In the realm of personal finance, a credit card is often viewed as a simple tool for transactions. However, for those who wish to master their financial health, the credit card is a complex instrument governed by specific timelines. One of the most misunderstood yet critical components of this timeline is the closing date. While most consumers focus exclusively on the “due date” to avoid late fees, the closing date is the actual fulcrum upon which your credit score, interest charges, and cash flow management pivot.

Understanding when your next closing date occurs—and more importantly, what happens on that day—is essential for anyone looking to optimize their personal balance sheet and maintain a pristine credit profile.

1. Decoding the Credit Card Closing Date

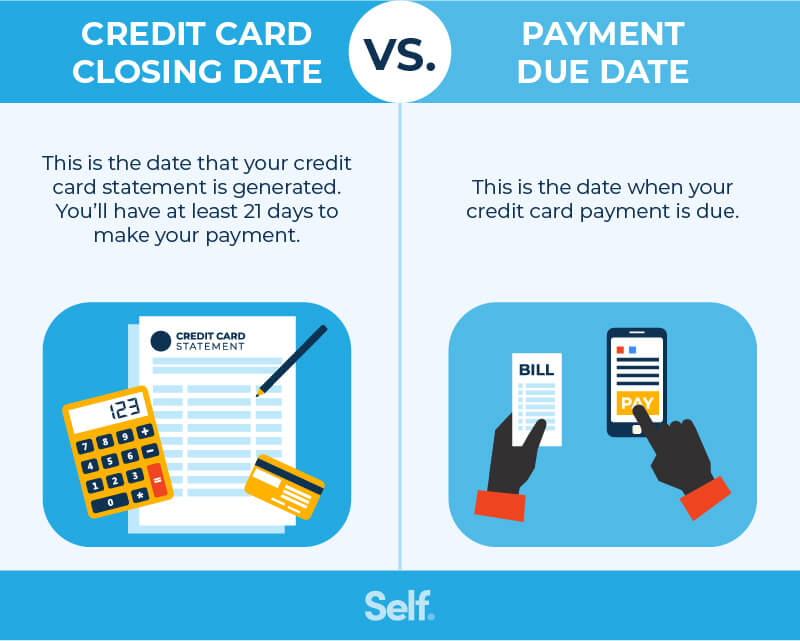

To navigate your finances effectively, you must first distinguish between the various dates listed on your financial statements. The closing date, often referred to as the “statement closing date” or “billing cycle end date,” marks the final day of a specific billing period.

Closing Date vs. Due Date: The Crucial Distinction

The most common mistake cardholders make is conflating the closing date with the payment due date. The closing date is the day the credit card issuer “wraps up” your activity for the month. On this day, they calculate your total balance, including new purchases, interest charges, and credits.

The due date, conversely, typically occurs 21 to 25 days after the closing date. This window is known as the grace period. While the due date tells you when you must pay to avoid penalties, the closing date determines what information is reported to credit bureaus.

How a Billing Cycle Actually Works

Most billing cycles last between 28 and 31 days. During this window, every swipe of your card adds to a running total. At the stroke of midnight on your closing date, the “snapshot” is taken. Any transaction that clears after this moment will fall into the next billing cycle. This means that a purchase made on the evening of your closing date could appear on your current statement, while a purchase made the following morning won’t be due for nearly two months.

2. Why Your Closing Date Is the Most Important Number for Your Credit Score

If you are focused on building or maintaining a high credit score, the closing date is arguably more important than the due date. This is due to how credit reporting works in the modern financial system.

Its Impact on Your Credit Score (Utilization Ratio)

The “Amounts Owed” category makes up 30% of your FICO credit score. The primary metric here is your credit utilization ratio—the amount of credit you are using compared to your total limits.

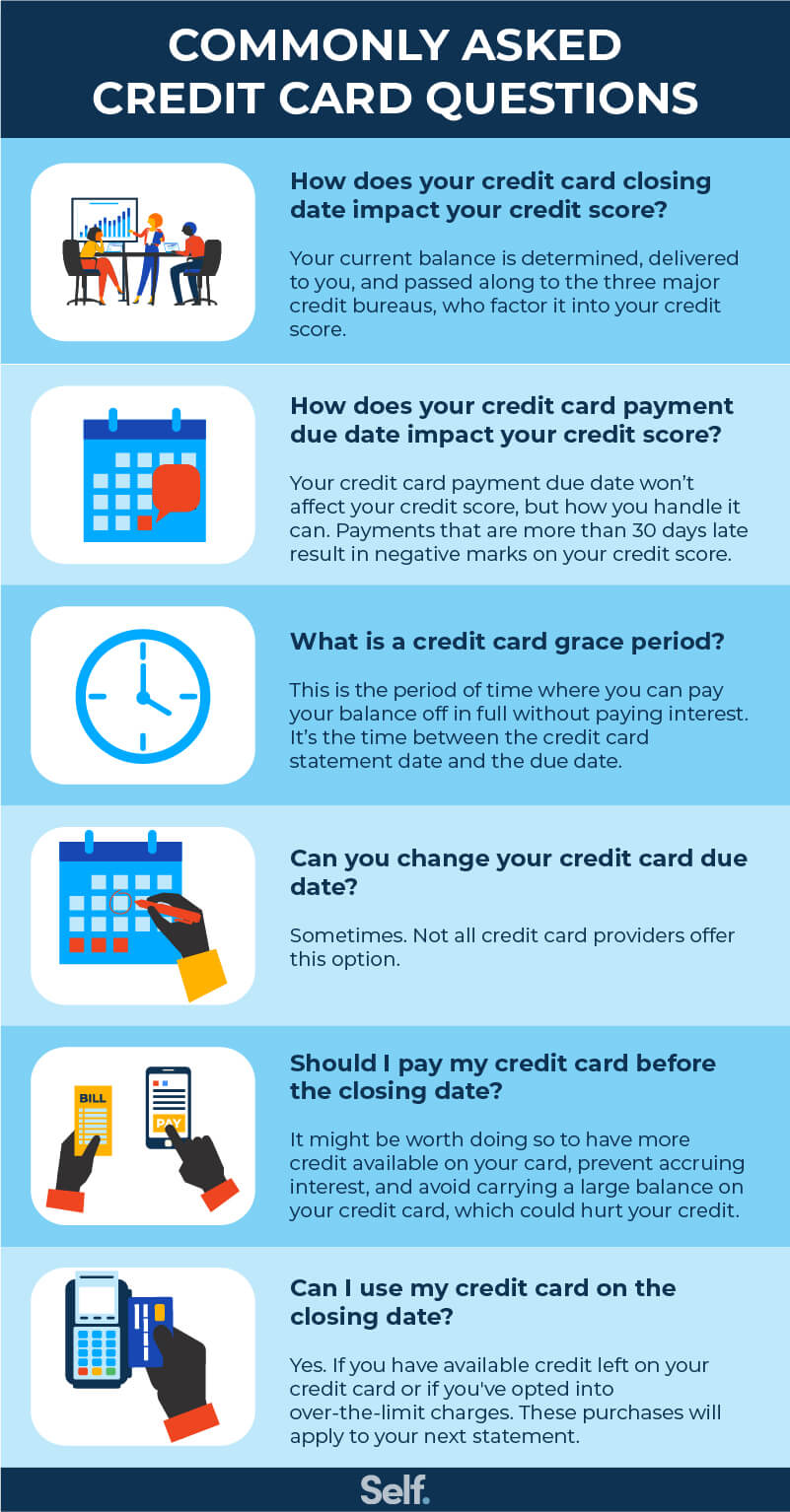

Crucially, most banks report your balance to the credit bureaus (Experian, Equifax, and TransUnion) exactly on your closing date. If you have a $10,000 limit and spend $5,000, and that $5,000 balance exists on your closing date, the bank reports a 50% utilization rate. Even if you pay that $5,000 in full by the due date three weeks later, the credit bureaus still see you as using 50% of your limit for that month. To maximize your score, you should aim to pay down your balance before the closing date so that a low balance (ideally under 10%) is reported.

Maximizing the Grace Period for Interest-Free Lending

For the disciplined spender, the closing date is the key to an interest-free loan. By understanding the cycle, you can time large purchases to occur right after a closing date. If your closing date is the 1st of the month and your due date is the 25th, a purchase made on the 2nd will not appear on a statement until the next month’s closing date, and won’t be due for payment until nearly 55 days later. This strategic use of the grace period allows you to keep your cash in high-yield savings accounts longer, earning interest for yourself rather than paying it to the bank.

3. How to Find and Manage Your Next Closing Date

Because closing dates can fluctuate slightly based on the number of days in a month (especially during February or months with 31 days), it is vital to know how to track this date in real-time.

Locating the Date via Digital Banking and Statements

The easiest way to find your next closing date is through your bank’s mobile app or online portal. Usually, under the “Account Details” or “Statement” section, you will see “Next Closing Date” or “Statement Ending.”

If you prefer paper or PDF statements, look at the top right or left corner of your last bill. It will list the “Billing Period.” For example, if it says “Jan 12 – Feb 11,” your closing date is the 11th of every month. However, be aware that if the 11th falls on a weekend or holiday, some issuers may move the date forward or backward by one business day.

Can You Change Your Closing Date?

Many people do not realize that the closing date is not set in stone. Most major issuers (such as Chase, Amex, or Citibank) allow you to request a change to your payment due date. Since the closing date is mathematically linked to the due date (usually 21–25 days prior), changing your due date will effectively shift your closing date.

This is a powerful tool for cash flow management. If you get paid on the 15th of the month, you might want your closing date to fall around the 20th, ensuring your payment is due shortly after your next paycheck arrives.

4. Strategic Spending: Using the Closing Date to Your Advantage

Sophisticated users of financial tools treat their credit card closing dates like a calendar for their expenses. By aligning your spending with these cycles, you can manipulate your liquid cash flow to your benefit.

The “Timing the Purchase” Strategy

If you have a significant upcoming expense—such as a new appliance or a vacation booking—timing is everything. If you make the purchase two days before your closing date, that bill will be due in roughly three weeks. If you wait until one day after your closing date, you effectively push the payment obligation an entire month into the future. This “float” is a legal and effective way to manage your monthly budget without incurring interest.

Managing Multiple Cards and Staggered Cycles

For those with multiple credit cards, there is a strategic advantage to having different closing dates for each. For example:

- Card A: Closing date on the 5th.

- Card B: Closing date on the 15th.

- Card C: Closing date on the 25th.

By staggering your dates, you ensure that no matter when an emergency or a large purchase arises, you always have a card that has just started a new billing cycle, giving you the maximum amount of time to pay off the balance before interest accrues.

5. Common Pitfalls and How to Avoid Them

While the closing date offers many benefits, it also presents traps for the unwary. Miscalculating this date can lead to unexpected interest charges or a sudden dip in your credit score.

The Trap of Minimum Payments Post-Closing

Many consumers believe that as long as they pay the “Minimum Amount Due” by the due date, they are managing their debt well. However, the interest is calculated based on the “Average Daily Balance” during the period ending on the closing date. If you do not pay the statement balance in full, the grace period for the next cycle is often revoked. This means new purchases begin accruing interest the very second you make them. Understanding your closing date helps you realize exactly when you must clear the deck to keep your “interest-free” status intact.

Residual Interest and the “Trailing” Balance

A common frustration occurs when a cardholder pays off their balance in full on the due date, only to see a small interest charge on the next statement. This is known as “residual” or “trailing” interest. It occurs because interest was accruing between the time the statement was closed and the time the payment was received. To avoid this, it is often best to pay the current balance (everything spent up to the present moment) rather than just the statement balance (what was owed on the last closing date).

The Importance of Monitoring

In the digital age, automation is your friend. Most financial institutions allow you to set up alerts not just for the due date, but for when a statement is closed. Setting a “Statement Available” alert serves as a monthly financial checkup. It prompts you to review your transactions for fraud and assess whether your spending for that cycle aligned with your budget.

Conclusion

The next closing date on your credit card is far more than just a bureaucratic deadline; it is a vital statistic in your personal financial profile. By mastering the timing of this date, you gain the ability to influence your credit score at will, extend your cash flow through the strategic use of the grace period, and avoid the compounding trap of high-interest debt.

In a world where financial literacy is the ultimate leverage, knowing your closing date is a simple yet profound step toward total financial control. Take a moment today to log into your accounts, identify your upcoming closing dates, and begin treating them as the strategic markers they are.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.