In the world of personal and business finance, numbers are the language of progress. However, raw data often fails to tell the full story without the context of scale. This is where the percentage becomes the most powerful tool in a financier’s arsenal. Whether you are calculating the return on an investment, determining the impact of inflation on your purchasing power, or analyzing the profit margins of a scaling startup, understanding how to work out the percentage is fundamental to making informed, data-driven decisions.

Percentages allow us to standardize comparisons. They turn abstract figures into actionable insights, enabling us to compare a small-cap stock’s growth to a blue-chip dividend with a common denominator. This guide explores the mathematical foundations and practical applications of percentage calculations within the realm of money, investing, and financial management.

The Fundamentals of Financial Mathematics

Before diving into complex portfolio analysis, one must master the basic mechanics of percentage calculations. In financial terms, a percentage represents a fraction of 100, providing a standardized way to express ratios.

Understanding the Basic Percentage Formula

The most basic formula for finding a percentage is:

(Part / Whole) × 100 = Percentage

In a financial context, this is often used for budgeting. If your total monthly income is $5,000 and your rent is $1,500, you determine the percentage of your income spent on housing by dividing 1,500 by 5,000 (0.3) and multiplying by 100 to get 30%. Mastering this simple movement of decimals is the first step toward high-level financial clarity.

Converting Decimals to Percentages for Quick Budgeting

Experienced investors often skip the “multiply by 100” step and work directly with decimals. In financial modeling—such as calculating a 5% interest rate—it is more efficient to use the decimal 0.05. Understanding that “per cent” literally means “per hundred” allows you to quickly shift decimal points two places to the right. This skill is invaluable when reading fast-paced market tickers or reviewing bank statements where interest yields are often presented in decimal formats.

Calculating Growth and Returns in Personal Finance

Wealth creation is rarely about the absolute dollar amount gained; it is about the rate of growth relative to the capital deployed. This is where percentage-based metrics like ROI (Return on Investment) and YoY (Year-over-Year) growth become essential.

How to Determine Investment ROI

Return on Investment is perhaps the most critical percentage in the world of money. It measures the efficiency of an investment. The formula is:

((Current Value – Initial Cost) / Initial Cost) × 100

For example, if you purchased shares of a tech company for $10,000 and their value increased to $12,500, your capital gain is $2,500. To find the percentage return, you divide $2,500 by the original $10,000, resulting in a 25% ROI. This percentage allows you to compare the performance of your stock portfolio against other asset classes, such as real estate or bonds, regardless of the different entry prices.

Analyzing Year-over-Year (YoY) Financial Growth

For long-term financial planning, looking at a single snapshot of time is insufficient. Investors use YoY growth percentages to track performance across fiscal years. This calculation helps smooth out seasonal fluctuations. If your side business earned $50,000 in 2022 and $65,000 in 2023, the percentage increase is calculated by finding the difference ($15,000), dividing it by the previous year’s total ($50,000), and multiplying by 100. This 30% growth rate provides a much clearer picture of business health than the raw $15,000 figure alone.

Managing Debt: Interest Rates and APR Calculations

While percentages can work for you in investments, they can work against you in the form of debt. Understanding how banks and lenders use percentages is vital for maintaining a healthy credit profile and minimizing interest expenses.

The Impact of Compound Interest on Your Savings

Compound interest is often called the “eighth wonder of the world” because it involves calculating a percentage not just on your principal, but on the interest already earned. The formula for compound interest is more complex, but the core concept relies on the percentage rate. A 7% annual return compounded monthly will yield a higher effective rate than one compounded annually. For a saver, understanding how these percentages stack over 20 or 30 years is the difference between a modest retirement and significant wealth.

Calculating the Real Cost of a Loan

When taking out a mortgage or an auto loan, the “sticker price” interest rate can be deceiving. The Annual Percentage Rate (APR) provides a more accurate percentage because it includes both the interest rate and any additional fees or costs associated with the loan. To work out the true cost of debt, you must look at the APR percentage. A seemingly small 1% difference in a mortgage interest rate can result in tens of thousands of dollars in additional payments over a 30-year term, illustrating why every percentage point matters in high-stakes finance.

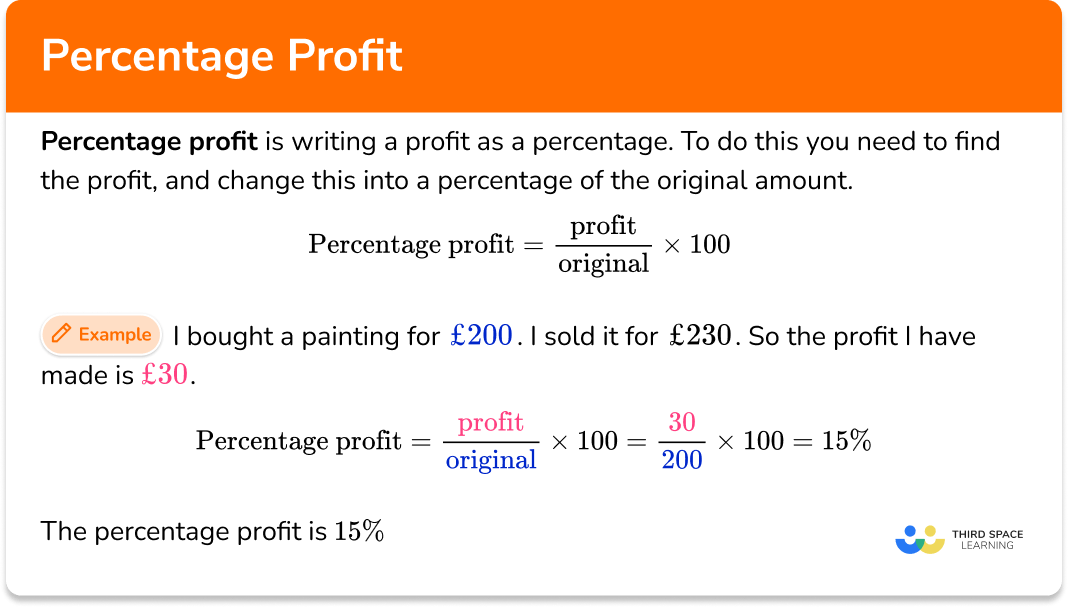

Business Finance: Profit Margins and Markups

For entrepreneurs and business owners, percentages are the primary indicators of operational efficiency. High revenue means very little if the percentage of that revenue retained as profit is negligible.

Gross Profit vs. Net Profit Percentages

Understanding the difference between gross and net profit margins is essential for business sustainability.

- Gross Profit Margin: (Gross Profit / Revenue) × 100. This shows the percentage of revenue exceeding the cost of goods sold.

- Net Profit Margin: (Net Income / Revenue) × 100. This is the “bottom line” percentage, showing how much of every dollar earned is actual profit after all expenses, taxes, and interest.

A business might have a high gross margin of 70%, but if its net margin is only 5%, it suggests that administrative or overhead costs are consuming too much of the capital.

Strategic Pricing Using Percentage Markups

Pricing a product requires a firm grasp of percentages. A “markup” is the percentage added to the cost of a product to derive the selling price. If a product costs $50 to manufacture and you want a 50% markup, you sell it for $75. However, beginners often confuse markup with margin. A 50% markup results in only a 33.3% profit margin. Knowing how to work out these specific percentages ensures that a business remains solvent and can cover its indirect costs.

Practical Tax and Discount Calculations

On a day-to-day basis, we encounter percentages most frequently through taxation and consumer discounts. These calculations are necessary for accurate budgeting and price comparisons.

Working Out Sales Tax and VAT

In many regions, the price on the tag is not the final price. To calculate the total cost including sales tax, you convert the tax percentage to a decimal, add 1, and multiply by the price. For example, if a laptop costs $1,000 and the sales tax is 8.5%, you multiply 1,000 by 1.085 to get a total of $1,085. In business accounting, working backward to find the original price before tax (Price / 1.085) is equally important for tax filing and internal audits.

Maximizing Savings During Seasonal Discounts

Retailers often use percentages to lure consumers, but the psychological impact can sometimes obscure the actual value. To work out a discount, subtract the percentage from 100, convert to a decimal, and multiply by the original price. If an item is $200 with a “30% off” tag, you are paying 70% of the price. $200 × 0.70 = $140. Comparing these percentages across different vendors allows for “opportunity cost” analysis, helping you decide where your capital is best deployed.

Conclusion: The Power of Proportional Thinking

Mastering how to work out the percentage is more than a mathematical exercise; it is a shift in mindset toward proportional thinking. In the world of money, absolute numbers are often distractions. A $1,000 gain is impressive for a $5,000 portfolio (20%), but negligible for a $1,000,000 portfolio (0.1%).

By consistently applying percentage calculations to your income, investments, debts, and expenses, you gain a level of financial oversight that protects you from market volatility and predatory lending. Whether you are using a simple calculator or building a complex financial spreadsheet, the ability to interpret the world through percentages is a hallmark of financial literacy and the foundation of long-term wealth accumulation.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.