For many Americans, the arrival of a small, red, white, and blue paper card in the mail signals a significant milestone: the transition into a new phase of financial and physical well-being. While the question “what does the medicare card look like” may seem like a simple inquiry into aesthetics, the answer carries profound implications for personal finance, identity security, and retirement planning.

In the landscape of modern personal finance, the Medicare card is more than just an insurance ID; it is a gateway to one of the most substantial financial benefits provided by the federal government. Understanding its design, the information it contains, and the security features it employs is essential for any individual looking to safeguard their financial future.

1. Decoding the Design: The Physical Identity of Federal Healthcare

The Medicare card has undergone significant transformations over the decades, evolving from a simple identification tool to a high-security document designed to protect the cardholder’s financial health. Today, the card is characterized by its patriotic color scheme and its minimalist, functional layout.

The Standardized Layout

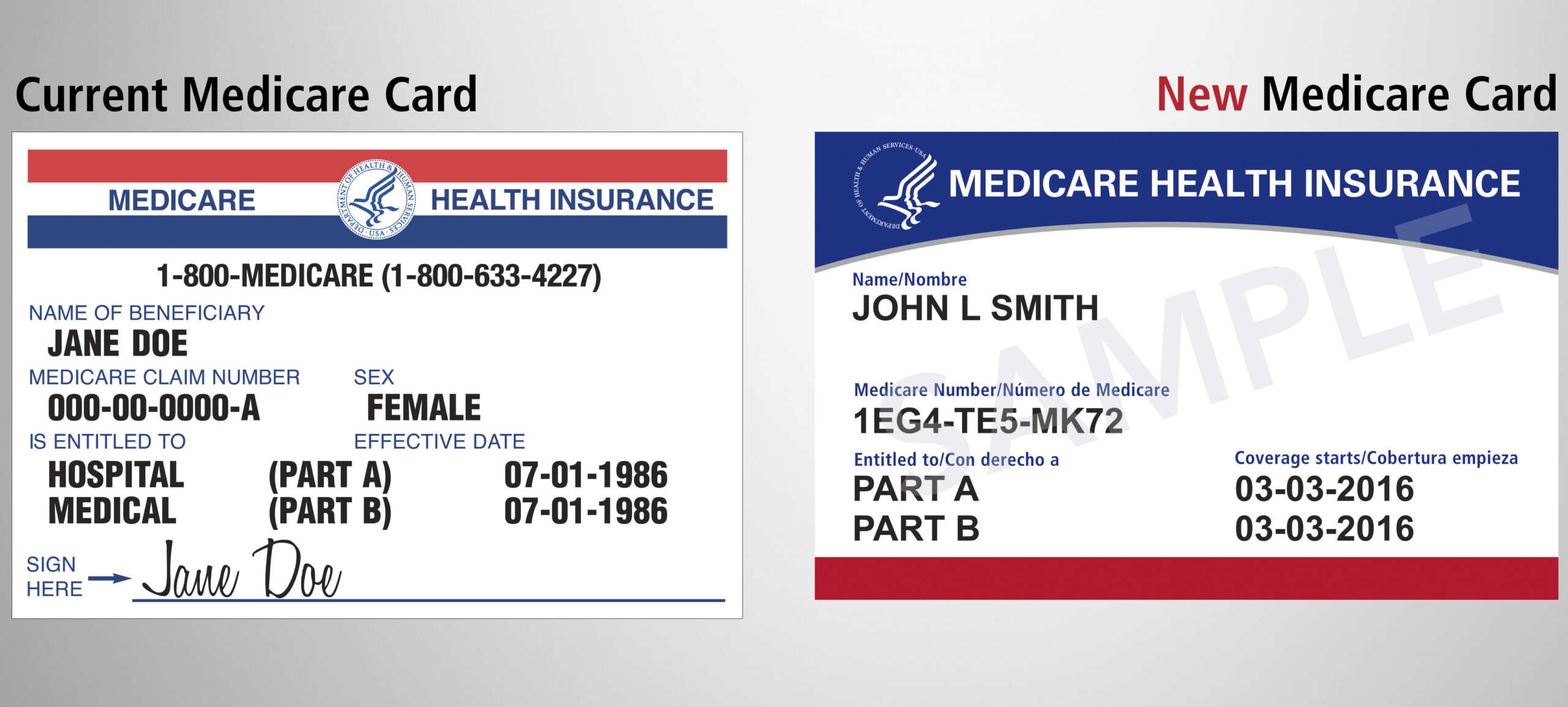

The current Medicare card is printed on high-quality paper and features a distinct red and blue header. Unlike the credit cards or driver’s licenses that many are used to, the Medicare card is intentionally thin to fit easily into a wallet. On the front of the card, you will find your name, your unique Medicare Number, and the specific coverage you are entitled to (Part A, Part B, or both), along with the dates those coverages became effective.

The Shift from Social Security Numbers to MBI

Perhaps the most critical “look” of the modern Medicare card is what is missing. Prior to 2018, Medicare cards prominently displayed the beneficiary’s Social Security Number (SSN). This created a massive financial risk, as a lost wallet could lead to instant identity theft and total financial compromise. The modern card now features a Medicare Beneficiary Identifier (MBI). This is a 11-character string of numbers and uppercase letters that is unique to you but contains no hidden personal information. From a financial security perspective, this shift was a monumental upgrade in protecting senior citizens’ credit scores and bank accounts.

Distinguishing Between Original Medicare and Advantage Plans

It is important to note that if you choose a Medicare Advantage Plan (Part C), your primary card for daily use will look different. Private insurers like UnitedHealthcare, Humana, or Aetna issue their own branded cards. However, even if you use an Advantage plan, you must keep your original red, white, and blue Medicare card in a safe place. It remains the foundational proof of your eligibility for federal benefits and is required if you ever decide to switch back to Original Medicare during an enrollment period.

2. The Financial Value of the Card: Accessing Your Benefits

When you look at your Medicare card, you are looking at a document that represents hundreds of thousands of dollars in potential healthcare coverage. In the context of personal finance, your Medicare card is an asset that must be managed with the same scrutiny as a 401(k) or an investment portfolio.

Understanding Part A and Part B Coverage Dates

The “Effective Date” listed on the front of your card is one of the most important numbers in your financial life. Part A (Hospital Insurance) typically carries no premium for those who have worked 10 years or more in the U.S. Part B (Medical Insurance), however, requires a monthly premium. Knowing exactly when these coverages begin allows you to coordinate with your previous employer’s insurance or COBRA, preventing “double-paying” for coverage or, worse, experiencing a gap in coverage that could lead to devastating out-of-pocket medical bills.

Avoiding Late Enrollment Penalties

The Medicare card serves as a reminder of the “Initial Enrollment Period.” From a money management perspective, missing your enrollment window is a permanent financial mistake. If you do not sign up for Part B when you are first eligible (and do not have “creditable coverage” from an employer), you may face a lifetime late enrollment penalty. This penalty is added to your monthly premium for as long as you have Medicare, effectively acting as a permanent tax on your retirement income.

Integration with Supplemental Insurance (Medigap)

For those on Original Medicare, the card is the first step, but it rarely covers 100% of costs. Most beneficiaries use their Medicare card in conjunction with a Medigap (Medicare Supplement) policy. When a provider sees your red, white, and blue card, they know they are billing the federal government for the majority of the cost, while your supplemental policy handles the remaining 20% coinsurance. Understanding this synergy is vital for budgeting your monthly healthcare “burn rate” during retirement.

3. Protecting Your Financial Health: Fraud Prevention and Security

The Medicare card is a frequent target for scammers and fraudsters. Because it represents a direct line to government funds, the visual familiarity of the card is often exploited in “spoofing” attacks. Protecting the physical card and the information on it is a core tenet of modern financial literacy.

Identifying Medicare Scams

Fraudsters often call seniors claiming that “Medicare is issuing a new plastic card” or a “card with a chip,” and they request a processing fee or the verification of a Social Security Number. It is vital to know that the official Medicare card is paper, not plastic, and the government will never call you to ask for your MBI. Any request for payment to “activate” a Medicare card is a financial red flag. Recognizing the legitimate look and feel of the card allows you to immediately identify and discard these fraudulent attempts to access your finances.

The Impact of Medical Identity Theft

If a thief gains access to your Medicare Number, they can bill the government for services never rendered or equipment never received. While the government loses money in this scenario, the beneficiary faces a significant financial headache: their “Maximum Out-of-Pocket” limits may be reached, or they may find their medical records corrupted with incorrect information, leading to denials of legitimate future claims. Treating your Medicare card with the same level of security as a debit card is essential for maintaining your financial integrity.

Safeguarding the Physical Card

Because the card is made of paper, many people wonder if they should laminate it. Financially speaking, this is a gray area; while it protects the card from wear and tear, lamination can sometimes interfere with the security watermarks or make it difficult for providers to scan. Instead, many financial advisors recommend using a high-quality plastic sleeve. If your card is lost or the information is compromised, you should immediately log into MyMedicare.gov or call 1-800-MEDICARE to request a replacement and a new MBI, effectively “freezing” the old account much like you would a compromised credit card.

4. Integrating Medicare into Your Long-Term Retirement Strategy

The ultimate goal of understanding your Medicare card is to ensure it fits seamlessly into your broader financial plan. Healthcare is often the largest expense for retirees, and the Medicare card is the primary tool used to mitigate those costs.

Budgeting for Premiums and Deductibles

The card signifies that you are now part of a system with predictable, but non-zero, costs. As of 2024, the standard Part B premium is a significant monthly expense that is usually deducted directly from Social Security checks. High-income earners must also account for the Income Related Monthly Adjustment Amount (IRMAA), which can triple or quadruple the cost of the card’s “maintenance.” Factoring these costs into your monthly cash flow analysis is crucial for a sustainable retirement.

The Role of Digital Financial Tools

In the modern era, the physical card is supported by a robust digital infrastructure. By creating an account on the official Medicare website, you can track your claims in real-time. This is an excellent way to audit your healthcare spending and ensure that providers are billing correctly. In the world of personal finance, “tracking every dollar” is a mantra; your Medicare portal allows you to do exactly that with your healthcare expenditures, providing a level of transparency that was impossible a generation ago.

Planning for the “Donut Hole” and Prescription Costs

While the standard Medicare card covers Parts A and B, your financial strategy must also include Part D (Prescription Drugs). Although Part D isn’t usually listed on the red, white, and blue card, your enrollment in it is linked to your MBI. Understanding how the “Donut Hole” or coverage gap affects your out-of-pocket costs for medications is essential for preventing a sudden “wealth shock” later in the year when drug costs might spike.

Conclusion

The Medicare card is far more than a simple piece of identification; it is a foundational pillar of an American’s financial security during their senior years. By understanding what the card looks like—and more importantly, what its features represent—you can protect yourself from identity theft, avoid permanent financial penalties, and more accurately budget for the years ahead.

Treat your Medicare card as you would a high-limit credit card or a deed to a property. It represents your right to healthcare and your protection against the catastrophic costs of illness. In the intersection of health and money, the red, white, and blue card is your most valuable asset. Keep it safe, understand its power, and use it as the centerpiece of a well-orchestrated financial retirement plan.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.