In the world of real estate and property management, the term “foundation” is often used both literally and figuratively. Financially speaking, the stability of a physical structure is inextricably linked to the stability of the investment itself. When concrete slabs—be they driveways, warehouse floors, or sidewalks—begin to sink or settle, they represent a literal erosion of capital. This is where “mud jacking” enters the conversation.

While the term may sound like a gritty construction process, in the context of personal finance and asset management, mud jacking is a strategic intervention designed to preserve equity and prevent catastrophic financial loss. Understanding what a mud jack is, how the process works, and the economic rationale behind it is essential for any homeowner, real estate investor, or commercial property manager looking to protect their bottom line.

The Economics of Foundation Repair: Why Mud Jacking Matters to Your Bottom Line

At its core, mud jacking is a concrete leveling technique used to raise sunken or uneven slabs by injecting a specialized material underneath them. From a financial perspective, it is a “corrective maintenance” expense that serves as a hedge against the much higher cost of total demolition and replacement.

Defining Mud Jacking in a Financial Context

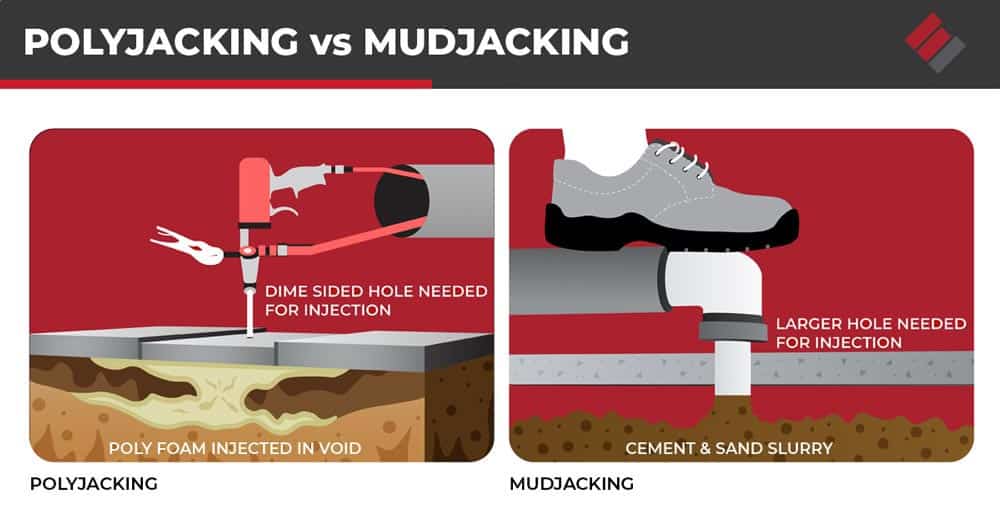

Mud jacking, often referred to as slab leveling or pressure grouting, involves drilling small holes into a sunken concrete slab. A “slurry”—typically a mixture of water, soil, sand, and cement—is pumped through these holes under high pressure. This mixture fills the voids beneath the slab and creates upward pressure, lifting the concrete back to its original position.

In the realm of personal finance, mud jacking is the ultimate “low-cost, high-impact” repair. It addresses the symptom of soil erosion or compaction without requiring the removal of the existing asset. By understanding this process, investors can make informed decisions about property maintenance that prioritize cash flow over unnecessary capital expenditures.

Preventing Diminishing Returns on Property Value

Real estate is an asset class that requires constant upkeep to maintain its valuation. Sunken concrete is more than an aesthetic eyesore; it is a red flag to appraisers and potential buyers. If left unaddressed, a minor dip in a walkway can lead to water pooling, which eventually compromises the structural integrity of the main building foundation.

From a money management standpoint, ignoring the need for a mud jack is an exercise in diminishing returns. The longer the problem persists, the more expensive the solution becomes. By the time a slab has cracked beyond the point of repair, the owner is no longer looking at a minor maintenance cost but a major capital loss. Mud jacking acts as a financial circuit breaker, stopping the “bleeding” of property value before it becomes a total loss.

Mud Jacking vs. Total Replacement: A Cost-Benefit Analysis

When a property owner identifies a sinking slab, they are generally faced with two choices: replace the concrete or level it. A rigorous cost-benefit analysis almost always favors the latter, making mud jacking a preferred tool for the fiscally responsible.

Upfront Costs vs. Long-Term Savings

The most compelling financial argument for mud jacking is the immediate price difference. On average, mud jacking costs between 30% and 50% of the cost of pouring new concrete. For a large commercial parking lot or a long residential driveway, this can translate into thousands, or even tens of thousands, of dollars in immediate savings.

Furthermore, new concrete requires a significant time investment. It must be poured, finished, and allowed to cure for several days or weeks before it can bear weight. In a business environment, this downtime represents “opportunity cost”—lost revenue from inaccessible parking or loading docks. Mud jacking, conversely, allows for near-immediate use. The ability to return an asset to service within hours rather than days is a significant factor in maintaining consistent operational cash flow.

The Hidden Costs of Ignoring Sunken Concrete

Failing to invest in mud jacking often leads to “secondary financial impacts.” These include:

- Water Damage: Improperly sloped concrete can direct water toward the home’s foundation, leading to basement flooding and mold remediation costs that far exceed the price of leveling.

- Infrastructure Strain: Sunken slabs can put pressure on underground plumbing and gas lines, leading to expensive utility repairs.

- Inflationary Pressure: The cost of raw materials (cement, aggregate, and labor) for new concrete is subject to market volatility. Mud jacking uses fewer materials and less labor, making it a more stable and predictable expense in a fluctuating economy.

Real Estate Investment Strategy: Using Concrete Repair to Boost Equity

For real estate investors, particularly those engaged in “fix-and-flip” strategies or BRRRR (Buy, Rehab, Rent, Refinance, Repeat), mud jacking is a secret weapon for boosting equity with minimal capital outlay.

Curb Appeal and Marketability

In the competitive real estate market, first impressions are directly tied to the final sale price. A house with a jagged, uneven sidewalk or a sunken garage floor immediately signals to a buyer that the property has been neglected. This perception leads to “lowball” offers and extended days on the market.

By utilizing mud jacking, an investor can restore the property’s “curb appeal” for a fraction of the cost of a full renovation. This creates a psychological sense of security for the buyer, who perceives the home as well-maintained. In many cases, a $1,500 mud jacking job can prevent a $10,000 reduction in the final sale price, yielding a massive return on investment (ROI).

Navigating Home Inspections and Closing Negotiations

During the “due diligence” phase of a real estate transaction, home inspectors are trained to look for trip hazards and drainage issues. An inspection report citing “unstable concrete slabs” can be a deal-killer or a powerful leverage point for a buyer to demand expensive concessions.

Smart investors get ahead of the inspection by mud jacking before the house hits the market. By providing documentation that the concrete has been professionally leveled and stabilized, the seller eliminates a potential point of negotiation. This proactive financial strategy ensures that the seller retains as much equity as possible during the closing process.

Scaling the Investment: Commercial Applications and Asset Management

The financial benefits of mud jacking are not limited to residential properties. For commercial real estate (CRE) owners and industrial facility managers, the stakes are even higher.

Protecting Liability and Reducing Insurance Premiums

From a business finance perspective, “risk management” is a primary pillar of profitability. Uneven concrete is a significant liability; it is a primary cause of “slip and fall” accidents. In the United States, the average cost of a slip-and-fall lawsuit can reach tens of thousands of dollars in legal fees and settlements.

Commercial property owners use mud jacking to mitigate this risk. By maintaining level walkways and warehouse floors, they reduce the likelihood of worker’s compensation claims and third-party liability suits. Furthermore, many insurance providers offer lower premiums to property owners who can demonstrate a proactive maintenance schedule. In this way, mud jacking is not just a repair; it is an insurance-optimizing strategy.

Strategic Budgeting for Large-Scale Property Maintenance

For those managing large portfolios—such as apartment complexes, retail centers, or industrial parks—budgeting for capital expenditures (CapEx) is a delicate balancing act. If a manager replaces every piece of cracked concrete, they will quickly exhaust their reserve funds, leaving little for other essential upgrades like roofing or HVAC systems.

Mud jacking allows for “surgical” maintenance. It enables managers to extend the lifecycle of existing concrete assets by another 10 to 15 years. By deferring the massive cost of replacement through strategic leveling, asset managers can allocate their capital more effectively, investing in high-yield upgrades that increase the property’s Net Operating Income (NOI) and overall market value.

Conclusion: The Financial Wisdom of the Mud Jack

The question “what is a mud jack?” may begin with a technical explanation of pumps and slurry, but the answer ends with financial prudence. Whether you are a homeowner looking to protect your most significant personal asset, an investor seeking to maximize ROI, or a commercial manager aiming to reduce liability and preserve CapEx, mud jacking represents a sophisticated approach to money management.

In an era where the cost of materials and labor continues to rise, the ability to repair rather than replace is a vital financial skill. Mud jacking offers a path to structural stability that respects the constraints of a budget, proving that the best way to build wealth is often to ensure that the ground you are standing on—literally and financially—remains level.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.