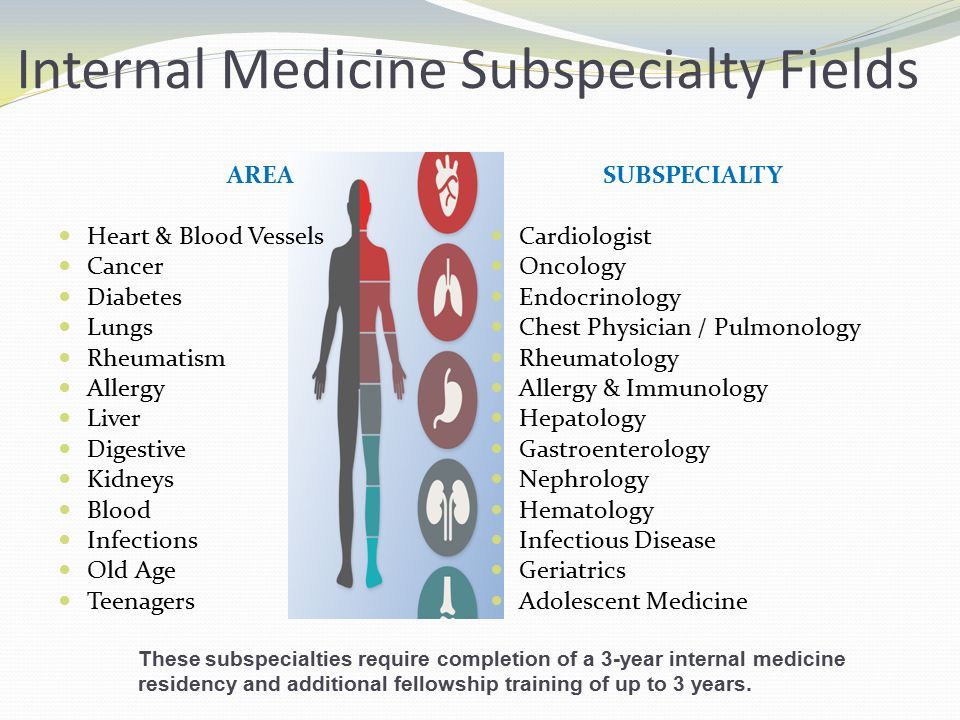

Choosing a career in medicine is as much a financial commitment as it is a vocational one. When people ask, “What is an internist medical doctor?” they are usually looking for a clinical definition—a physician who specializes in the prevention, diagnosis, and treatment of internal diseases in adults. However, from a “Money” niche perspective, an internist represents a specific economic profile within the healthcare industry. They are the backbone of the adult medical system, acting as the primary gatekeepers of patient health and, consequently, the primary drivers of healthcare billing and revenue.

To understand the internist from a financial lens, one must look past the stethoscope and evaluate the Return on Investment (ROI) of their education, the various business models they operate within, and the complex wealth management strategies required to navigate a career that often begins with significant debt and ends with high-net-worth status.

The Financial Anatomy of an Internist: Understanding Earning Potential and ROI

The journey to becoming an internist is one of the most significant financial undertakings a professional can pursue. It begins with four years of undergraduate study, followed by four years of medical school, and concludes with a three-year residency in internal medicine. From an investment standpoint, the “cost of entry” is high.

The Cost of Education vs. Starting Salaries

Most medical students in the United States graduate with an average debt load exceeding $200,000. For an internist, the “break-even” point occurs later than in many other high-paying professions like tech or finance. During the three years of residency, an internist-in-training earns a modest stipend, often between $60,000 and $75,000, which barely covers interest on student loans in many cases.

However, once board-certified, the earning potential shifts dramatically. As of 2024, the median annual salary for a general internist typically ranges from $240,000 to $300,000. While this is lower than surgical specialties like orthopedics or cardiology, internal medicine offers a more stable and predictable income stream. The ROI for an internist is realized over a 20-to-30-year horizon, where the compounding effect of a high salary allows for significant wealth accumulation, provided debt is managed aggressively in the early years.

Geographic Arbitrage and Income Variance

In the world of personal finance, where you live determines how much you keep. For internists, the highest salaries are often not found in high-cost-of-living (HCOL) cities like New York or San Francisco, but in rural or underserved areas. Due to supply and demand imbalances, an internist in the Midwest or the Deep South may earn 20% to 30% more than their counterparts in metropolitan hubs. This “geographic arbitrage”—earning a high salary in a low-cost area—is one of the most effective ways for an internist to accelerate their path to financial independence.

Business Models in Internal Medicine: From Private Practice to Employment

An internist’s financial success is heavily dictated by the business model they choose to work within. The traditional image of the “neighborhood doctor” in a small private practice is evolving into a more complex corporate landscape.

The Shift Toward Hospital Employment

Today, a significant majority of internists are “w-2 employees” of large hospital systems or private equity-backed medical groups. From a financial perspective, this model offers a “guaranteed” salary, comprehensive benefits, and malpractice insurance coverage. It removes the “entrepreneurial risk” of running a business, but it also caps the upside potential. For the internist who prioritizes steady cash flow and a predictable retirement contribution (such as 403(b) or 457(b) plans), hospital employment is the most secure financial route.

The Economics of Private Practice and Partnership

For those with an entrepreneurial spirit, private practice remains an option. In this model, the internist is a business owner. They must manage overhead, which includes rent, staff salaries, electronic health record (EHR) subscriptions, and medical supplies. While the risks are higher, the rewards can be substantial. Partners in a successful internal medicine group often earn more than their employed peers through profit-sharing and the ability to bill for ancillary services like in-house lab work, X-rays, or infusions.

Concierge Medicine and Direct Primary Care (DPC)

A rising trend in the “Money” side of medicine is the Concierge or Direct Primary Care (DPC) model. In these systems, the internist opts out of the traditional insurance-based billing system. Instead, patients pay a monthly or annual subscription fee (membership) for direct access to the doctor.

This model is a game-changer for an internist’s bottom line. By eliminating the administrative “middleman” of insurance companies, the doctor reduces overhead and can maintain a smaller patient panel while often increasing their net income. For the patient, it is an investment in personalized care; for the internist, it is a high-margin business strategy that protects against physician burnout and declining reimbursement rates.

Wealth Management and Debt Strategies for the Modern Internist

Being a high earner does not automatically make one “rich.” Many internists fall into the trap of being “HENRYs”—High Earners, Not Rich Yet. Because they start their earning years in their late 20s or early 30s, they are behind on the power of compounding interest.

Aggressive Debt Liquidation vs. Investment

The first financial hurdle for any internist is the six-figure student loan debt. The strategy here usually involves a choice: Public Service Loan Forgiveness (PSLF) or private refinancing.

- PSLF: If the internist works for a non-profit hospital for 10 years, their federal loans can be forgiven tax-free. This is often the most lucrative “financial bonus” a doctor can receive.

- Refinancing: For those in private practice, refinancing to a lower interest rate and aggressively paying down the principal is the priority to free up cash flow for investments.

Tax Planning and Asset Protection

Internists are in the highest tax brackets, meaning tax efficiency is paramount. Utilizing “Backdoor Roth IRAs,” Health Savings Accounts (HSAs), and defined benefit plans are standard maneuvers for the tax-savvy physician. Furthermore, because of the nature of their work, asset protection is a critical component of their financial plan. This includes high-limit malpractice insurance and the use of trusts or legal entities to shield personal assets from potential professional liability.

Lifestyle Creep and the “Doctor House”

One of the biggest financial risks for an internist is “lifestyle creep.” After years of sacrifice and low pay during residency, many new attendings immediately purchase luxury cars and “doctor houses” using specialized physician mortgages (which allow for low down payments). From a wealth-building perspective, this can be a mistake. Financial experts often advise internists to “live like a resident” for the first few years of their career to stabilize their net worth before increasing their cost of living.

The Future of Revenue in Internal Medicine: Navigating Value-Based Care

The way internists make money is undergoing a systemic shift from “Fee-for-Service” to “Value-Based Care.” Understanding this transition is vital for anyone looking at the long-term economic viability of the profession.

The Move to Value-Based Reimbursement

In the old model, an internist was paid for the volume of patients they saw—more visits meant more revenue. In the new “Value-Based” model, insurance providers (especially Medicare) reward internists for patient outcomes. If an internist can keep a population of patients healthy and out of the hospital, they receive a portion of the “shared savings.” This turns the internist into a “health manager,” where financial success is tied to efficiency and preventative care rather than just procedural volume.

Diversified Income Streams

Many modern internists are diversifying their income to protect against changes in healthcare legislation. This includes:

- Telemedicine: Providing remote consultations as a side hustle.

- Medical Consulting: Working for insurance companies or tech startups to help develop AI-driven diagnostic tools.

- Real Estate: Many physician groups own the building where they practice, allowing them to collect rent and benefit from property appreciation, creating a dual-income stream of professional services and real estate dividends.

Conclusion

What is an internist medical doctor? Clinically, they are the experts on the adult body. Financially, they are high-earning professionals navigating a high-debt, high-reward career path. While the initial costs are staggering, the stability of the profession, combined with the ability to choose between various business models—from hospital employment to the lucrative concierge niche—makes internal medicine a sound financial choice for those who manage their capital as diligently as they manage their patients. By focusing on debt management, tax efficiency, and evolving reimbursement models, an internist can transform a high-salary career into a legacy of multi-generational wealth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.