In the complex ecosystem of personal finance and corporate management, we are often identified by a dizzying array of digits. From Social Security numbers and bank account routing digits to credit card tokens and tax identification numbers, these sequences act as the keys to our financial lives. However, one of the most common yet frequently misunderstood identifiers is the “Group Number.”

Found most prominently on health insurance cards and corporate benefits documentation, the group number is far more than a random string of characters. It is a fundamental pillar of how large-scale financial contracts are organized, how risk is managed, and how billions of dollars in claims are processed annually. For the individual consumer, understanding the group number is a vital step in financial literacy, ensuring that benefits are maximized and out-of-pocket costs are minimized. For the business professional, it represents the structural backbone of employer-sponsored financial security.

Understanding the Fundamental Structure of a Group Number

To understand what a group number is, one must first understand the concept of “group financial products.” Unlike individual insurance or investment plans that are tailored to one person’s specific risk profile, group plans are designed for a collective—usually the employees of a specific company or members of a professional organization.

Definition and Primary Purpose

At its core, a group number is a unique identifier assigned by a financial institution (usually an insurance carrier or a benefits administrator) to a specific group of people covered under a single master contract. When a company like a multinational corporation or a small local business signs a deal with a provider to offer benefits to its staff, the provider generates a group number. This number serves as a shorthand for the entire set of rules, coverage limits, and pricing structures negotiated between that company and the provider.

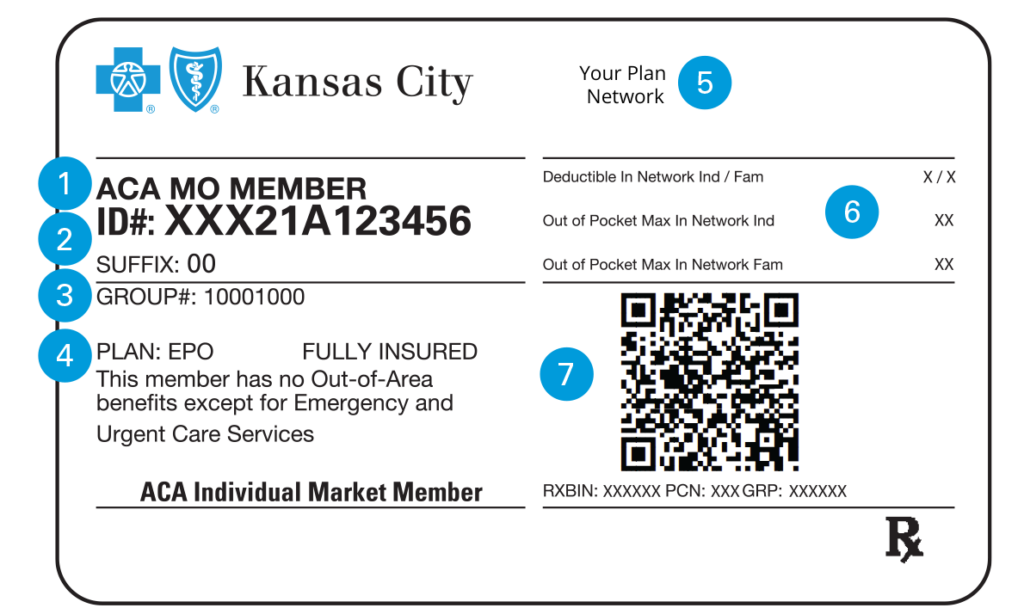

The Critical Distinction: Member ID vs. Group Number

One of the most common points of confusion for individuals navigating their financial paperwork is the difference between their Member ID and the Group Number.

- The Member ID: This is your personal identifier. It is unique to you (and often your dependents) and is used to track your specific claims, history, and usage of the plan.

- The Group Number: This is shared by every single person in your organization who is on the same plan. If you work for “Company A,” you and your 500 colleagues will likely have the exact same group number. It tells the service provider exactly which contract governs your benefits and what your employer has agreed to pay versus what you are responsible for paying.

The Economic Power of the Group: Risk Pooling and Premiums

From a “Money” niche perspective, the group number is the symbol of collective bargaining and risk management. It represents the transition from individual financial vulnerability to collective financial strength.

The Financial Mechanics of Risk Pooling

In the world of finance and insurance, “risk” is the primary variable that determines cost. If an individual seeks health or life insurance independently, the provider assesses that specific individual’s health, age, and lifestyle. This can lead to prohibitively high premiums.

However, when people are organized under a group number, they participate in “risk pooling.” The insurance company looks at the group as a single entity. They assume that while a few members of the group might have high expenses, many others will have very low expenses. This averages out the cost across the entire group, allowing the provider to offer lower premiums to everyone. The group number is the administrative tag that holds this pool together.

Negotiated Rates and Corporate Bargaining

When a company manages a large workforce, they use the volume of their employees to negotiate better rates with financial institutions. A group number is essentially a code for a “bulk discount.” When you present your group number at a pharmacy or a doctor’s office, you are tapping into a pre-negotiated price list that is often significantly lower than the “retail” price an uninsured individual would pay. This is why the group number is a crucial component of an employee’s total compensation package; it represents hidden savings that contribute to an individual’s overall net worth.

Navigating Financial Documentation: Where to Find and Use Your Group Number

For many, the only time they think about a group number is when they are prompted for it at a point of service. However, knowing where this information lives is a key part of personal financial organization.

Locating the Number on Cards and Portals

The most common location for a group number is on a physical or digital insurance card. It is typically labeled clearly as “Group No.” or “GRP.” In the modern era of fintech, this number is also prominently displayed in employee benefit portals and mobile banking apps.

Financial planners recommend that individuals keep a digital copy of these identifiers. In the event of a medical emergency or a financial dispute, having the group number ready allows for immediate verification of benefits. Without it, providers may default to “out-of-network” or “uninsured” pricing, which can lead to significant financial strain and the headache of seeking reimbursements later.

Using Group Numbers for Tax Deductions and Reimbursements

In many jurisdictions, the costs associated with plans identified by a group number are tax-deductible or paid with pre-tax dollars. For example, in the United States, premiums paid toward a group health plan are often deducted from an employee’s gross pay before taxes are calculated.

When filing taxes or managing a Health Savings Account (HSA) or Flexible Spending Account (FSA), the group number serves as a reference point for the legitimacy of the expense. It proves that the expenditure was part of a qualified employer-sponsored plan, ensuring that the taxpayer remains compliant with government regulations while maximizing their tax savings.

Group Numbers in Business Finance: Managing Large-Scale Benefits

While individuals see the group number as a way to access services, for business owners and financial officers, it is a vital tool for organizational accounting and financial health.

Consolidated Billing and Administrative Efficiency

Imagine if a company with 10,000 employees had to manage 10,000 individual insurance contracts. The administrative overhead would be a financial disaster. Group numbers allow for “consolidated billing.” The insurance provider sends one massive invoice to the company, indexed by the group number, and the company’s payroll department handles the individual deductions. This efficiency reduces the “cost of doing business,” allowing the company to reallocate those funds toward growth, innovation, or higher wages.

Financial Security and Fraud Prevention

In the realm of corporate finance, the group number also serves as a layer of security. It ensures that only verified members of an organization are accessing the company’s funded benefits. By auditing usage under a specific group number, companies can identify patterns of overspending or potential fraud. For instance, if a group number for a small accounting firm shows a sudden spike in claims that don’t match the demographic of the employees, the company’s financial officers can trigger an investigation. This oversight protects the company’s bottom line and ensures the long-term sustainability of the benefits plan.

The Future of Group Identification in a Digital Economy

As we move further into the digital age, the way we interact with group numbers is evolving. We are seeing a shift from physical cards to integrated financial ecosystems where these numbers are embedded in “Smart Wallets.”

Blockchain and Secure Identification

There is an increasing movement toward using blockchain technology to manage group financial identifiers. Instead of a static number printed on a piece of plastic, a “group number” could become a secure, encrypted token on a ledger. This would allow for instantaneous verification of benefits without exposing the individual’s sensitive personal data, further enhancing the security of personal finance.

Integration with Personal Finance Apps

Modern personal finance apps (like Mint, YNAB, or specialized benefit trackers) are beginning to use group numbers to help users see their “total wealth” more accurately. By pulling data associated with a group number, these apps can show a user their remaining deductible, their out-of-pocket maximums, and their employer’s contributions in real-time. This level of transparency is revolutionizing how individuals plan for their financial futures, turning a once-obscure number into a dynamic tool for wealth management.

Conclusion: The Power of Financial Literacy

What is a group number? It is far more than an administrative necessity. It is a symbol of the collective’s power in a market-driven economy. It is the key that unlocks negotiated savings, the framework that enables risk pooling, and the tool that allows corporations to provide a safety net for their workforce.

For the savvy individual, the group number is a reminder that they are part of a larger financial structure. By understanding how this number functions, where to find it, and how it impacts their taxes and out-of-pocket costs, they can navigate the world of finance with greater confidence. In an era where every cent counts, mastering the small details—like a group number—can lead to significant long-term financial stability. Knowledge is the greatest asset in any portfolio, and understanding the “why” behind the digits on your card is a perfect place to start.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.