When navigating the world of real estate, whether as a tenant looking for a place to live or a business seeking commercial space, understanding the fundamental distinctions between renting and leasing is crucial. While often used interchangeably in casual conversation, these two terms represent distinct contractual agreements with significant financial and legal implications. For individuals and businesses managing their finances, grasping these differences can impact budgeting, long-term planning, and overall financial well-being. This article delves into the core differences between rent and lease agreements, focusing on their financial implications and how they affect your personal or business finances.

Understanding the Financial Framework: Short-Term vs. Long-Term Commitments

At its heart, the difference between renting and leasing boils down to the duration of the agreement and the financial flexibility it offers. This distinction has a direct impact on how you budget, manage cash flow, and plan for future expenditures.

The Nature of Rental Agreements: Flexibility and Shorter Durations

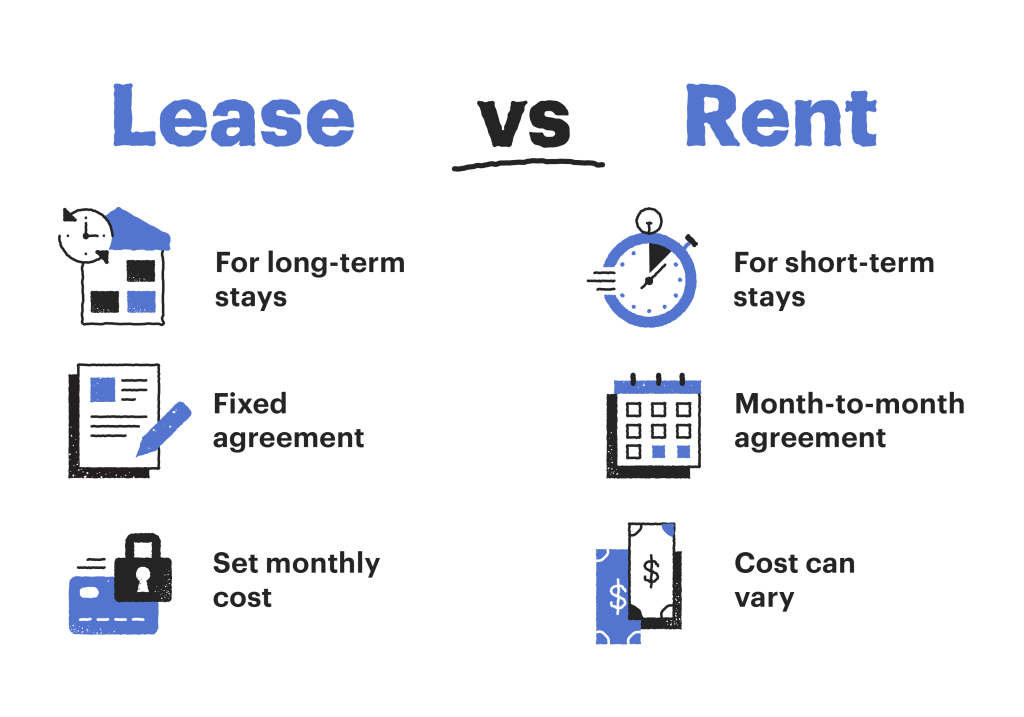

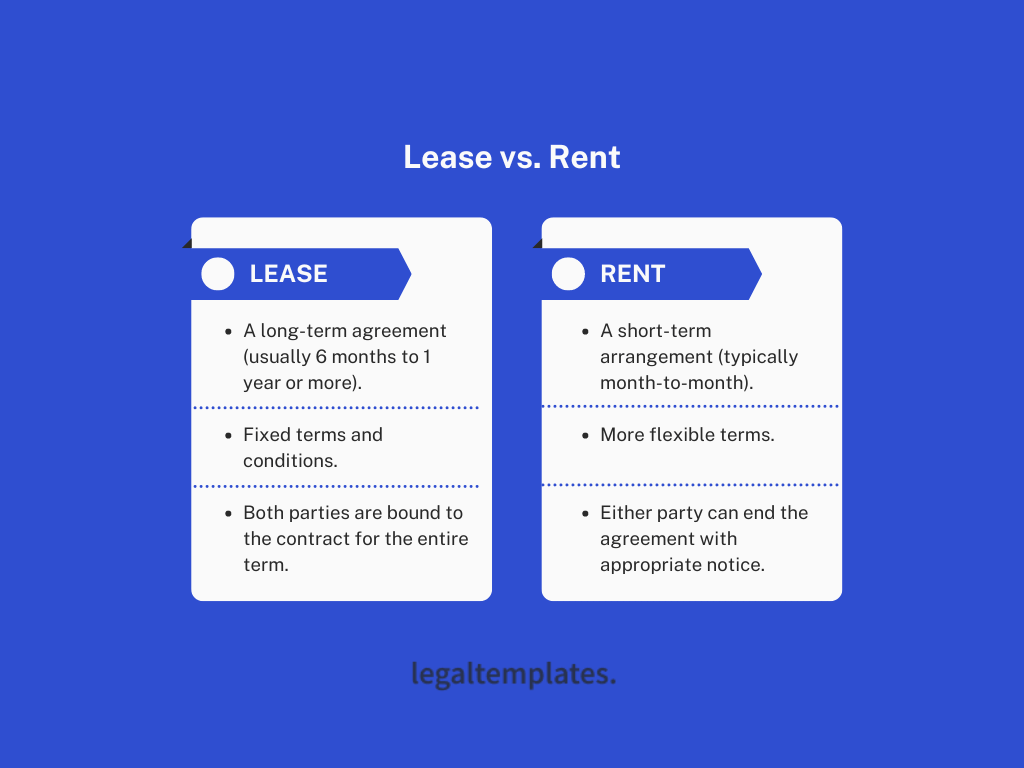

Rental agreements are typically short-term contracts, often on a month-to-month basis, though they can sometimes extend to six months or a year. From a financial perspective, rentals offer a significant degree of flexibility.

Monthly Payments and Budgeting Stability

The most prominent financial characteristic of a rental agreement is the recurring monthly payment. This predictability makes budgeting relatively straightforward. Individuals and businesses can allocate a fixed amount each month for housing or operational space, simplifying cash flow management. For personal finance, this means a consistent housing expense that can be factored into a monthly budget with minimal surprises. For small businesses, this predictable outgoing can be vital for maintaining operational liquidity.

The Cost of Flexibility: Potential for Increases

While flexibility is a hallmark of renting, it also comes with a financial caveat: the potential for rent increases. Landlords can adjust the rental price at the end of each term (usually monthly or annually). This means that the cost of your living or business space is not fixed long-term. Financially, this can introduce uncertainty. A sudden, significant rent hike can disrupt personal budgets or necessitate a business relocation if the new cost becomes prohibitive. This necessitates having a contingency fund or being prepared to absorb increased expenses.

Security Deposits: A Standard Financial Outlay

Most rental agreements require a security deposit, typically equivalent to one or two months’ rent. This serves as financial protection for the landlord against damages or unpaid rent. From a renter’s perspective, this is an upfront financial outlay that needs to be accounted for in the initial moving expenses. While the deposit is generally refundable at the end of the tenancy, it represents capital that is tied up and unavailable for other uses during that period. Proper management of this deposit, understanding its terms, and ensuring its timely return are crucial financial considerations.

The Structure of Lease Agreements: Commitment and Predictable Costs

Lease agreements are characterized by their longer terms, commonly spanning one to five years, or even longer for commercial properties. This commitment brings a different set of financial implications, prioritizing stability and predictability over short-term flexibility.

Fixed Rental Rates: Long-Term Budgetary Certainty

A key financial advantage of a lease agreement is the fixed rental rate. Once a lease is signed, the rental price generally remains the same for the entire term. This provides exceptional budgetary certainty. For individuals, this means knowing exactly how much their housing will cost for several years, allowing for more accurate long-term financial planning, such as saving for other goals or investments. For businesses, a fixed lease payment offers a stable operating expense, making it easier to forecast profitability and plan for expansion or other investments without the immediate worry of fluctuating occupancy costs.

Lease Escalations: Understanding Future Costs

While lease agreements offer fixed rates, it’s important to understand that longer leases may include provisions for rent escalation. These are pre-determined increases in rent that occur at specific intervals throughout the lease term, often tied to inflation or a set percentage. Financially, this requires careful review of the lease document to understand the future financial commitment. While not as unpredictable as month-to-month rent hikes, these escalations need to be factored into long-term financial projections. For businesses, negotiating favorable escalation clauses can be a significant factor in controlling operating costs over time.

Security Deposits and Other Financial Guarantees

Similar to rentals, leases often require security deposits. However, due to the longer commitment and higher value of the property often involved, these deposits can be substantial. Furthermore, some commercial leases may require additional financial guarantees, such as a personal guarantee from the business owner or a larger upfront payment (e.g., first and last month’s rent, plus an additional security deposit). These financial obligations represent a significant upfront investment and can impact the business’s liquidity or an individual’s available capital. Careful negotiation and understanding of these financial requirements are paramount.

Financial Implications for Tenants and Businesses

The choice between renting and leasing has profound and lasting financial implications for both individuals and businesses, influencing everything from daily cash flow to long-term investment strategies.

For Individuals: Renting for Simplicity, Leasing for Stability

When it comes to personal finance, the decision hinges on individual circumstances, risk tolerance, and financial goals.

Renting: Minimizing Upfront Costs and Maximizing Liquidity

For individuals who prioritize flexibility or have a lower tolerance for long-term financial commitments, renting is often the more appealing option. The upfront costs associated with renting are typically lower than leasing, primarily consisting of a security deposit and the first month’s rent. This allows for greater liquidity, meaning more cash is available for immediate use, investment, or emergency savings. This is particularly beneficial for those who are early in their careers, anticipate frequent relocations, or prefer to keep their options open.

Leasing: Securing Predictable Housing Costs and Long-Term Planning

Conversely, individuals who are settled in an area and plan to stay for several years may find leasing a financially advantageous option. The ability to lock in a rental rate for an extended period provides a significant advantage for long-term financial planning. It eliminates the worry of rent increases that could strain a budget and allows for more precise savings goals. For those aiming to purchase a property in the future, a predictable housing expense from a lease can free up funds for a down payment.

Impact on Credit and Financial Reputation

Both rental and lease payments, when made consistently and on time, can positively impact an individual’s credit history. However, the reporting mechanisms can differ. Some landlords and property management companies report rent payments to credit bureaus, which can help build or improve credit scores. Similarly, consistent lease payments demonstrate financial responsibility, which can be viewed favorably by future lenders or landlords. Late payments or defaults on either agreement, however, can have severe negative consequences for creditworthiness.

For Businesses: Leasing for Operational Certainty, Renting for Agility

Businesses, particularly small to medium-sized enterprises (SMEs), face unique financial considerations when choosing between renting and leasing.

Leasing: A Cornerstone of Business Financial Planning

For most businesses, a lease agreement is the standard for commercial real estate. The predictable, fixed costs associated with a long-term lease are invaluable for operational stability and financial forecasting. Businesses can confidently budget for occupancy expenses, which is critical for profitability projections, loan applications, and investment decisions. This certainty allows businesses to focus on growth and operations rather than being constantly subjected to the vagaries of short-term market fluctuations in rental rates.

Renting: Navigating Early-Stage Uncertainty and Niche Needs

Renting can be a viable option for businesses in their nascent stages, those requiring highly adaptable space, or those in industries with rapid technological changes. For startups, a month-to-month lease offers the flexibility to scale operations up or down without the burden of a long-term commitment, should their trajectory change unexpectedly. It minimizes upfront capital expenditure, allowing crucial funds to be directed towards product development, marketing, or staffing. This agility can be a significant competitive advantage in dynamic markets.

Impact on Business Loans and Investment

The financial structure of your real estate agreement can significantly influence a business’s ability to secure financing. A stable, long-term lease agreement often demonstrates a well-managed and sustainable business, making it more attractive to lenders and investors. The predictable expense of rent contributes to a lower debt-to-income ratio, a key metric for loan approval. Conversely, a reliance on short-term, unpredictable rental agreements might be viewed as a sign of instability, potentially hindering access to capital for expansion or R&D.

Key Financial Clauses and Considerations in Agreements

Beyond the fundamental differences in duration, both rental and lease agreements contain specific clauses that have direct financial implications. A thorough understanding of these is vital for responsible financial management.

Security Deposits and Holdover Clauses

The security deposit is a universal financial element. In rentals, it’s usually a fixed sum to cover potential damages. In leases, especially commercial ones, it can be more substantial and might include additional guarantees. Understanding the conditions for its return is critical. A “holdover clause” is another important financial consideration, particularly in leases. It dictates what happens if a tenant remains in the property after the lease expires. Typically, the rent dramatically increases, often doubling or tripling, to incentivize a prompt departure. This can lead to substantial, unexpected financial penalties if not managed carefully.

Maintenance, Repairs, and Utilities: Who Pays?

The allocation of responsibility for maintenance, repairs, and utilities has direct financial consequences. In most rental agreements, landlords are responsible for major repairs and structural maintenance, while tenants handle minor upkeep and utility payments. In commercial leases, the “triple net lease” (NNN) is common, where tenants are responsible for property taxes, insurance, and maintenance costs in addition to rent. This significantly increases the tenant’s financial burden and requires careful budgeting for these variable expenses. Understanding these clauses before signing is paramount to avoiding unexpected financial outlays.

Subletting and Assignment Rights: Financial Repercussions

The ability to sublet or assign your rental or lease can have financial implications. Subletting allows you to rent out the property to another party, potentially recouping some of your rental costs if you need to vacate early. Assignment involves transferring the entire lease to another party. Both require landlord permission and typically come with specific conditions and fees. Financially, understanding these rights can provide an exit strategy or a way to generate income from a property you can no longer use, mitigating financial losses. Conversely, restricting these rights can leave you financially exposed if circumstances change.

Making the Right Financial Choice: Rent vs. Lease

The decision between renting and leasing is not merely a matter of preference; it’s a strategic financial decision that impacts your long-term financial health and stability.

Evaluating Your Financial Goals and Risk Tolerance

Before committing to either a rental or a lease, a comprehensive assessment of your financial goals and risk tolerance is essential. Are you prioritizing short-term flexibility and minimizing upfront costs, or are you seeking long-term predictability and stability in your expenses? For individuals saving for a down payment or investing aggressively, the liquidity offered by renting might be more beneficial. For businesses needing to forecast operational costs with precision, a lease is almost always the preferred choice.

Understanding the Long-Term Financial Landscape

While short-term financial advantages are important, considering the long-term implications is crucial. A series of short-term rentals, while offering flexibility, can lead to higher overall housing costs over several years due to potential rent increases. Conversely, a long-term lease, even with a small annual escalation, might prove more cost-effective and financially secure over the same period. For businesses, the stability of a lease can foster stronger relationships with lenders and investors, facilitating growth and expansion.

The Importance of Legal and Financial Due Diligence

Regardless of whether you are renting or leasing, thorough due diligence is non-negotiable. This involves carefully reading and understanding every clause in the agreement, paying particular attention to financial obligations, responsibilities for maintenance, and any clauses that could lead to unexpected costs. Consulting with a legal professional or a financial advisor to review the terms can prevent costly mistakes and ensure you are entering an agreement that aligns with your financial capabilities and long-term objectives. Ultimately, the most financially sound decision is one that is well-informed and strategically aligned with your personal or business financial roadmap.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.