The intersection of mortality and finance is a subject many prefer to avoid, yet it is one of the most critical aspects of personal financial planning. When a person passes away, they leave behind more than just memories and personal belongings; they often leave behind a complex web of financial obligations. A common fear among grieving family members is the sudden burden of a loved one’s unpaid credit cards, mortgages, or medical bills.

Understanding what happens to debt after death is essential for protecting your inheritance, managing an estate, and ensuring financial peace of mind. In the world of personal finance, the general rule is that debt does not simply vanish, but neither is it automatically transferred to the next of kin. Instead, the responsibility falls upon the “estate” of the deceased.

Understanding the Probate Process and the Role of the Estate

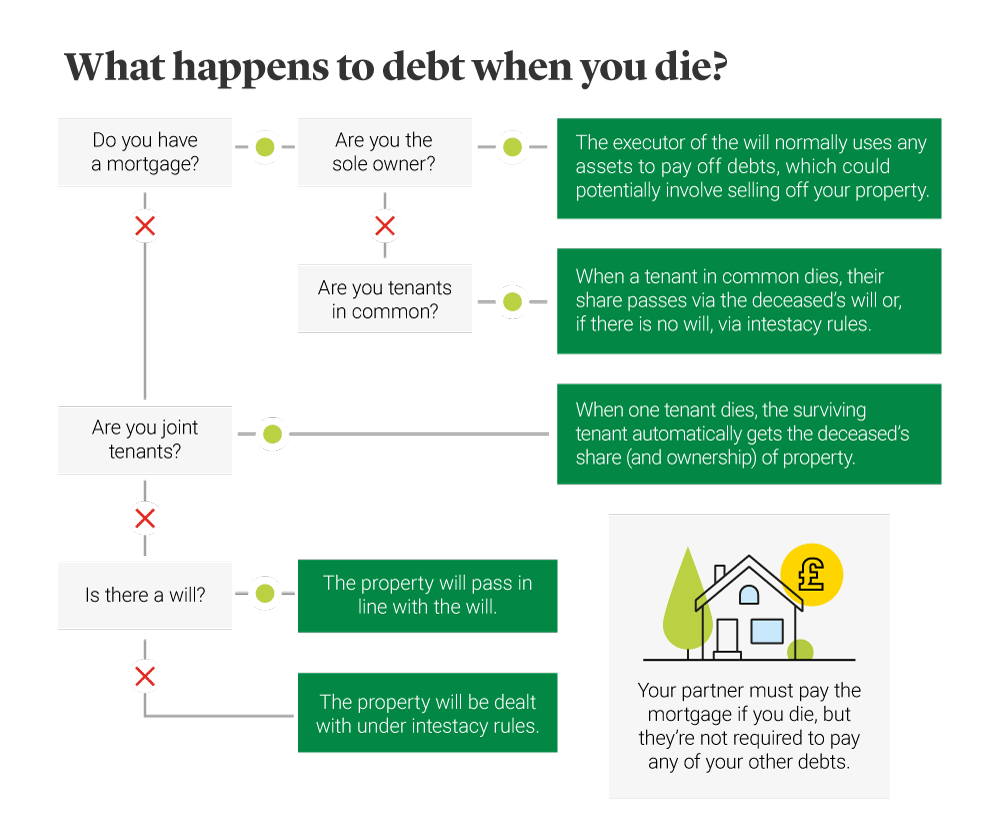

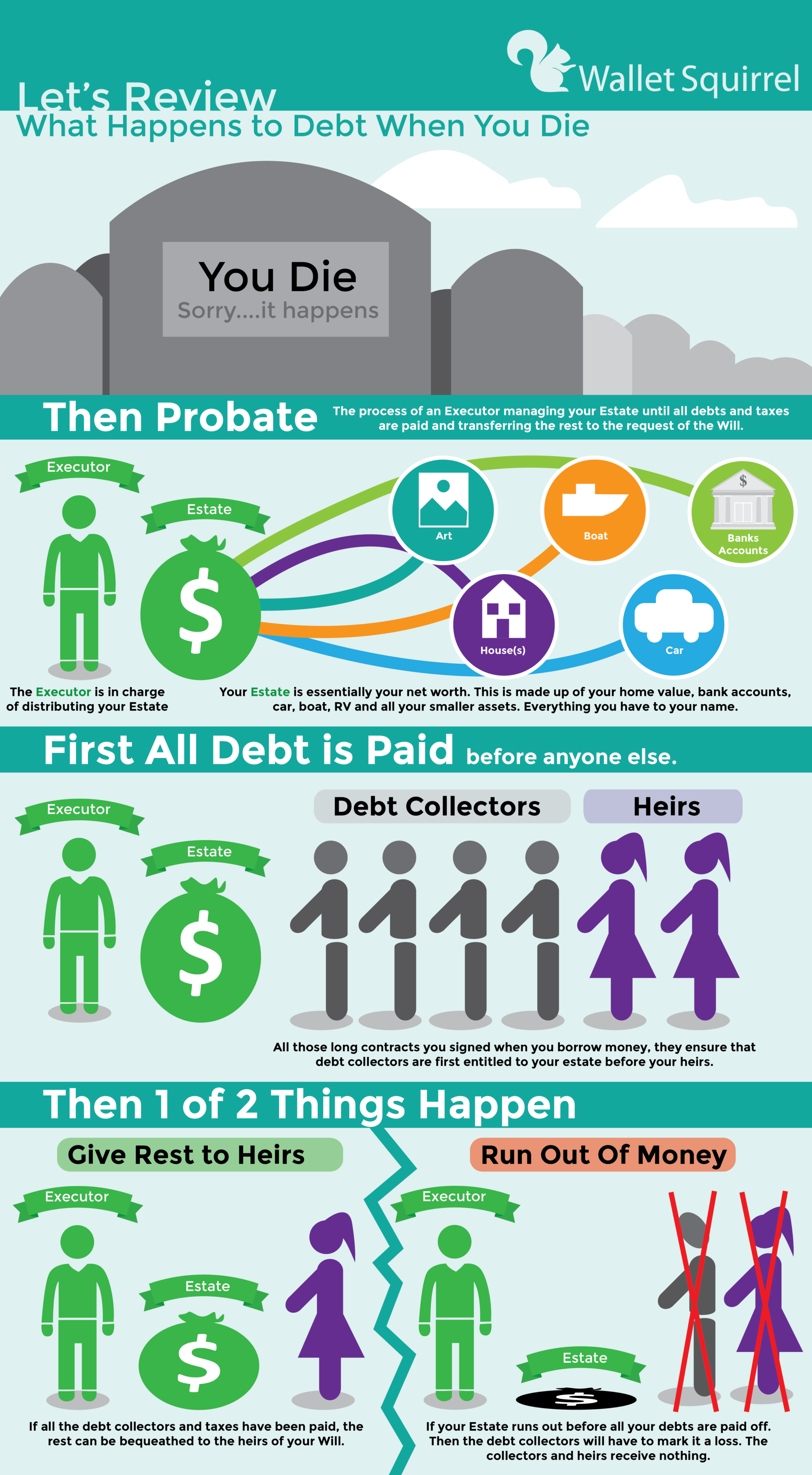

When an individual dies, all their assets—including bank accounts, real estate, investments, and personal property—collectively become known as the “estate.” This estate is a legal entity responsible for settling the deceased person’s affairs under the supervision of a probate court.

Defining the Estate and Probate

Probate is the court-supervised legal process of validating a will (if one exists), identifying assets, and ensuring that all debts and taxes are paid before any remaining inheritance is distributed to beneficiaries. If there is no will, the person is said to have died “intestate,” and the court follows state laws to determine how assets are handled. The estate acts as a buffer; it is the primary source of funds used to satisfy creditors.

The Role of the Executor or Administrator

If a will exists, it typically names an executor. If there is no will, the court appoints an administrator. This individual has a fiduciary duty to manage the estate’s finances. One of their first tasks is to notify creditors of the death. Once notified, creditors have a specific window of time to file claims against the estate for the money they are owed. The executor must then verify these claims and pay them using the estate’s liquid assets.

The Priority of Claims: Who Gets Paid First?

In the world of business finance and estate law, not all debts are created equal. Most jurisdictions follow a specific hierarchy for payments. Generally, the order of operations is as follows:

- Funeral and Administrative Expenses: Costs for the burial and legal fees for the probate process are paid first.

- Taxes: Federal and state taxes, including the final income tax return of the deceased, must be settled.

- Secured Debts: Debts backed by collateral, such as mortgages.

- Unsecured Debts: Credit cards, personal loans, and medical bills are usually last in line.

If the estate runs out of money before reaching the bottom of the list, the remaining creditors typically have to write off the loss. This is known as an “insolvent estate.”

Different Types of Debt and How They Are Handled

How debt is treated depends largely on whether it is secured or unsecured and the specific terms of the loan agreement.

Secured vs. Unsecured Debt

Secured debts are tied to a specific asset. If the debt isn’t paid, the creditor can seize the asset. Unsecured debts, conversely, are granted based on the borrower’s creditworthiness and do not have collateral. In the event of death, secured creditors have a much stronger position than unsecured ones.

Mortgages and Home Equity Loans

A mortgage is the most common form of secured debt. When a homeowner dies, the debt remains attached to the property. If a co-owner or an inheritor wishes to keep the house, they must continue making the payments. Under the Garn-St. Germain Depository Institutions Act, lenders generally cannot trigger a “due on sale” clause just because the owner died and the property passed to a relative. However, if no one can afford the payments and the estate cannot cover the balance, the lender may foreclose on the home to recoup the loan.

Credit Card Balances and Personal Loans

Credit card debt is unsecured. When a person dies, the credit card company becomes a general creditor of the estate. They must file a claim with the probate court to get paid. If the estate has enough cash or assets that can be sold, the credit card debt is settled. If the estate is insolvent, the credit card company is usually out of luck. Family members are not responsible for these balances unless they were joint account holders.

Student Loans: Federal vs. Private

The treatment of student loans varies significantly. Federal student loans are the most “forgiving” in this regard; they are legally required to be discharged upon the death of the borrower (or the student for whom a Parent PLUS loan was taken). Private student loans, however, are governed by the contract terms. Some private lenders offer death discharges, but others may attempt to collect from the estate or hold a co-signer responsible.

When Are Heirs Responsible for a Deceased Relative’s Debt?

One of the most persistent myths in personal finance is that children inherit their parents’ debt. While this is generally false, there are three specific scenarios where survivors may find themselves legally obligated to pay.

Co-signers and Joint Account Holders

There is a critical distinction between an “authorized user” and a “joint account holder.” An authorized user is not responsible for the debt. However, a joint account holder or a co-signer shared the legal responsibility for the debt while the person was alive, and that responsibility continues after death. If you co-signed a car loan for a relative who passes away, the lender will look to you for the remaining payments.

Community Property States

In the United States, most states follow “common law,” where debt belongs only to the person who incurred it. However, in “community property” states (such as California, Texas, and Arizona), most debts incurred during a marriage are considered the joint responsibility of both spouses. In these jurisdictions, a surviving spouse might be held liable for a deceased partner’s debt, even if their name wasn’t on the original contract.

Filial Responsibility Laws

Though rarely enforced, nearly 30 states have “filial responsibility” laws. These statutes can, in theory, require adult children to pay for their deceased parents’ unpaid medical or long-term care bills if the estate cannot. While modern insurance and Medicaid have made these laws largely obsolete, they remain on the books in many places and can occasionally be leveraged by healthcare providers.

Protecting Assets and Planning for the Future

Effective financial planning can prevent a person’s debt from consuming their entire legacy. By utilizing specific financial tools, individuals can ensure that their wealth passes directly to their heirs, bypassing the reach of creditors.

Life Insurance as a Debt Shield

Life insurance is one of the most powerful tools in a financial portfolio. In most cases, life insurance proceeds are paid directly to named beneficiaries and do not become part of the probate estate. This means the money is generally protected from the deceased’s creditors. This liquidity can provide heirs with the funds needed to pay off a mortgage or simply maintain their standard of living without the shadow of the deceased’s debts.

Setting Up Trusts to Bypass Probate

A living trust is another effective strategy. Assets placed in a properly structured trust are owned by the trust, not the individual. Upon death, these assets pass to beneficiaries outside of the probate process. Since they don’t pass through probate, they are often shielded from certain types of creditor claims, though laws vary by state regarding “spendthrift” clauses and asset protection.

The Importance of a Clear Will

While a will does not prevent debt from being paid, it brings order to the chaos. A clear will allows you to designate which assets should be sold first to cover liabilities, potentially saving sentimental items or the family home from being liquidated by an executor trying to satisfy creditors.

Dealing with Debt Collectors and Legal Rights

The period following a loss is emotionally taxing, and it can be made worse by aggressive debt collectors. It is vital to know your rights under federal law to prevent financial harassment.

The Fair Debt Collection Practices Act (FDCPA)

The FDCPA protects survivors from predatory collection tactics. Debt collectors are allowed to contact the deceased person’s spouse, executor, or administrator to discuss the debt. However, they are generally prohibited from contacting other family members. More importantly, they cannot mislead you into believing you are personally responsible for a debt that you do not legally owe.

Identifying Scams and False Claims

Unfortunately, some unscrupulous collectors and scammers monitor obituary notices to target grieving families. They may call and demand immediate payment for a “forgotten loan” or an “overdue bill.” Always demand a “validation notice”—a written statement providing the amount of the debt and the name of the creditor. Never make a payment over the phone until you have verified the debt with the estate’s executor or a legal professional.

Conclusion

Debt does not always die with the debtor, but it rarely migrates to the living. By understanding the mechanisms of the estate, the hierarchy of creditor claims, and the nuances of different loan types, individuals can better navigate the financial complexities of loss. Whether you are planning your own estate or managing the affairs of a loved one, knowledge is the best defense against financial instability. In the realm of personal finance, being proactive with life insurance, trusts, and clear documentation ensures that your final legacy is one of security, not a burden of debt.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.