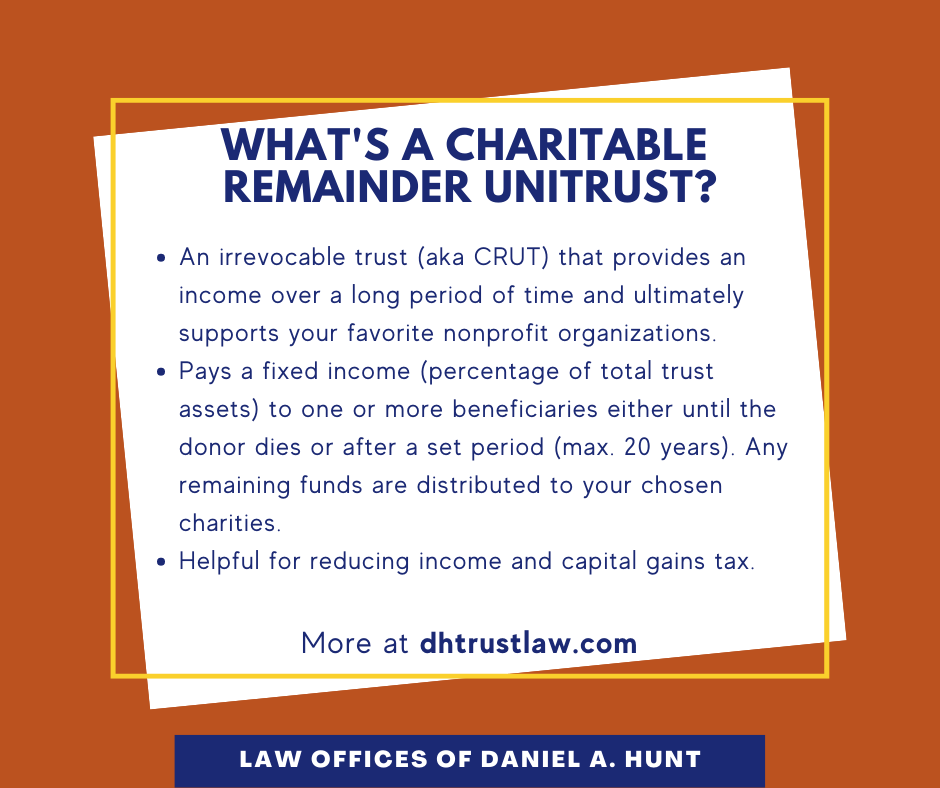

In the sophisticated landscape of estate planning and wealth management, the “Unitrust”—formally known as a Charitable Remainder Unitrust (CRUT)—stands as one of the most powerful tools for high-net-worth individuals. It is a unique financial vehicle that allows an investor to achieve three seemingly divergent goals simultaneously: creating a sustainable income stream, securing significant tax advantages, and establishing a lasting philanthropic legacy.

At its core, a Unitrust is an irrevocable trust that pays a set percentage of its value to a named beneficiary for a specific period, after which the remaining assets are transferred to a designated charity. Unlike fixed-income vehicles, the Unitrust is designed to fluctuate with market performance, offering a hedge against inflation and a way to participate in market growth even after assets have been moved out of a personal portfolio. For the modern investor, understanding the mechanics, benefits, and strategic applications of a Unitrust is essential for sophisticated long-term financial health.

Understanding the Mechanics of a Unitrust

A Unitrust operates on a specific logic defined by the Internal Revenue Code. It is a “split-interest” transition, meaning the benefits of the assets are divided between a non-charitable beneficiary (often the donor or their family) and a qualifying charitable organization. To grasp how this works in practice, one must look at the legal structure and the specific valuation methods that differentiate it from other trust types.

The Legal Structure and Participants

Every Unitrust involves four primary roles. First is the Grantor (or donor), the individual who funds the trust with assets such as highly appreciated stocks, real estate, or private business interests. Second is the Trustee, who manages the assets and ensures the trust complies with IRS regulations. Third is the Income Beneficiary, who receives the annual payments for a term of years (not to exceed 20) or for the duration of their lifetime. Finally, there is the Charitable Remainder Beneficiary, the non-profit organization that receives whatever is left in the trust after the income period ends.

How the Payout Formula Works

The defining characteristic of a Unitrust is the “unitrust amount.” By law, the trust must pay out a fixed percentage of its net fair market value, which must be at least 5% but no more than 50% of the value of the assets. Because this is a percentage rather than a flat dollar amount, the actual cash flow to the beneficiary changes every year. If the trust’s investments perform well and the principal grows, the payout increases. Conversely, if the market dips, the payout decreases. This “tide-like” movement ensures that the beneficiary’s interests are aligned with the growth of the trust’s corpus.

Annual Revaluation: The Defining Feature

Unlike a Charitable Remainder Annuity Trust (CRAT), which pays a fixed sum regardless of market conditions, a Unitrust requires an annual revaluation of its assets. On a specific date each year—often the first business day of the year—the trustee calculates the total value of the trust’s holdings. The agreed-upon percentage is then applied to this new figure to determine the distribution for the coming year. This mechanism provides a natural inflation hedge; as the cost of living rises and asset values (ideally) increase, the income stream from the Unitrust typically scales upward, preserving the donor’s purchasing power.

The Financial Advantages of Establishing a CRUT

The popularity of the Unitrust in wealth management is largely driven by its extraordinary tax efficiency. For investors sitting on highly appreciated assets, the CRUT provides a “tax-free environment” to reposition capital.

Capital Gains Tax Deferral and Avoidance

Perhaps the most significant benefit of a Unitrust is the ability to sell highly appreciated assets without immediately triggering capital gains tax. When a donor transfers an asset (like a block of tech stock with a low cost basis) into a CRUT, the trust—being a tax-exempt entity—can sell that asset at its current market value and reinvest the full proceeds. If the donor had sold the stock personally, they might have lost 15% to 23.8% of the value to federal capital gains taxes, plus potential state taxes. Inside the CRUT, 100% of the proceeds are put to work, compounding the growth potential of the income-producing portfolio.

Immediate Income Tax Deductions

When you fund a Unitrust, the IRS allows you to take an immediate charitable income tax deduction. This deduction is not for the full value of the assets placed in the trust, but rather for the “present value” of the remainder interest that will eventually go to the charity. This value is calculated using IRS actuarial tables, considering the donor’s age, the payout percentage, and current interest rates. This deduction can be used to offset the donor’s Adjusted Gross Income (AGI), providing significant tax relief in the year the trust is funded, with the ability to carry forward any unused deduction for up to five additional years.

Estate Tax Reduction and Wealth Preservation

For those with estates exceeding federal exemption limits, a Unitrust serves as an effective estate-shrinking tool. Because the assets transferred to the CRUT are no longer part of the donor’s taxable estate, they are not subject to the 40% federal estate tax upon the donor’s death. While this removes assets from the direct inheritance of heirs, many savvy investors use the tax savings and the increased income stream from the CRUT to purchase a life insurance policy within an Irrevocable Life Insurance Trust (ILIT). This “wealth replacement” strategy allows the donor to provide for charity, enjoy an income stream, and still leave a significant, tax-free legacy to their heirs.

Unitrust vs. Annuity Trust: Which Is Right for Your Portfolio?

When deciding on a charitable trust structure, investors often choose between the Unitrust (CRUT) and the Charitable Remainder Annuity Trust (CRAT). While they share the same tax-exempt status, their risk profiles and income characteristics differ significantly.

Fixed Income vs. Variable Potential

The CRAT provides a fixed, guaranteed dollar amount every year. This is ideal for older investors who prioritize absolute certainty and do not want their income affected by market volatility. However, the CRAT is rigid; once the payout is set, it can never be changed. The CRUT, by contrast, offers variable income. While this introduces the risk of lower payments during market downturns, it offers the upside of participating in bull markets. For an investor with a longer time horizon, the CRUT is often the superior choice because it allows the income stream to grow over decades.

Inflation Protection Considerations

Inflation is the silent killer of fixed-income portfolios. A CRAT payment of $50,000 may feel substantial today, but in twenty years, its purchasing power could be halved. Because the CRUT is revalued annually, it has an inherent mechanism to combat inflation. As the underlying assets (equities, real estate, etc.) rise in value due to inflationary pressures, the 5% or 6% payout from the trust is applied to a larger base, effectively giving the beneficiary a “raise” that keeps pace with the economy.

Complexity and Administrative Overhead

It is important to note that the CRUT is more administratively complex than the CRAT. Because the assets must be valued every year, the trustee must perform rigorous accounting, especially if the trust holds “hard-to-value” assets like private equity or real estate. These appraisal costs can eat into the trust’s returns. However, for most investors, the benefits of flexibility and inflation protection far outweigh the annual administrative costs.

Strategic Implementation: Who Should Consider a Unitrust?

The Unitrust is not a “one-size-fits-all” product; it is a surgical instrument best used in specific financial scenarios. Identifying when to deploy this tool is the hallmark of advanced financial planning.

High-Net-Worth Individuals and Business Owners

Business owners facing a liquidity event—such as the sale of a company—are prime candidates for a Unitrust. By transferring a portion of their business interests into a CRUT before the sale, they can avoid the massive tax hit on the gain, diversify their wealth into a balanced portfolio, and create a lifetime pension for themselves. This “pre-sale” planning is one of the most effective ways to transition from active business ownership to a passive, income-generating retirement.

Retirees Seeking Sustainable Cash Flow

For retirees who are “asset rich but cash poor”—perhaps owning a large portfolio of non-dividend-paying stocks or undeveloped land—the Unitrust offers a way to convert those assets into cash flow without the “tax haircut” associated with a standard sale. It provides a structured way to draw down wealth while ensuring that the principal is managed professionally.

Philanthropically Minded Investors

At its heart, the Unitrust is a gift. It is an ideal vehicle for individuals who already plan on leaving a significant portion of their estate to a university, hospital, or house of worship. By using a CRUT, the donor receives the “warm glow” of giving and the formal recognition from the charity during their lifetime, while still retaining the economic use of the assets for as long as they live.

Conclusion

The Unitrust represents a sophisticated intersection of private wealth and public good. By utilizing the CRUT structure, investors can navigate the complexities of the tax code to protect their capital from heavy taxation, generate a flexible income stream that responds to market growth, and fulfill their charitable aspirations. In an era of economic uncertainty and shifting tax landscapes, the Unitrust remains a foundational element of high-level financial strategy, proving that it is indeed possible to do well for oneself while doing good for the world.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.