In today’s hyper-connected world, convenience is king. From ordering groceries with a tap to managing your finances on the go, mobile technology has revolutionized how we interact with the world, and perhaps nowhere is this more evident than in how we handle payments. Mobile check deposits, a feature embraced by banks and financial institutions, offer a seamless way to deposit funds directly from your smartphone, saving trips to the branch or ATM. However, as with any digital innovation, this convenience is not without its shadows. The very ease of mobile deposits has opened the door to a new breed of financial fraud: the fake mobile check.

This article delves into the deceptive world of fake mobile checks, exploring how they operate, what red flags to watch out for, and how to protect yourself. Drawing on themes from technology, brand integrity, and personal finance, we’ll equip you with the knowledge to navigate this increasingly sophisticated landscape and safeguard your hard-earned money.

The Rise of Mobile Deposits and the Emergence of Fraud

Mobile check deposit, a seemingly innocuous technological advancement, has become a cornerstone of modern banking. Its adoption has been rapid, driven by consumer demand for speed and accessibility. Banks, in turn, have invested heavily in developing and refining these mobile platforms. This surge in legitimate mobile check activity, however, has unfortunately created a fertile ground for fraudsters to exploit.

The core principle of mobile check deposit is straightforward: a user captures an image of the front and back of a physical check using their smartphone camera and uploads it through their bank’s mobile app. The bank then processes this digital image as if it were the physical check. This process relies on a combination of sophisticated imaging technology, Optical Character Recognition (OCR) to read the check details, and secure data transmission protocols.

However, the illusion of simplicity can be a powerful tool for deception. Scammers leverage this familiarity and perceived ease to introduce fraudulent checks into the system. These fake checks can range from cleverly altered legitimate checks to entirely fabricated documents designed to mimic real ones. The goal is always the same: to trick individuals and financial institutions into believing that a worthless or invalid instrument holds real monetary value.

Understanding the Mechanics of Mobile Check Fraud

The methods employed by fraudsters to create and pass fake mobile checks are diverse and constantly evolving. Understanding these tactics is the first step in protecting yourself. Broadly, these schemes fall into a few categories:

1. Counterfeit Checks: These are entirely fabricated checks, often printed on sophisticated printing equipment designed to replicate the security features of genuine checks. They might mimic the look and feel of checks from legitimate businesses or even personal checks. The details on these checks (account numbers, routing numbers, payee names) are often fictitious or belong to compromised accounts.

2. Altered Checks: This involves taking a legitimate check and altering its key information. This could include:

* Payee Change: Using chemicals or erasures to change the name of the intended payee to the fraudster’s name.

* Amount Manipulation: Changing the written or numerical amount of the check to a higher value.

* Forged Signatures: While harder to pass through mobile deposit due to the requirement of endorsing the back, fraudsters might attempt to forge signatures or present checks where the endorsement is already complete.

3. Stolen Checks: In some instances, fraudsters may obtain stolen checks from individuals or businesses and then attempt to deposit them. While not strictly “fake” in their creation, their use by an unauthorized party constitutes fraud.

4. “Real” Checks from Non-Existent Accounts: Some scams involve presenting checks drawn on accounts that either don’t exist or have been deliberately drained of funds. The check itself may look authentic, but the underlying financial backing is absent.

The underlying technology of mobile deposit, while robust, is not infallible. Banks employ various checks and balances, but the speed at which these transactions occur can sometimes allow fraudulent checks to slip through, at least initially. This is where the responsibility of the individual becomes paramount.

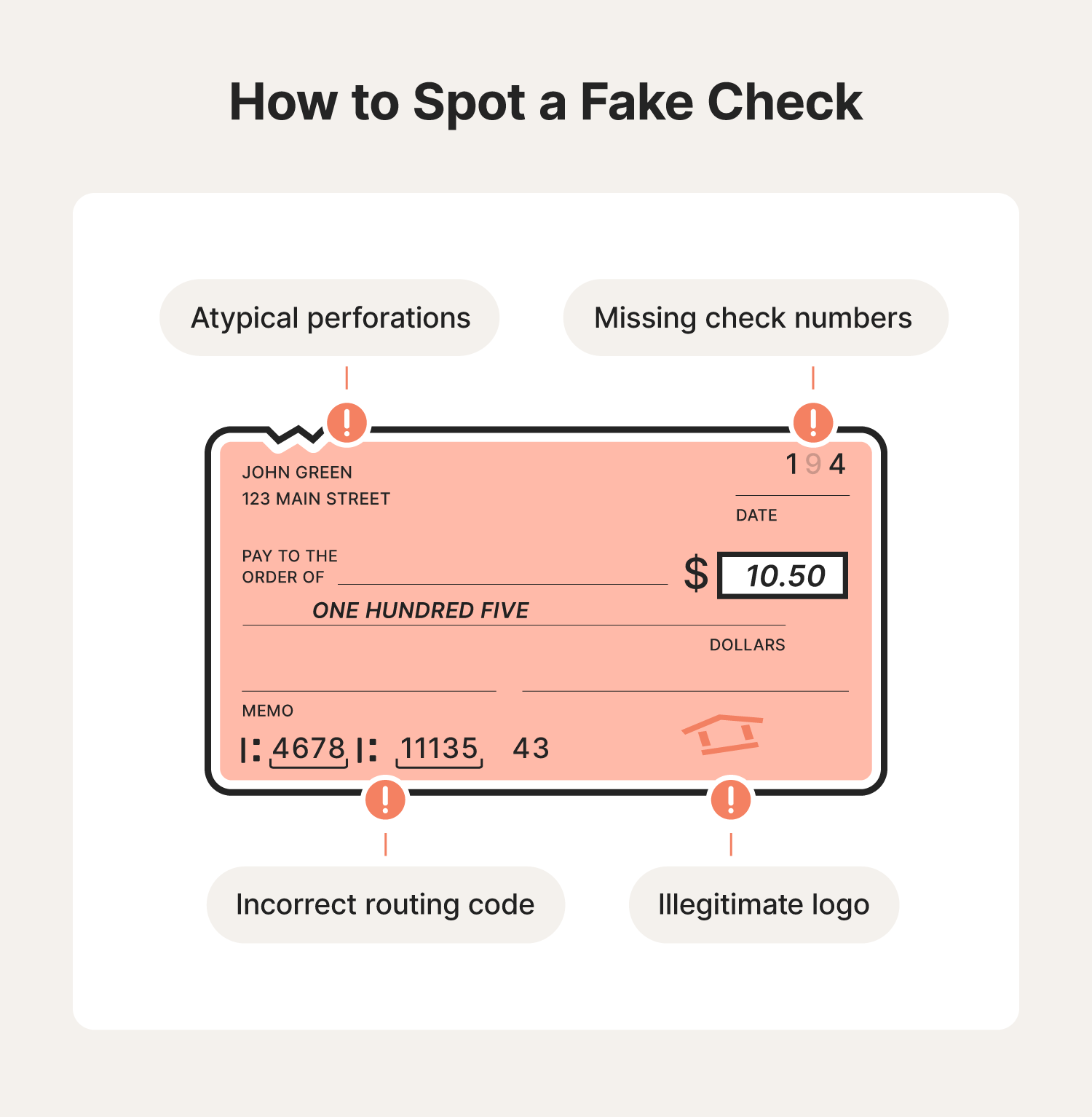

Identifying the Red Flags: What to Look For in a Suspicious Mobile Check

Recognizing a fake mobile check before you deposit it is crucial. While advanced counterfeiters can create very convincing forgeries, there are often subtle indicators that can betray their deception. These red flags can be broadly categorized by what you see on the check itself, and how the situation surrounding the check unfolds.

Visual Clues on the Check Itself

When you are presented with a check you intend to deposit via your mobile device, take a moment to scrutinize it carefully. Don’t let the convenience of the app blind you to potential problems.

-

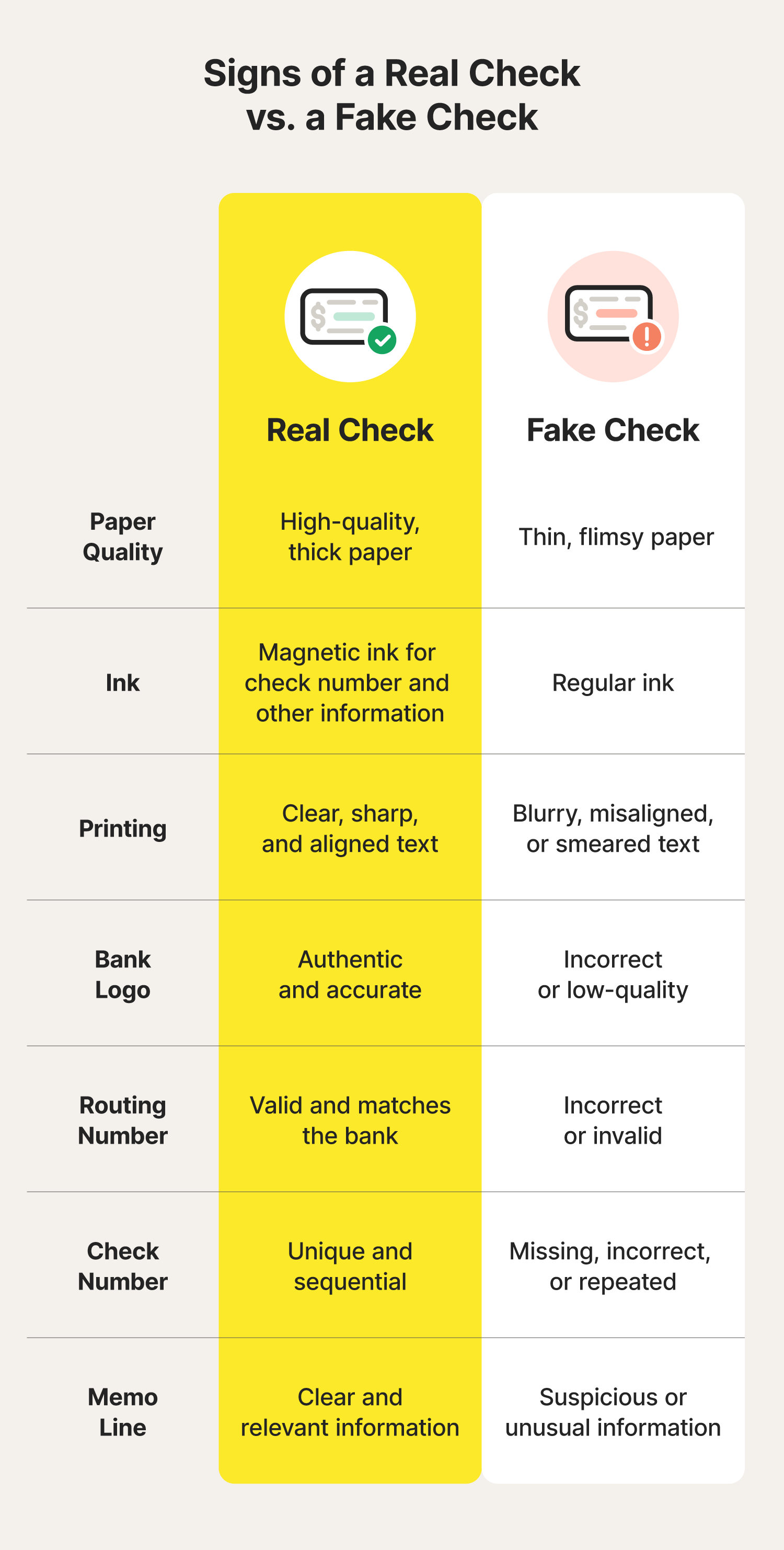

Paper Quality and Security Features: Genuine checks are printed on specialized paper with security features designed to prevent counterfeiting. Look for:

- Watermarks: Many checks have faint watermark designs that are difficult to replicate.

- Microprinting: Tiny text, often too small to read with the naked eye, that appears as a solid line.

- Security Threads: A colored or metallic thread embedded within the paper.

- Color-Shifting Ink: Ink that changes color when viewed from different angles.

- Unusual Texture or Thickness: Fake checks may feel flimsy, too thick, or have a glossy finish that is not typical of security paper.

-

Printing Quality and Alignment: Examine the clarity and precision of the printing.

- Blurry or Smudged Text: Poor quality printing, especially around the numbers and text, can be a giveaway.

- Misaligned or Uneven Lines: The lines in the MICR (Magnetic Ink Character Recognition) line at the bottom of the check should be perfectly straight and uniformly spaced.

- Incorrect Font or Size: Counterfeiters may use fonts that are similar but not identical to the standard banking fonts.

-

Information Discrepancies: Cross-reference the details on the check.

- Routing and Account Numbers: While the MICR numbers themselves might be printed correctly, ensure they correspond to a legitimate bank. A quick online search for the routing number can help verify its authenticity. Be wary if the routing number doesn’t seem to match the bank name printed on the check.

- Payee and Amount Alignment: The written-out dollar amount should precisely match the numerical dollar amount. Any discrepancy is a major red flag.

- Bank Logo and Name: Ensure the bank’s logo and name are accurate and properly placed. Counterfeiters sometimes use outdated logos or slightly misspelled bank names.

- Address and Contact Information: Legitimate businesses and individuals usually have clear contact information. Vague or missing addresses can be suspicious.

-

The Endorsement (Back of the Check): This is particularly important for mobile deposits.

- “For Mobile Deposit Only” Notation: Most legitimate checks used for mobile deposit will already have this restriction clearly printed or stamped on the back by the bank or intended payee. If you have to write it yourself on a check that doesn’t have it, it might indicate the check wasn’t intended for mobile deposit.

- Signatures and Endorsements: Ensure the endorsement signature matches the payee name on the front of the check. If the back of the check is already signed by someone other than the payee, or if the endorsement looks forced or poorly executed, it’s a concern.

Situational Red Flags: Beyond the Paper

Fraudsters often employ manipulative tactics to pressure individuals into depositing fake checks quickly, before they have a chance to thoroughly examine them. Be wary of situations that feel “too good to be true” or involve unusual circumstances.

-

Unsolicited Offers and Overpayments: If you receive a check for more than the agreed-upon amount for a sale, service, or job, especially with instructions to return the difference or use some of the funds for a separate task, it’s a classic overpayment scam. The original check will likely bounce, leaving you responsible for the funds you’ve already sent out.

-

Pressure to Deposit Immediately: Scammers want to get the funds into your account before the fraud is detected. If someone is pressuring you to deposit the check and send them money immediately, be suspicious.

-

Unfamiliar Payers or Companies: If the check is from an individual or company you don’t recognize, and you haven’t conducted any business with them, exercise extreme caution.

-

Requests for Personal Information: While not directly related to the check itself, if the person offering the check also requests sensitive personal information (social security number, bank login details), it’s a significant red flag for identity theft.

-

“Mystery Shopper” or “Secret Shopper” Scams: These often involve sending a check, asking you to purchase gift cards or other items, and then sending the remaining funds back. The check will invariably be fake.

By combining a keen eye for visual detail with an awareness of suspicious circumstances, you can significantly reduce your risk of falling victim to mobile check fraud. Remember, if something feels off, it’s always better to err on the side of caution.

Protecting Yourself and Your Finances: Best Practices for Mobile Check Deposits

Preventing fake mobile check fraud is a multi-layered approach that involves understanding the risks, employing vigilance, and utilizing the tools and resources available to you. While banks have security measures in place, the ultimate responsibility for safeguarding your financial well-being rests with you.

Vigilance Before and During the Deposit

The most effective defense is to be proactive. Don’t let the ease of mobile banking lead to complacency.

-

Verify the Payer and the Transaction: Before accepting any check, ensure you know who the payer is and that the amount reflects a legitimate transaction you have engaged in. If it’s a business check, confirm that the business is legitimate. A quick online search can often reveal if a company is reputable.

-

Inspect the Check Thoroughly: As detailed in the previous section, take the time to examine the paper quality, printing, security features, and all numerical and written information on the check. Trust your instincts; if something looks or feels unusual, it probably is.

-

Use Your Bank’s Official App: Only use the legitimate mobile banking app provided by your bank or credit union. Never download or use third-party apps claiming to offer check deposit services, as these are often scams designed to steal your information or deposit fraudulent checks.

-

Follow the App’s Instructions Carefully: Mobile deposit apps provide specific instructions for capturing images of the front and back of the check. Ensure the images are clear, well-lit, and that the entire check is visible, including all four corners. Proper capture is essential for the bank’s verification process.

-

Write “For Mobile Deposit Only” on the Back (If Necessary): While many banks pre-print this, if your app instructs you to endorse the check and it doesn’t have this notation, write “For Mobile Deposit Only” beneath your endorsement. This helps prevent the check from being deposited elsewhere.

Post-Deposit Actions and Staying Informed

Even after a successful deposit, it’s important to remain vigilant.

-

Monitor Your Account Activity: Regularly check your bank account statements and online transaction history. Look for any discrepancies or unexpected withdrawals. If you notice a fraudulent deposit that was initially accepted and then reversed, understand the implications for your account balance.

-

Understand Funds Availability Policies: Be aware of your bank’s funds availability policy. Banks typically hold deposited funds for a certain period to allow for verification. Funds from mobile deposits, especially for larger amounts, may not be immediately available. Do not spend money from a mobile deposit until you are certain the funds have cleared and are available in your account.

-

Keep Physical Checks Secure: After successfully depositing a check via mobile app, do not immediately discard the physical check. Most banks recommend holding onto the physical check for a specified period (e.g., 14-30 days) before securely destroying it (shredding it is ideal). This allows time for any potential fraud to be discovered and gives you a physical record if needed.

-

Report Suspicious Activity Immediately: If you suspect you have deposited a fake check or have encountered a suspicious check-cashing attempt, contact your bank or financial institution immediately. Report the incident to the Federal Trade Commission (FTC) and potentially local law enforcement. The sooner you report, the better the chance of mitigating any damage.

-

Educate Yourself and Others: Stay informed about the latest scam tactics. Share this information with friends, family, and colleagues, especially those who may be less familiar with digital banking risks. Financial literacy and awareness are powerful deterrents.

The Role of Technology and Brand Trust

While individual vigilance is key, the broader technological landscape and the integrity of brands play a significant role in combating fraud.

-

Bank Security Measures: Banks are continuously investing in advanced fraud detection systems, including AI and machine learning algorithms that can identify suspicious patterns in mobile check deposits. As technology evolves, so do the methods used to combat fraud.

-

Brand Reputation and Trust: Legitimate businesses and financial institutions strive to maintain a strong brand reputation built on trust and security. When dealing with unknown entities, the absence of a recognizable and trustworthy brand can be a warning sign. Scammers often operate without established brands, making their offers seem less scrutinized.

-

App Security and Updates: Ensure your mobile banking app is always up-to-date. Software updates often include critical security patches that protect against emerging vulnerabilities.

By understanding the nuances of mobile check fraud, actively looking for red flags, and adhering to best practices, you can confidently utilize the convenience of mobile check deposits while significantly reducing your exposure to financial deception. In the digital age, knowledge and vigilance are your most valuable assets in protecting your money.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.