In the complex ecosystem of personal finance, few terms carry as much weight or cause as much confusion as the “charge-off.” For many consumers, seeing this status on a credit report feels like a financial death sentence or, conversely, a confusing sign that a debt has simply vanished. Neither is strictly true. A charge-off is a pivotal moment in the lifecycle of a debt, representing a transition from a standard lending agreement to a serious delinquency that carries long-term implications for your creditworthiness and financial future.

Understanding what it means to charge off an account requires looking past the jargon to the accounting realities of the banking industry. It is a declaration by a creditor that a debt is unlikely to be collected, but it is far from a cancellation of the obligation. To navigate this situation effectively, one must understand the timeline, the impact on credit scores, and the legal avenues available for resolution.

The Mechanics of a Charge-Off: When and Why it Happens

A charge-off is primarily an accounting entry. From a regulatory perspective, banks and lenders cannot carry non-performing assets on their books indefinitely. When a borrower stops making payments, the lender eventually reaches a point where they must acknowledge that the debt is a “loss” for tax and reporting purposes.

The Standard Timeline for Delinquency

Most creditors do not charge off an account after one or two missed payments. Instead, there is a standardized window of delinquency. For most revolving credit accounts, such as credit cards, the charge-off typically occurs after 180 days (six months) of non-payment. For installment loans, such as personal loans or auto loans, the window is often shorter, typically 120 days.

During this period, the account moves through stages of “past due” status—30, 60, 90, and 150 days late. Each stage triggers internal collection efforts, including phone calls, emails, and letters. If the consumer fails to bring the account current or enter a hardship program by the end of the designated window, the lender “charges off” the balance.

The Creditor’s Perspective and Accounting Shift

When a lender charges off an account, they are essentially moving the debt from the “assets” column of their balance sheet to the “loss” column. This allows the institution to reduce its tax liability by claiming the unpaid debt as a business loss. However, it is a common misconception that this “loss” means the borrower is no longer responsible for the money.

The legal obligation to pay remains. The charge-off merely changes how the lender views the debt internally. In many cases, the lender will then sell the debt to a third-party collection agency for pennies on the dollar or assign it to an internal recovery department to continue collection efforts under a different strategy.

The Impact on Your Financial Health and Credit Profile

The consequences of a charge-off are significant and multifaceted. It is considered one of the most severe “derogatory marks” a consumer can have on their credit report, second only to bankruptcy or a foreclosure.

Credit Score Consequences

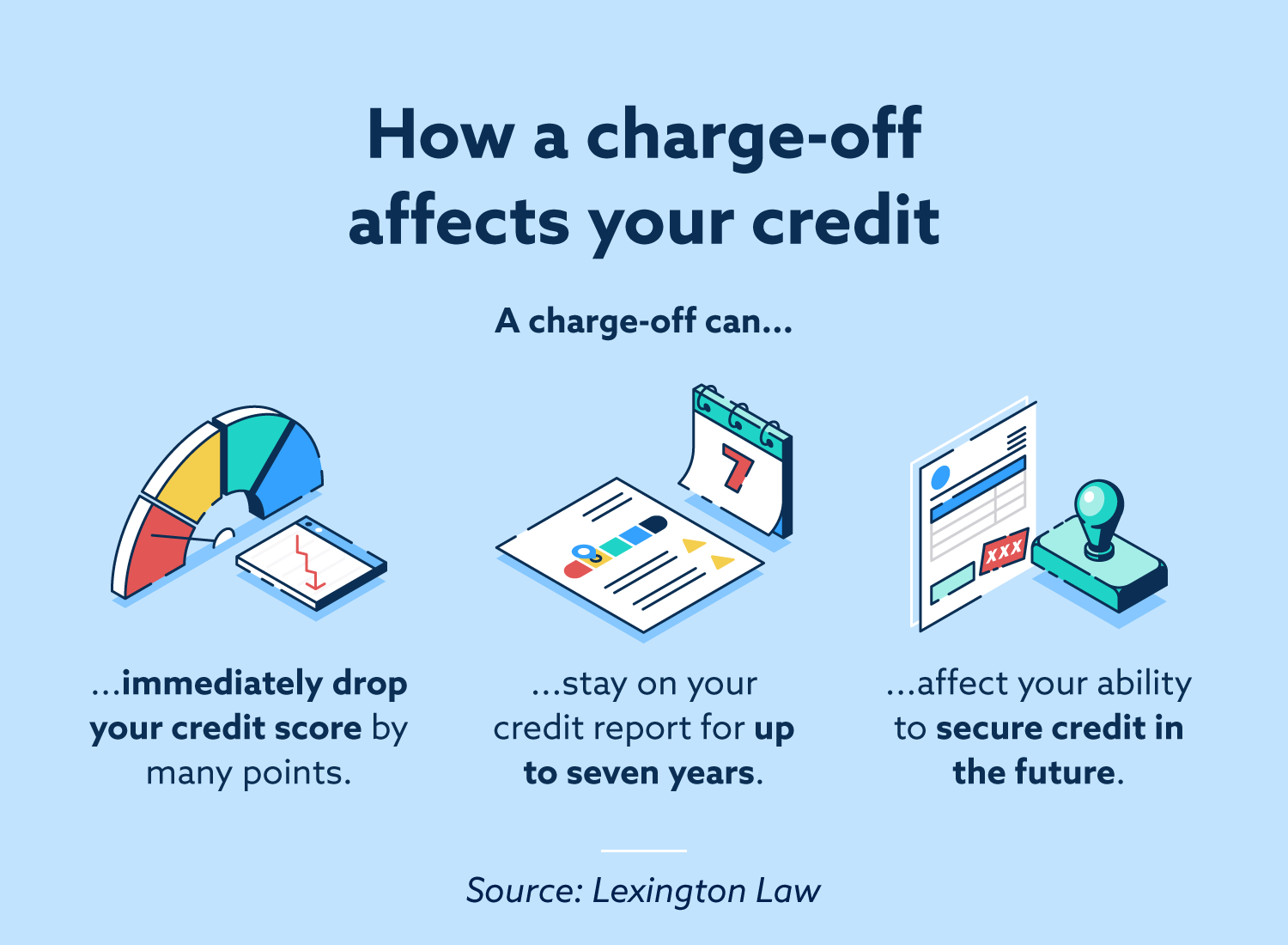

A charge-off acts as a major red flag to future lenders. Because it indicates that a previous creditor was unable to collect a debt despite months of trying, it suggests a high level of risk. Upon the reporting of a charge-off, a consumer’s FICO or VantageScore can drop by 100 points or more, depending on their starting score.

Furthermore, the impact is not static. While the initial drop is the most dramatic, the charge-off remains on a credit report for seven years plus 180 days from the “Date of First Delinquency”—the date of the first missed payment that led to the charge-off status. Even as the score begins to recover over time, the presence of the “Charged Off” notation can lead to automatic denials for premium credit cards, mortgages, or competitive auto loan rates.

Future Borrowing and the “Cost of Credit”

Beyond the score itself, a charge-off changes the “cost of credit” for the consumer. If you are able to secure a loan with a charge-off on your record, you will likely be relegated to “subprime” lenders who charge significantly higher interest rates and administrative fees. Over the life of a five-year auto loan or a thirty-year mortgage, the presence of a charge-off on your history could literally cost you tens of thousands of dollars in additional interest payments.

In some sectors, such as the rental market or employment in the financial services industry, a charge-off can also serve as a barrier to entry. Landlords and hiring managers often view a charge-off as a sign of financial instability or a lack of personal responsibility.

Resolving a Charged-Off Account: Strategy and Negotiation

If you find yourself with a charged-off account, the worst course of action is to ignore it. While the damage to your credit score has already occurred, the status of the charge-off—whether it is “Unpaid,” “Paid,” or “Settled”—matters immensely to future lenders and your overall financial peace of mind.

Paying in Full vs. Settling for Less

There are two primary ways to resolve a charge-off. The first is to pay the full balance. This changes the status on your credit report to “Paid Charge-Off.” While this does not remove the negative mark, it looks significantly better to future lenders because it shows you eventually fulfilled your obligation.

The second option is a “settlement.” Because the debt has been written off, many creditors (or the collection agencies that bought the debt) are willing to accept a lump sum that is significantly lower than the original balance—sometimes as low as 30% to 50% of what is owed. If you settle, the report will reflect “Settled Charge-Off” or “Paid for less than full balance.” This is generally better than an unpaid charge-off, though some lenders view it slightly less favorably than a full payment.

The “Pay for Delete” Negotiation

A more advanced strategy used by some consumers is the “Pay for Delete” agreement. In this scenario, the consumer offers to pay the debt (either in full or a settled amount) on the condition that the creditor removes the entire account from the credit report.

While this is a highly desirable outcome, it is difficult to achieve. Most major banks have internal policies against “Pay for Delete” because they are under contract with credit bureaus to report accurate information. However, smaller collection agencies are often more flexible. If you attempt this, it is vital to get the agreement in writing before sending any money. Without a written contract, the creditor may take your money and leave the derogatory mark on your report.

Legal Realities and Long-term Recovery

Navigating a charge-off also requires an understanding of the legal framework surrounding debt collection and the statutes of limitations that govern how long a creditor can legally sue you for a balance.

Third-Party Debt Collectors and the FDCPA

Once an account is charged off, it is frequently sold to a “debt buyer.” These companies specialize in purchasing large portfolios of delinquent debt and using aggressive tactics to recover funds. Consumers should be aware of their rights under the Fair Debt Collection Practices Act (FDCPA), which prohibits collectors from using deceptive, unfair, or abusive practices.

If a debt buyer contacts you regarding a charge-off, you have the right to “debt validation.” You can demand that the collector provide proof that the debt is yours, that they have the legal right to collect it, and that the amount is accurate. This is an essential step, as debts are often sold with incomplete or inaccurate documentation.

Statutes of Limitations and the “Zombie Debt” Phenomenon

Every state has a statute of limitations on debt, which is the time limit a creditor has to use the court system to force you to pay. This typically ranges from three to ten years. Once the statute of limitations has expired, the debt is considered “time-barred.”

However, “time-barred” does not mean the debt is gone; it just means you have a legal defense if you are sued. A dangerous trap for consumers is “re-aging” the debt. In many jurisdictions, making even a small payment on a charged-off account can “reset” the statute of limitations clock, giving the creditor a fresh window of time to sue you. Before making a payment on an old charge-off, it is crucial to research your state’s laws or consult with a legal professional.

Rebuilding After a Charge-Off

Recovering from a charge-off is a marathon, not a sprint. The strategy for recovery involves two parallel paths: resolving the old debt and building new, positive credit history. Once the charge-off is resolved (paid or settled), you should focus on adding “positive tradelines.” This might include opening a secured credit card or a credit-builder loan. By maintaining a perfect payment history on these new accounts, the weight of the old charge-off diminishes over time.

In the world of finance, time is the ultimate healer. As the charge-off ages, its impact on your score lessens. By the time it reaches its fifth or sixth year, a consumer who has managed their other finances perfectly may find that their score has rebounded significantly, proving that while a charge-off is a serious setback, it is not a permanent barrier to financial success.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.