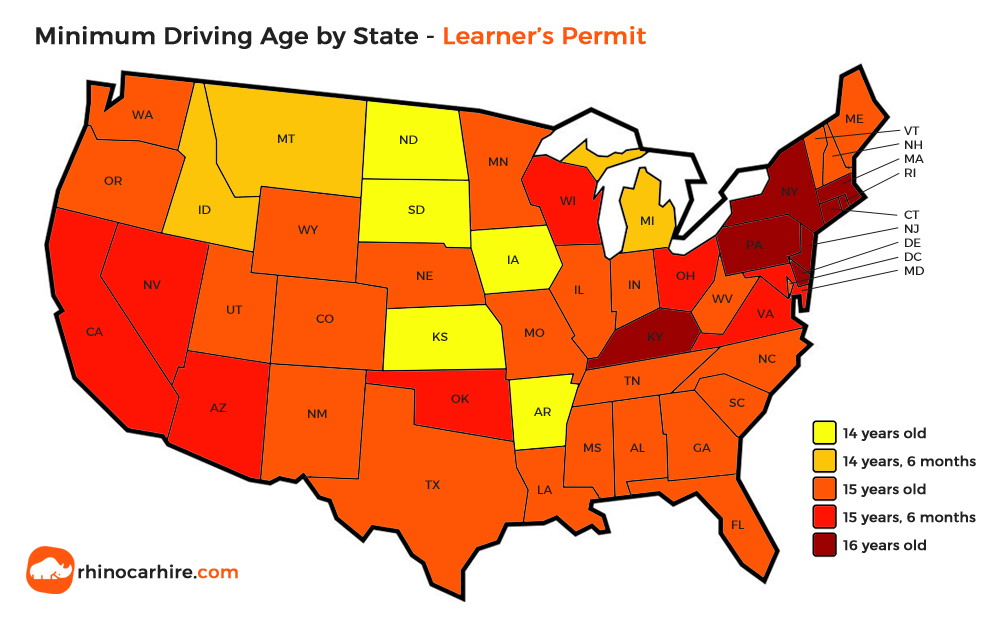

In the landscape of American personal finance and regional economics, few milestones carry as much weight—both literally and figuratively—as the acquisition of a driver’s license. While the cultural narrative often focuses on the freedom of the open road, the underlying reality is one of significant financial commitment, risk management, and economic participation. When we ask “what state has the youngest driving age,” the answer points us directly to South Dakota, where a learner’s permit can be obtained at just 14 years old. However, the financial implications of this policy extend far beyond the individual teenager.

From the perspective of personal finance, insurance markets, and labor economics, the states with the youngest driving ages represent a unique case study in how early mobility impacts a household’s bottom line and a state’s economic engine. This article explores the fiscal landscape of early licensing, the staggering costs of teen insurance, and the long-term wealth-building implications of starting the “car-ownership” journey earlier than the national average.

The Fiscal Landscape of Early Driving: Identifying the States and Their Economic Drivers

To understand the financial motivation behind early driving ages, one must look at the geography and economy of the states that allow it. South Dakota leads the nation, allowing 14-year-olds to obtain a permit and, after six months of clean driving, a restricted minor’s permit. Close followers include North Dakota, Montana, and Iowa. These are not coincidental selections; they are states with massive agricultural footprints and low population densities.

The Rural Economic Necessity

In these regions, early driving is less about leisure and more about economic survival. In a state like South Dakota, where the agricultural sector contributes billions to the GDP, a 14-year-old being able to drive a pickup truck between farm plots or to a local co-op isn’t just a convenience—it’s a labor necessity. By lowering the driving age, these states effectively expand their seasonal labor force without increasing the cost of adult labor. For the family farm, this represents a significant “internalized” cost saving, allowing younger family members to contribute to the business’s logistics.

Lowering the Barrier to Teen Employment

Beyond the farm, early licensing has a direct impact on the teen labor participation rate. In states where the driving age is 17 or 18, many teenagers are financially locked out of the workforce because they lack the means to reach a job site. In early-licensing states, 15-year-olds can hold steady part-time jobs in retail, hospitality, or local services. This early entry into the workforce allows for the beginning of personal savings, the introduction of taxable income at an earlier age, and the early development of financial literacy through earning and spending.

The Cost of Early Independence: Insurance Premiums and Risk Management

While the ability to work at 14 or 15 provides an income stream, it is often immediately met by one of the most significant “poverty traps” for young people: auto insurance. From a money management perspective, insuring a 14-to-16-year-old driver is one of the most expensive ventures a household can undertake.

Why Youngest Drivers Face the Highest Premiums

Insurance companies operate on actuarial data, and the data for the youngest drivers is clear: they represent the highest risk of collision and total-loss claims. In states with the youngest driving ages, premiums for a restricted permit holder can be astronomical. A family might see their annual premium increase by 50% to 100% simply by adding a 14-year-old to the policy.

The “Money” niche perspective here focuses on the “Risk vs. Reward” ratio. For many families in South Dakota or Montana, the cost of the insurance is viewed as a necessary business expense for the family’s economic output. However, for a suburban family, this is a discretionary expense that requires careful budgeting and an understanding of how liability limits affect personal net worth.

Strategic Financial Planning for Teen Auto Insurance

To mitigate these costs, savvy families utilize several financial tools and strategies:

- Good Student Discounts: Most major insurers offer a 10% to 15% discount for students maintaining a B average or higher. This creates a financial incentive for academic performance.

- The “Beater” Strategy: From a capital expenditure standpoint, many families opt to buy older, low-value vehicles for young drivers. By carrying only liability insurance and eschewing comprehensive or collision coverage on a vehicle worth less than $3,000, families can save thousands in annual premiums.

- Telematics and Monitoring: Many modern insurance products use “black box” technology to track driving habits. For a young driver, proving safe habits through data can lead to significant rate reductions, turning “behavior” into “currency.”

The Automotive Industry’s Financial Stake in Young Drivers

The states with the youngest driving ages also serve as unique micro-markets for the automotive industry. When 14 and 15-year-olds enter the market, they create a specific demand for used vehicles, maintenance services, and aftermarket products.

Used Car Market Trends in Early-Licensing States

In states like North Dakota and Iowa, the “starter car” market is exceptionally robust. There is a high velocity of transactions in the $5,000 to $10,000 range. This creates a local economic ripple effect: used car dealerships, independent mechanics, and parts retailers see steady demand driven by a demographic that is notoriously hard on vehicles. For an investor or business owner, these states offer a more consistent “entry-level” automotive market than states with higher licensing ages.

Maintenance and Depreciation: The Hidden Costs of Early Ownership

From a personal finance standpoint, the cost of the car is only the “sticker price.” The real financial impact lies in maintenance and depreciation. Young drivers are statistically less likely to perform preventative maintenance, leading to higher long-term repair costs. Furthermore, the high mileage often associated with rural driving in states like Montana leads to rapid depreciation. For a teenager trying to build wealth, a car is a “depreciating asset” that requires constant capital infusion. Understanding this early is a vital lesson in asset management—learning that a car is a tool for income generation, rather than a store of value.

Long-Term Wealth Building and the “Car-First” Mentality

Perhaps the most profound financial impact of living in a state with a young driving age is the early introduction to the “Car-First” lifestyle. In the United States, transportation is often the second-largest household expense after housing. When a person starts driving at 14, they are potentially adding 2-4 years of vehicle ownership costs to their lifetime total compared to someone in an urban center or a state with a higher driving age.

Opportunity Costs of Teen Car Ownership

If a 15-year-old in South Dakota spends $3,000 a year on insurance, gas, and maintenance, that is $3,000 that is not being invested in a Roth IRA or a college savings fund. Using the power of compound interest, that $3,000 invested at age 15 could potentially grow to over $50,000 by retirement (assuming a 7% return over 40+ years).

The “Money” lesson here is one of opportunity cost. While the driver’s license provides the means to earn money, the cost of that mobility can actually hinder long-term wealth building if not managed correctly. Families that succeed financially in these states often find ways to offset these costs, such as having the teenager pay a portion of the insurance to instill a sense of fiscal responsibility.

Building Credit and Financial Responsibility through Early Asset Management

On the positive side of the ledger, early driving can be a gateway to credit building. Many parents use the purchase of a teenager’s first car as an opportunity to co-sign a small loan. When managed correctly, this allows the young driver to begin building a credit history years before their peers in other states. A high credit score by age 21 can save a person tens of thousands of dollars in interest on future home loans and higher-tier credit products. In this sense, the “youngest driving age” is not just a legal statute; it is a head start in the American financial system, provided the risks are managed with professional-grade scrutiny.

Conclusion: The Bottom Line on Early Licensing

While the question “what state has the youngest driving age” has a simple geographical answer, the financial reality is incredibly complex. States like South Dakota, North Dakota, and Montana have created a system where early mobility fuels the local economy and provides teenagers with an early path to employment. However, this path is paved with high insurance premiums, significant maintenance costs, and the potential for long-term opportunity costs.

For the modern investor or parent, the key to navigating the youngest driving ages lies in strategic financial planning. By utilizing insurance discounts, understanding the used car market, and viewing a vehicle as a tool for income rather than a mere lifestyle choice, the “early start” provided by these states can be turned into a significant financial advantage. Ultimately, the driver’s license at 14 is more than a right of passage; it is the first major “business decision” a young person will ever make.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.