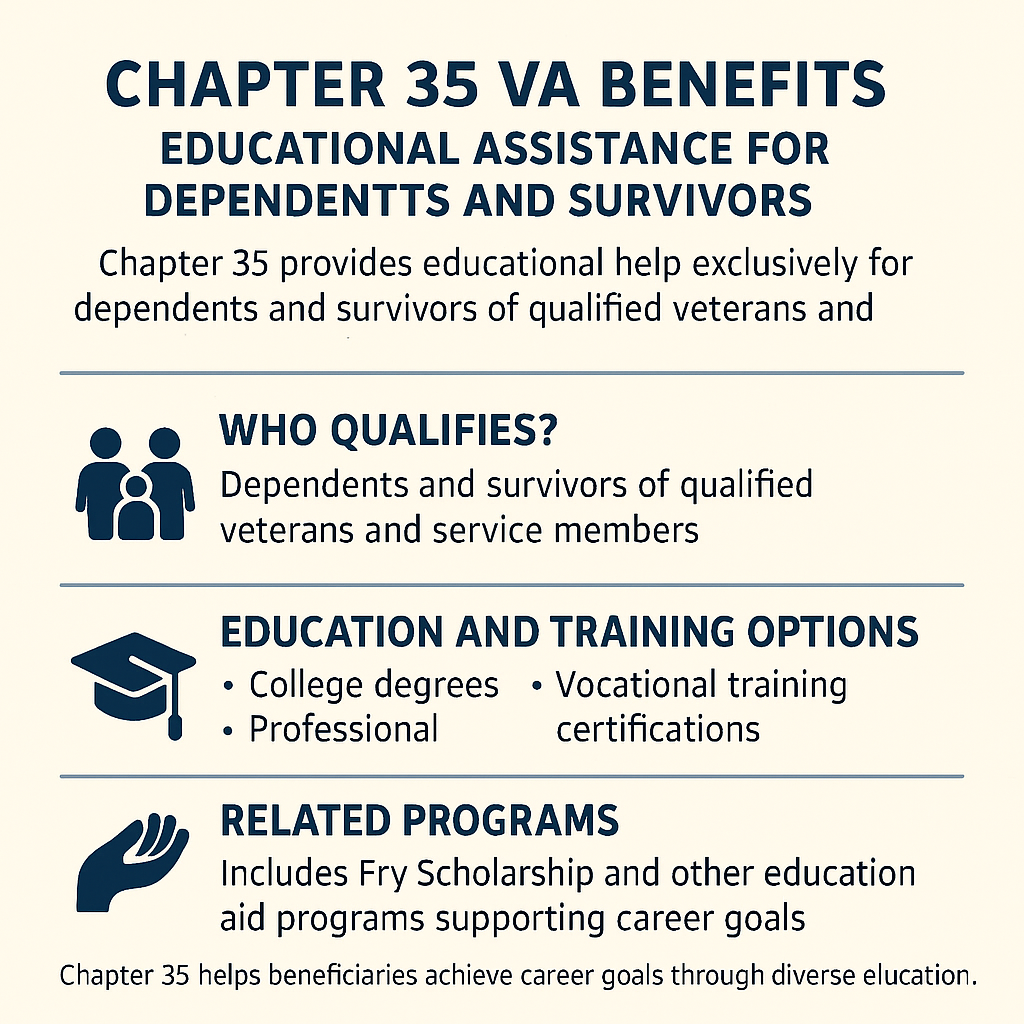

For many families of veterans and service members, the financial burden of higher education can be a daunting obstacle. However, within the landscape of federal financial tools, one specific provision stands out as a cornerstone of support for the dependents of those who have made significant sacrifices for their country. This is known as Chapter 35, or the Survivors’ and Dependents’ Educational Assistance (DEA) program.

Falling under the broader umbrella of personal finance and government-backed financial tools, Chapter 35 is more than just a benefit—it is a strategic financial asset. It provides monthly stipends to eligible survivors and dependents of veterans who have died, been captured, or are permanently and totally disabled as a result of their service. Understanding the mechanics, eligibility, and financial implications of Chapter 35 is essential for any military family planning their long-term financial future.

What is Chapter 35? Defining the DEA Program

At its core, Chapter 35 is a monthly benefit payment designed to help cover the costs of education and training. Unlike many other educational grants that are paid directly to a university, Chapter 35 is unique in its structure and its impact on a family’s cash flow.

The Core Purpose of Chapter 35

The primary goal of the DEA program is to provide a pathway to economic independence for the spouses and children of veterans. The program recognizes that when a service member is significantly disabled or loses their life, the family’s earning potential and savings capacity are often compromised. By providing a steady stream of monthly income dedicated to education, the federal government helps ensure that these dependents can pursue professional careers without the crushing weight of excessive student loan debt.

How Chapter 35 Differs from the Post-9/11 GI Bill

It is a common misconception that Chapter 35 is simply a “transfer” of the veteran’s GI Bill. In reality, Chapter 35 is a distinct program under Title 38 of the U.S. Code. While the Post-9/11 GI Bill (Chapter 33) often covers the full cost of tuition and fees paid directly to the school, Chapter 35 pays a monthly stipend directly to the student.

This means the student is responsible for paying their own tuition and fees to the institution. From a financial planning perspective, this requires more active management of funds, as the student must budget their monthly check to cover housing, books, and tuition installments.

Eligibility Requirements and Who Qualifies

Eligibility for Chapter 35 is strictly defined by the Department of Veterans Affairs (VA). Because it is a significant financial commitment from the government, the criteria are centered on the service member’s status and the dependent’s relationship to them.

Qualifying Veterans and Service Members

To unlock these benefits for their dependents, the veteran or service member must meet one of the following criteria:

- The veteran died or is permanently and totally disabled (P&T) as the result of a service-connected disability.

- The veteran died from any cause while a service-connected P&T disability was in existence.

- The service member is currently missing in action (MIA) or was captured in the line of duty by a hostile force.

- The service member is currently being held by a foreign government or power.

- The service member is hospitalized or receiving outpatient care for a service-connected P&T disability and is likely to be discharged for that disability.

The “Permanent and Total” (P&T) designation is the most common gateway for Chapter 35. This rating implies that the VA does not expect the veteran’s condition to improve, acknowledging the long-term financial strain on the household.

Dependent and Spouse Criteria

The program is available to two primary groups: children and spouses.

- Children: This includes biological children, adopted children, and stepchildren. Benefits are typically available between the ages of 18 and 26, though there are certain circumstances where these limits can be extended (such as military service by the child).

- Spouses: A surviving spouse or the spouse of a P&T disabled veteran remains eligible for 10 to 20 years from the date the VA determines they are eligible or from the date of the veteran’s death.

Age Limits and Timeframes

Timing is a critical component of financial planning with Chapter 35. For children, the “eight-year window” (usually ages 18 to 26) is the standard period for benefit usage. If a child joins the military, their eligibility may be extended by the length of their service. For spouses, the timeframe is longer, reflecting the reality that a spouse may need to pivot careers or return to school later in life to support the family.

Financial Benefits and Monthly Stipend Rates

The most vital aspect of Chapter 35 from a “Money” perspective is the monthly stipend. These rates are adjusted annually to keep pace with inflation and the rising cost of living.

Current Payment Rates for Full-Time and Part-Time Students

As of the current academic cycle, the VA pays a set monthly amount based on the student’s “training time.” For full-time students, this amount is often enough to cover a significant portion of living expenses or community college tuition.

- Full-time: The maximum monthly rate (e.g., ~$1,488 for the 2023-2024 period).

- Three-quarter time: A reduced rate (approx. 75% of the full-time rate).

- Half-time: Approximately 50% of the full-time rate.

- Less than half-time: Payments are limited to the cost of tuition and fees, not to exceed the half-time rate.

By understanding these tiers, a family can calculate the “return on investment” for different course loads. A student taking 12 credits (full-time) receives the highest level of financial support, making it the most efficient way to utilize the 36 months of entitlement.

How Benefits are Disbursed

Unlike federal student loans, Chapter 35 benefits are paid “in arrears.” This means the student receives the payment for a specific month at the beginning of the following month. For example, the payment for September’s classes arrives in early October. From a personal finance standpoint, this requires the student to have an initial “buffer” of savings to cover their first month of rent and expenses before the VA payments begin to flow.

Covering Tuition, Books, and Living Expenses

Because the money is paid directly to the student, they have the flexibility to use it however they see fit. A student attending a school with a full-tuition scholarship can use the Chapter 35 stipend entirely for housing and food, essentially providing them with a “salary” to attend school. Conversely, a student at an expensive private university will likely need to supplement Chapter 35 with other grants or part-time work to cover the tuition gap.

Approved Programs and Educational Opportunities

Chapter 35 is remarkably versatile. It is not restricted to traditional four-year degrees; it covers a wide range of pathways designed to increase the recipient’s earning potential.

Degree Programs and Vocational Training

The most common use of Chapter 35 is for associate, bachelor’s, master’s, or doctoral degrees at accredited colleges and universities. However, it also covers vocational and technical schools. This is a vital financial tool for those looking to enter skilled trades—such as HVAC, plumbing, or coding bootcamps—where the entry-to-employment timeline is shorter than a traditional degree.

Certification Tests and On-the-Job Training

Financial support extends to non-traditional learning as well. The DEA program can reimburse students for the cost of national standardized tests (like the SAT or LSAT) and professional certification exams (like a CPA or PMP). Additionally, it can be used for “On-the-Job Training” (OJT) or apprenticeships. In these cases, the student earns a wage from their employer while receiving a supplemental stipend from the VA, effectively boosting their income while they learn a trade.

Special Restorative and Specialized Vocational Training

For dependents with physical or mental disabilities that may hinder their pursuit of a standard education, Chapter 35 offers “Special Restorative Training.” This can include speech and voice therapy, lip reading, or braille reading. This specific sub-section of the benefit ensures that financial barriers do not prevent dependents with special needs from reaching their full potential.

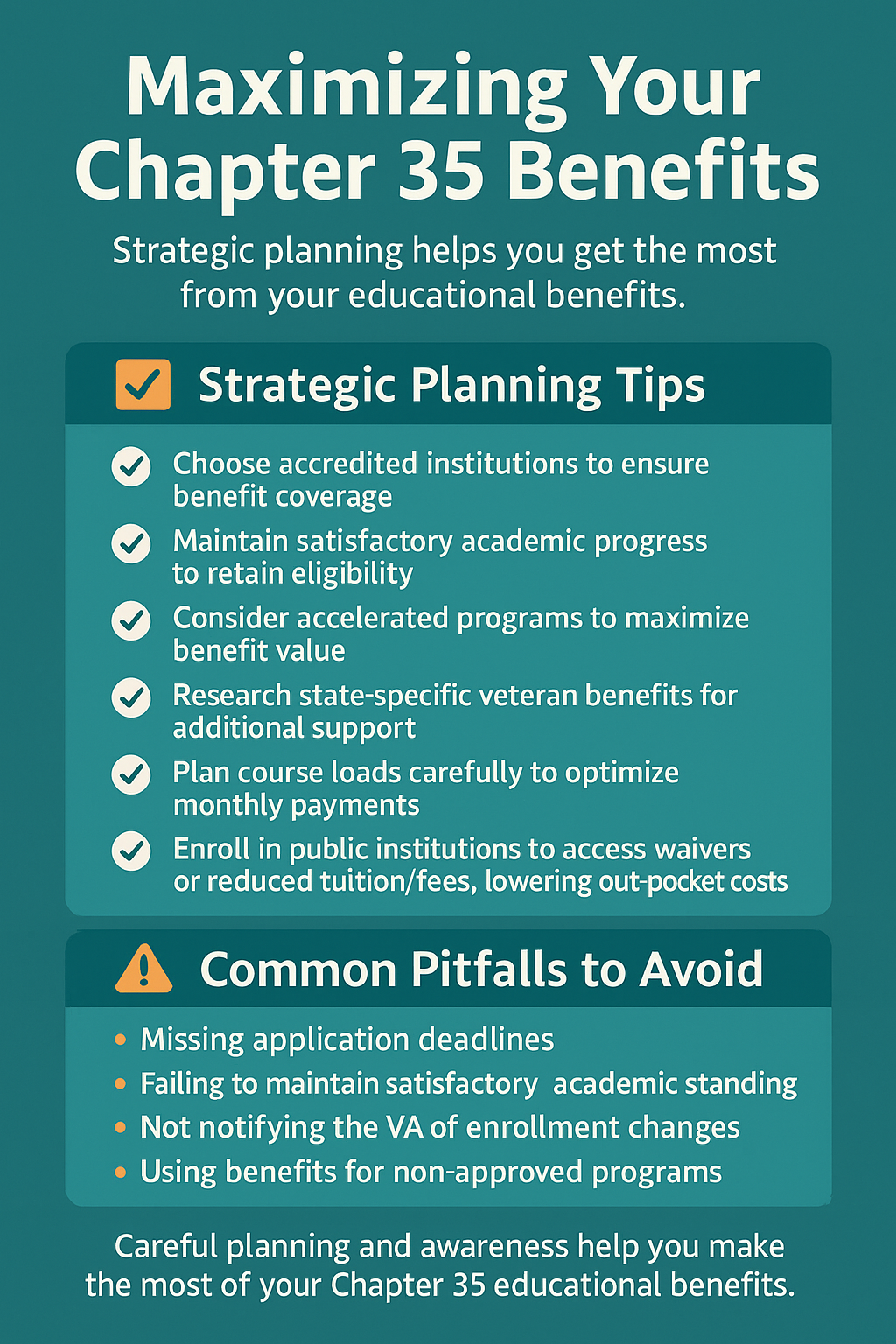

How to Apply and Maximize Your Benefits

To transform Chapter 35 from a theoretical benefit into an actual financial resource, one must navigate the application process and manage the entitlement strategically.

The Application Process: Step-by-Step

- Verify Eligibility: Ensure the veteran has the P&T rating or meet the other death/service criteria.

- Submit VA Form 22-5490: This is the formal “Dependents’ Application for VA Education Benefits.” It can be completed online via the VA.gov portal.

- Certificate of Eligibility (COE): Once approved, the VA will mail a COE. This document is the “gold ticket” that must be presented to the school’s School Certifying Official (SCO).

- Enrollment Certification: The school must certify the student’s enrollment in specific classes before the VA will trigger the monthly payments.

Common Pitfalls and How to Avoid Them

The most common financial mistake is failing to account for the “45-month vs. 36-month” rule. Historically, Chapter 35 offered 45 months of benefits. However, for those who first became eligible after August 1, 2018, the entitlement is capped at 36 months.

Miscalculating this can leave a student without funding for their final year of a five-year program or a graduate degree. It is essential to map out the 36-month timeline to ensure that every month of entitlement is used toward a credit-bearing course that moves the student closer to graduation.

Strategic Financial Planning with Chapter 35

For families with multiple children or those eligible for multiple benefits (such as the Fry Scholarship), the choice of which benefit to use is a complex financial decision. The Fry Scholarship (Chapter 33) might cover full tuition at a high-cost university, whereas Chapter 35 might be more profitable if the student is attending a low-cost state school or has other scholarships.

Consulting with a financial advisor who specializes in military benefits can help families “stack” benefits. Many states also offer tuition waivers for Chapter 35 recipients at public universities. When a student combines a state tuition waiver with the Chapter 35 monthly stipend, they are essentially being paid to earn their degree—a powerful financial foundation that sets the stage for a lifetime of wealth building and professional success.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.